UPCOMING EVENTS

LATEST BLOG

QUERY OF THE WEEK

Virtual Elevate Conference

Thursday 14th October at 10am

Virtual Workshop

Tuesday 9th October 2021

Landbay

‘How 2021 is setting the scene for Q4 and into 2022’

By Paul Brett, Managing Director, Intermediaries

Are there any lenders that will do a residential remortgage on a house with 10 acres of land and a place to moor boats next to the land? The property is also next door to a boat repair shop.

Legal & General Protection

New process of paying commission

In order to help improve the efficiency of your business we are implementing a new process of paying commission for policies sold.

Currently, the commission we pay to you is in advance of the collection of the customers 1st premium payment. The new process will move to paying commission once we are in receipt of the customer’s 1st premium.

This change will take effect from 1st November 2021; any business completed after this date will be subject to these new payment terms.

We have updated our Terms of Business Agreement relating to the new commission payment terms.

Please click on the link here to find a copy of the amendment to Terms of Business Agreement and Terms of Commission.

We are doing this to help improve your cashflow management and reduce transactions and reconciliations relating to commission payments.

In order to help improve the efficiency of your business we are implementing a new process of paying commission for policies sold.

Currently, the commission we pay to you is in advance of the collection of the customers 1st premium payment. The new process will move to paying commission once we are in receipt of the customer’s 1st premium.

This change will take effect from 1st November 2021; any business completed after this date will be subject to these new payment terms.

We have updated our Terms of Business Agreement relating to the new commission payment terms.

Please click on the link here to find a copy of the amendment to Terms of Business Agreement and Terms of Commission.

We are doing this to help improve your cashflow management and reduce transactions and reconciliations relating to commission payments.

October is Breast Cancer Awareness Month

Breast cancer is the most common cancer worldwide, and October marks a month of awareness for the disease.

In 2020, 2.3 million people were diagnosed with breast cancer globally, which now puts the disease ahead of lung cancer as the most common cancer diagnosis. In the same year worldwide, there were 685,000 deaths from breast cancer.

Here in the UK, there are around 55,000 new cases diagnosed every year. The latest figures show that incidence of breast cancer diagnosis grew by 23% between 1993 and 2017, with a 4% drop between 2014 and 2017. Rates for male breast cancer have remained stable for the past two decades.

The good news is that survival rates for breast cancer are typically high, with 9 in 10 surviving one year after diagnosis, and 85% surviving beyond five years since their diagnosis. 75.9% those diagnosed will survive for 10 or more years after their diagnosis. It’s thought between 23%-37% of breast cancer cases can be prevented with lifestyle changes.

In 2020, we paid out 578 breast cancer-related critical illness claims, and 347 breast cancer-related life claims. 2020 saw huge impacts to cancer diagnosis and care due to Covid-19. Estimates suggest that around 11,000 people are now living with undiagnosed breast cancer, and around 10,600 fewer patients have started their breast cancer treatment in England due to disruptions by Covid-19.

For more information including signs, symptoms and support, Breast Cancer Now is the UK charity leading the October national campaign.

Source: https://www.breastcanceruk.org.uk/about-breast-cancer/facts-figures-and-q-as/facts-and-figures/

Buckinghamshire Building Society

Adverse and impaired credit further supported

Our new Bucks Solutions Portfolio has now launched, and provides extended support to those who have experienced credit issues in the past or who are finding it challenging to secure a mortgage.

The new products use a credit matrix structure (click here for details) which allows us to offer a range of rates and LTVs, based on someone’s individual circumstances.

In addition to this, we are dedicated to supporting people on the journey to owning their own home. That is why we continue to offer:

- Additional flexibility for those people with varying levels of credit blips

- Bespoke and human approach to underwriting

We recognise the market has changed drastically during the last two years and we are working hard to respond to the changing needs of the customer. We are continuously reviewing and improving the products we offer and look forward to announcing more new products shortly.

About Buckinghamshire Building Society

Buckinghamshire Building Society is an award winning, mutually owned independent Building Society, first founded in 1907. The Society is based in the beautiful Buckinghamshire village of Chalfont St Giles and offers simple savings accounts to its members, as well as specialist mortgage products to customers, through intermediaries. We are dedicated to providing excellent customer service and pride ourselves on the work we do to give back to our local community.

Loughborough Building Society

Increase LTV on Standard JBSP Mortgages

The Loughborough have announced the increased LTV on standard Joint Borrower Sole proprietor mortgages as 90% with immediate effect.

These are currently available for residential mortgages in England and Wales.

It allows both older family members to help out younger and younger family members to help out their elders. So with up to 4 people on the mortgage application family members are able to assist one another to own their own home no matter what age.

As all parties will be responsible for the mortgage payments, there is no requirement for the proprietor to be able to take on the mortgage alone until all family members are ready and able to make the change.

The proprietors’ income is insufficient to cover the mortgage without the assistance of additional joint borrower(s) who live independently from the mortgaged property. Affordability will be assessed taking into account income and commitments of all named parties.

The Loughborough criteria allows one aspect of the affordability to be based on the balance of the mortgage at the point the joint borrower retires, this allows the proprietor to potentially take a mortgage over 35 years, rather than have a restricted mortgage term at the outset.

Ashley Pearson, BDM says ‘We launched in November 2020 at 85% and have been pleased with the response. Increasing the LTV to 90% means we will be able to help more people realise their home ownership ambitions’

NatWest Intermediary Solutions

Reducing and Simplifying our Valuation Fees

We are delighted to announce that effective immediately, we have reduced and simplified our purchase Valuation Fees where they are applicable,

What you need to know:

We currently offer a free valuation for all purchase applications where the lower of the purchase price or property value is less than or equal to £2m (Only the first standard valuation is fee free). This is now moving to less than or equal to £3m and will be based per property, rather than per application.

Where a valuation fee is applicable we are reducing the number of property value bands from 24 down to just 2, and are also reducing our valuation fee from an average of £352 down to a flat rate of £177 (including admin fee) on any property up to £3m in value.

The new valuation price bandings are as follows (if you select a non-fee product):

- Purchase price or property value up to and including £3million = £102 + £75 admin fee = £177

- Purchase price or property value above £3million = £1,380 + £75 admin fee = £1,455

For any properties valued over £10m these are available, upon request via LGSS.

The valuation fee is applied automatically for new applications from 6th October. The new fee structure will appear on all new applications immediately.

Please note that there is no change to Home Buyer or Structural reports

Precise Mortgages

Important application information

On Sunday 10 October our online mortgage system will be unavailable whilst some important maintenance takes place.

IMPORTANT: If you’ve recently received a decision in principle, you’ll need to advance this to the ‘App submitted stage’ by 5pm on Saturday 9 October.

If you fail to do so you’ll unfortunately need to start again and re-key.

If you have any queries, please contact our intermediary support team on 0800 116 4385.

Zephyr Homeloans

007 great reasons to consider Zephyr

To mark the release of the latest Bond film in cinemas, here’s why you should always spy on Zephyr for your specialist BTL cases…

£0 application fees*

0% product fee option*

7 criteria highlights:

– 2&5 yr Fixed rates up to 80% LTV

– Max loans to £2m

– Single properties & portfolios

– Standard & Specialist properties – HMOs, MUFBs, FACs, New Builds

– Individuals & Limited Companies (SPVs)

– Personal & Portfolio income backed Top Slicing considered**

– Consistent and reliable service

* Other fees and costs apply. ** Subject to criteria.

If you’ve got a specialist BTL case on your desk – don’t be shaken or stirred, give our expert team a call.

To discuss a new case and quickly find out if this will fit with Zephyr – please find the contact details for your RSM and Telephone BDM on our website.

For general enquiries about Zephyr, please contact us on 0370 707 184 (Mon to Fri from 9am to 5pm) or just send us an email.

Take a look at some cases we’ve recently supported:

- Client purchasing the flat above his own main residence – We’re able to consider BTL properties within close proximity of other owned BTLs or the applicant’s residential home.

- Two brothers, one a first-time landlord and a first-time buyer, moving a MUFB property into a new SPV, then remortagaging next-day to raise cash to fund a property purchase on the same street – We accept new Ltd Co (SPV) applications from related Directors and allow remortgaging for capital raising purposes.

AIG

AIG Life CPD qualifying webinar – Intermediary Quality – An insight into Lead Generation

Kelly Phillips will be hosting the webinar and will be joined by Alain Desmier, owner of Contact State, and Ryan Berry, owner of Cornerhouse Media. Both are respected experts in the field and will offer their insights into how to get the best out of lead generation, and what regulation will mean for advisers.

Register here – https://bit.ly/3zfKRzg

Skipton Building Society

Increased Max Loans and Product Changes

We’re making changes to our full mortgage product range, as well as increasing our Residential maximum loan sizes. Full details can be found below.

Key Changes

We’re increasing our Residential max loan sizes. Full details can be found below:

- Less than or equal to 80% LTV now £1,000,000.

- 80.01- 85% LTV now £800,000.

- 85.01- 95% LTV now £600,000.

Aviva Equity Release

CPD sessions available

If you are looking to learn more about Equity Release, you should join the Aviva property webinars. It is a join presentation by our experts Neil Uttley – Equity Release national sales manager and Andrew Tuner – our in house chartered surveyor.

You’ll discover more about:

- The common misconceptions concerning valuations and how to access property values

- How to deal with complex and often difficult property scenarios

- Our lending criteria that lets us to say yes to more customers

- The role of the valuer and what’s expected of them

There are two dates to choose from making it easier for you to develop your skills at a time that suits you.

- Weds 13th Oct 2.00pm to 3pm – https://event.on24.com/wcc/r/3452300/112A6B021F893AC4B1493DD854A0A3C4

- Friday 15th Oct – 10.00am – 11.00am – https://event.on24.com/wcc/r/3452340/F59A2FF22D4667500208E9B4B3480772

Royal London

Maximise your protection conversations with tenants and letting agents

Through working together, we want to make sure more tenants are told about their protection options during the lettings process.

To help you access this potential client base, and grow your business, we’ve developed a range of protection tools and support materials including:

- A sales aid outlining the benefits of income protection for letting agents.

- A sales aid for tenants with example case studies

- Email templates to help you approach letting agents and tenants.

- Email templates for letting agents to send to their tenants.

- Email footers to promote income protection for tenants and encourage queries and referrals.

- An income shortfall calculator

You’ll also be able to register for our latest protection webinar ‘Unlocking protection opportunities in the UK rental market’ which takes place on Thursday 21 October 2021.

Santander for Intermediaries

Changes to ERC refund window for non-simultaneous porting

To support existing customers moving home during the pandemic, where redemption of the existing mortgage and purchase of the new property was non-simultaneous, we temporarily extended the ERC refund window. With effect from 1 January 2022 the ERC refund window for non-simultaneous porting will change as follows:

- Standard purchase cases (non-new build) will revert back to three months (currently five months) in total.

- New build purchase cases will revert back to six months (currently 8 months) in total.

Please remember Flexible Offset porting has always been excluded from this policy and will continue to be excluded. If your client is porting a Flexible Offset mortgage, redemption and completion must be on the same day (simultaneous).

For more information visit our existing Santander mortgage customers moving home page.

Saffron for Intermediaries

Self-employed criteria announcements

We’ve added medical underwriting across our Just For You Lifetime Mortgage range to help you respond to the FCA’s challenge for improved personalisation.

And six in 10 people could borrow more, or reduce their borrowing costs.

Just

Helping you deliver lifetime mortgage solutions unique to every client

We’ve added medical underwriting across our Just For You Lifetime Mortgage range to help you respond to the FCA’s challenge for improved personalisation.

And six in 10 people could borrow more, or reduce their borrowing costs.

Vida Homeloans

Changes to BTL Expat Criteria

As one of our valued partners who has recently submitted an Expat application to us, we wanted to make you aware of some changes which we are making to our Buy to Let Expat criteria which is effective for all new applications submitted from today Thursday 7th October.

Vida will consider applications submitted from British Citizens who hold a current UK passport and are residing outside of the UK in selected EEA or Worldwide countries listed below:

| Austria | Belgium | Bulgaria |

| Croatia | Cyprus | Czechia |

| Denmark | Estonia | Finland |

| France | Germany | Greece |

| Hungary | Iceland | Ireland |

| Italy | Latvia | Lichtenstein |

| Lithuania | Luxembourg | Netherlands |

| Norway | Poland | Portugal |

| Romania | Slovakia | Slovenia |

| Spain | Sweden |

Rest of the world

| Australia | Canada | Gibraltar |

| New Zealand | Switzerland | South Africa |

| UAE | USA |

Please find attached our updated Expat flyer and Criteria guide for your information and any pipeline Expat applications will continue to be processed as normal.

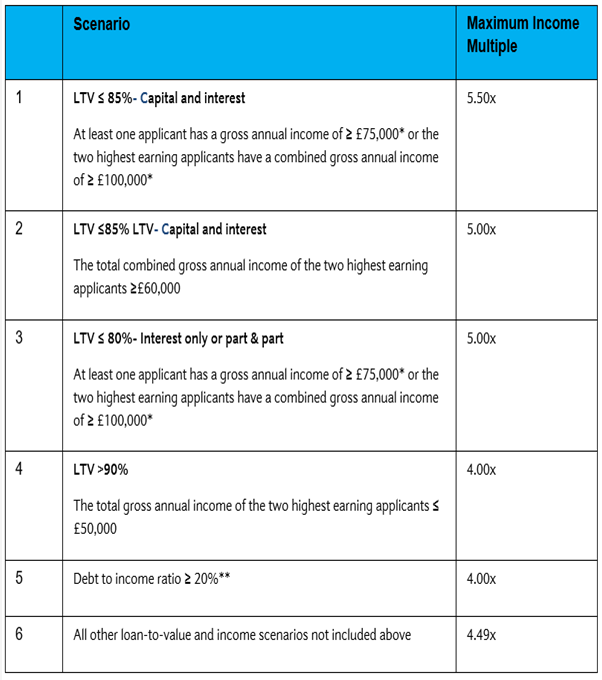

Barclays

Improved Residential ‘Loan-to-Income’ multiples

We’re pleased to announce the launch of a new improved set of loan-to-income multiples for residential lending, effective today, Friday 1st October, 2021.

This means that from today, the following limits will automatically be applied when a residential lending decision is reviewed on a case, including on submitted pipeline applications.

Our improved loan-to-income multiples

* The income components considered when deciding if the minimum income threshold is met are: Basic income + sustainable allowances + self-employed income.

** Debt to Income ratio is calculated as monthly credit commitments after completion as a percentage of gross monthly income.

Please click here if you unable to view the above image our improved loan-to-income multiples

Also, as part of our ongoing commitment to simplify and enhance our lending criteria, we’re extending the residential applications on which we’ll consider annual bonus income within our affordability assessment. From today, Friday 1st October we’ll also factor annual bonus income into our assessment of affordability on residential applications where your clients are applying to re-finance existing commitments.

Please be advised our lending policy and the affordability calculators on our website have been be updated to reflect the changes.

Live More

A fresh look at affordability – a webinar from LiveMore

Are you wondering how much your semi-retired, self-employed clients can borrow from LiveMore, or if your single applicant with rental income will be able to get a mortgage?

Following the huge success of our affordability webinar on September 21st, we have decided to host it again!

During our 45-minute webinar, you will be provided with a brief overview of LiveMore, and we will demonstrate real life customer scenarios of cases we have been able to help using our fresh, common-sense approach to affordability.

We will also cover;

• Examples of how different types of income can affect affordability

• A demonstration of how our affordability calculator works

• How our affordability calculator can help potential borrowers over 55.

95.45% of attendees confirmed they felt more confident running our affordability calculator, after they attended our previous webinar!

The webinar will be hosted by:

Matt Kingston – Regional Sales Manager

Attendees who attend the full session will be sent learning certificates which can be used for CPD.

We encourage brokers to ask questions during the event, but if you would like to provide us with any questions you have in advance, please supply when registering below. We will do our best to get through as many as possible.

West One

Dispelling the myths of specialist BTL

Further to last weeks Myth #3 around specialist buy-to-let, the team at West One are sorting the fact from the fiction and this week tackling two myths. Find out more and how to be in with a chance to win a luxury hamper here…

Myth #3

While most high street lenders will make an automated decision using the clients credit score, a specialist lender will have more products available for borrowers with impaired credit.

At West One, we do not credit score, instead our underwriting is based on a credit assessment and each case is assessed individually on its merits.

Myth #4

Unsurprisingly, self-employed individuals find the high street approach to self-employed hard, with many lenders requiring 2 years of accounts so that they can see a stable income and assess the level of risk.

This approach doesn’t consider the changing landscape of a self-employed business. A specialist lender will take the time to understand the individuals’ circumstances, taking a view on 1 years trading or the latest years accounts. And for those whose self-employment is being a professional landlord whose sole source of income is their property portfolio, we at West One Can assist these clients and accept this type of income.

West One are offering you the chance to enter their free prize draw to win a luxury hamper from Fortnum and Mason. Click here to enter: https://www.westoneloans.co.uk/dispelling-the-myths-of-specialist-buy-to-let-clubs-networks

Entries must be received by 5 pm on Friday 22nd October. We will be announcing the lucky winner on Monday 25th October!

The Loans Engine

TLE TICK ALL THE BOXES

At TLE we like to tick all the boxes and provide market leading solutions for your clients whether they need a Second, First, Bridge, Buy to Let, Commercial or Development Mortgage.

SECOND CHARGE MORTGAGES – RATES FROM 3.34% pa

- Up to 100% LTV

- Residential, BTL, CBTL and HMO

- All credit profiles considered

- Flexible income ratios

BRIDGING – RATES FROM 0.43% pm

- Up to 85% LTV

- Most property types considered

- Regulated and non-regulated

- Any legal purpose

SPECIALIST FIRST CHARGE – RATES FROM 3.80% pa

- Up to 85% LTV

- Residential, CBTL and Unencumbered

- Purchase and Remortgage products

- Flexible LTI and poor credit accepted

SPECIALIST BTL – RATES FROM 2.85% pa

- Up to 80% LTV

- No experience required

- Most property types considered

- Adverse accepted

COMMERCIAL – RATES FROM 3.6% pa

- Up to 80% LTV

- Commercial and semi-commercial

- Owner occupied and investors

- Most property types considered

DEVELOPMENT – RATES FROM 7.00%

- Full planning to be in place

- 65% LTGDV

- SPVs or Personal Names

- Land should be owned already

Call now to refer clients to The Loans Engine for Second, First, Bridging, Complex BTL, Commercial and Development mortgages.

Platinum rated service (see Broker Reviews here), market leading commission, and attractive client fees are just a few of the benefits of working with TLE.

Whenever you have cases you’re struggling to place, think TLE!

TLE will pay you commission and do all the work for you!