UPCOMING EVENTS

LATEST BLOG

QUERY OF THE WEEK

Virtual Workshop

Thursday 30th September at 10am

GI Quote & Apply Demo

Friday 8th October at 10am

Virtual Elevate Conference

Thursday 14th October at 10am

Precise Mortgages

‘Finding Solutions for your Self-Employed Clients’

By Liza Campion, Head of Corporate Accounts, Precise Mortgages

My client is buying a house with Japanese knotweed (category 2) in the neighbour’s garden. Which lenders will consider this?

Santander for Intermediaries

Self-Employed and Furlough Update

Residential Self-Employed Applications

From Monday 27th September, Santander for Intermediaries are simplifying their definition for applicants where business and or income was adversely affected by Covid-19.

New Covid-19 definition

They’ll consider your client as adversely affected where any of the below apply:

- A business which is not currently trading or has been re-opened for less than three months

- Where the business has taken an SEISS, JRS grant (for limited companies) or Bounce-Back, BBIL or CBIL loans in the last 12 months prior to the date of application

- Staff have previously been furlough due to business trading conditions in the 12 months prior to the date of application

Click here to see the full details including additional evidence requirements.

PLEASE NOTE: INTRODUCER INTERNET DOWNTIME

Introducer Internet won’t be available from 9pm on Saturday 25 September until 6am on Monday 27 September.

Brokers won’t be able to submit cases during this time. We’re sorry for any inconvenience caused.

RELIANCE BANK

New Intermediary Website Launch

Reliance Bank are delighted to announce that following hard work behind the scenes and in response to your valuable feedback they have launched a new intermediary website.

To visit their new website you will need to use one of the following browsers:

- Google Chrome

- Firefox

- Safari

Their new website is www.reliancebankltd.com/intermediary and you will need to enter the following password:

789456 – please keep this to hand should you need to visit their site in future.

IPSWICH BUILDING SOCIETY

Ipswich launch back into the Shared Ownership Market

Ipswich Building Society are delighted to be back in the Shared Ownership Market.

Criteria

- Max loan £500k

- Available for purchase and remortgage

- Purchase includes new build houses and flats up to 10 storeys

- Flats above good quality commercial on a case-by-case basis

- Ability to staircase

- Properties throughout England and Wales

Click here to find out more.

WEST ONE BTL

DISPELLING MYTHS OF SPECIALIST BTL

Post pandemic, there is likely to be an increase of borrowers that high street banks will be unable to serve as their borrowing needs have become more complex. This presents a huge opportunity for the specialist lending market to step in and support the UK’s 2.7 million landlords.

Specialist lending has sometimes been thought of as a last resort, something the buy-to-let team here at West One are passionate about changing. Over the next few weeks, we will be sorting the fact from the fiction and offering brokers the chance to win a luxury hamper!

Discover our first myth and how to enter our competition here…

MYTH 1 – THE PROCESS IS SIMILAR TO THE HIGH STREET – FACT

One of the biggest myths is that specialist finance is complicated, while the cases themselves may be complex the process isn’t.

A specialist lender will have the resources to do the necessary checks while looking at each case individually in order to propose a transparent solution that is easy to understand.

Like many high street lenders, specialist lenders have a professional and streamlined process allowing them to deliver a quick answer to the borrower.

West One are offering you the chance to enter their free prize draw to win a luxury hamper from Fortnum and Mason. Click here to enter: https://www.westoneloans.co.uk/dispelling-the-myths-of-specialist-buy-to-let-clubs-networks

Entries must be received by 5 pm on Friday 22nd October. We will be announcing the lucky winner on Monday 25th October!

THE MORTGAGE LENDER

Updated BTL Criteria

- Increase loan amount for a HMO to £2m

- Increase loan amount for a MUB to £3m

- Increase in New Build to £2m

- Increase in Flats above commercial properties to £2m

- Aggregate lending limit to apply to any type of property – based on maximum £5m lend only

- Separate concentration limits for flats and houses on individual developments and buildings

- Updated concentration limit for small block of flats – Flats in a single development, less than 4 = 100%, 5-10 = 75%, 10-20 = 50%

PURE RETIREMENT

NEW VIDEO AVAILABLE – WATCH NOW

Pure Retirement’s CEO, Paul Carter, recently featured on their YouTube channel to review the lender’s most recent quarterly market report, available via the lender’s Adviser Toolkit, providing a thorough market commentary into the customer and market trends spanning the previous quarter.

Paul sat down with Senior Comms and Editorial Executive Gareth Ware to discuss headline figures from the report in greater detail to explore how the market performed over the first half of the year, analysing research and statistics from a number of leading industry sources. Topics covered include what the saving patterns of Gen X’ers could mean long-term for the retirement planning sector, the marked increase in gifting, the pension pot gender gap, and the equity release knowledge gap among the public.

Watch the video in full via the Pure Retirement YouTube channel

KENSINGTON

SOMETHING SPECIALIST IS COMING

As we approach our 1 year anniversary of lending in Northern Ireland, we’ll be coming to the Hilton Belfast on Tuesday 28th September. Along with our New Business Director, Craig McKinlay and your BDM, Sharon Cochrane, I’ll be joined by Jordan Buchanan, PropertyPal, who will be giving you a market update. Check out the full agenda below.

Don’t miss this event and register now

KEYSTONE PROPERTY FINANCE

PRODUCT TRANSFER FOR KEYSTONE’S EXISTING BORROWERS

Keystone Property Finance product transfer option allows landlords to seamlessly switch to a new rate once their current deal ends.

Landlords can choose from the current core selection of two and five-year fixed rates up to 75% LTV, which includes the standard, specialist and green ranges.

Product transfer for borrowers include:

- No application fee

- No valuation fee on standard properties

- No legal fees

- 1% arrangement fee which applies to all products and can be added to the loan or paid upfront

- Procuration fee of up to 0.45%

- Available or individuals, Limited Companies, Trading limited companies and LLPs

- Available on houses and flats (please contact our internal sales team to discuss HMOs and freehold blocks)

If you have any questions or need any assistance with your complex buy to let case enquiries, Keystone’s Business Development Managers are here to help, call their broker hotline on 0345 148 9086, email enquiry@keystonepropertyfinance.co.uk or speak to them via the online chat feature here.

LV= PROTECTION

COMPREHENSIVE INCOME PROTECTION SOLUTIONS

At LV=, we believe that protecting income underpins financial resilience and wellbeing. That’s why we’ve extended our already comprehensive range of income protection solutions. We now offer two new products Executive Income protection– to help smaller businesses cover the cost of providing sick pay benefits to a key employee, and Mortgage and Rent cover designed to help those with variable earnings look after their Mortgage or rent payments, if they become unable to work because of illness or an accident.

Our Income protection solutions allow you to tailor policies to your clients’ protection needs, budget and lifestyle. Not only that, they also provide a range of emotional and practical support services.

To find out more about our New Mortgage and Rent cover or New Executive Income protection or any of our comprehensive Income protection solutions please click here.

To find out more about how LV= can support you and your clients, visit LVadviser.com, contact your LV= Account Manager or call us on 0800 032 4219.

Need to find out the latest on your pipeline applications? Check the Protection Progress Hub

PARAGON BANK

INCORPORATING DURING A FIXED RATE

Do your landlord clients have the flexibility to move property from their personal name to limited company ownership during a fixed rate? With Paragon they can!

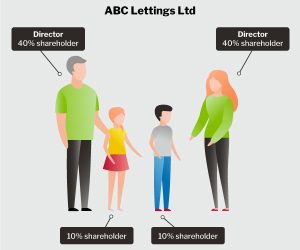

Example

Mr and Mrs Smith are existing Paragon borrowers, having completed on their 5 year fixed rate in May 2017. On the back of specialist tax advice, they’ve been advised that they should look to move the ownership through to an SPV limited company. However, their current ERC’s do not expire until May 2022.

Background

- On the back of tax advice, Mr and Mrs Smith set up a new SPV limited company

- Mr and Mrs Smith are listed as Directors holding 80% shares between them

- Their two children, aged 7 and 5, hold 10% of shares each

The above set-up would also work for an existing SPV limited company, owned by the applicants, that already holds buy-to-let properties with other lenders.

The process of incorporating with Paragon

• Mr and Mrs Smith notify us that they wish to incorporate using our incorporation application form

• They also send us confirmation and details of the advice they have received to incorporate

• We will check the limited company to ensure the Directors match the applicants, and that the main focus of the company is centred around property letting

• A deeds release fee of £75 plus VAT (per mortgage account) is paid

• We will issue a “deed of covenant” to the Solicitors, which is subsequently lodged with Land Registry, completing the process

Result

Mr and Mrs Smith have incorporated their personally owned buy-to-let property through to limited company ownership, with no change in their existing loan terms.

IMPACT SPECIALIST FINANCE

BRIDGING LOANS: A BROKERS GUIDE

Have a client with a great opportunity but not the funds? A bridging loan could help keep the deal moving.

From keeping a house purchase on track if the chain breaks down, to funding renovations on an unmortgageable auction property, you could be missing a trick if you’re not looking at bridging finance.

What is bridging finance?

The clue is in the name. Bridging loans are short-term finance to bridge the gap between money going out and money coming in. So, they are an option for clients wanting to buy their next property before another has sold, or to pay for renovations on a ‘fixer-upper’ they are planning to sell on.

Regulated bridging loans are secured on residential property and have a maximum term of 12 months. Unregulated bridging loans, which can be secured on residential investment property, semi-commercial, commercial property, or land, also usually have a 12 month term but longer durations are available.

Bridging finance could be the answer if:

- The client won’t be keeping the property long, or they’ll move to a longer-term loan once their short-term spend has driven an increase in value.

- When they need money fast (for example, to secure an auction property).

- If their property is deemed uninhabitable, but the loan will pay for renovations that mean it can be mortgaged in the future.

Want to know more?

Call the impact team on 01403 272625 or email bridging@impactsf.co.ukwith your enquiry.

LEGAL & GENERAL PROTECTION

YOUR REMINDER TO ENTER THE BUSINESS QUALITY AWARDS

Closing date for entries 22 October 2021

If you haven’t entered yet, now is the time to nominate yourself for our Outstanding Customer Outcome award.

We’ve got to hand it to you — you’re always there for your clients. That’s why we’re inviting you to showcase your work and gain extra recognition.

And why we’re organising a big celebration to celebrate the positive impact you make upon your clients’ lives every day.

All BQA nominees are shortlisted based on exceptional performances and statistics, delivering excellent end-to-end client experiences over the last twelve months, and rising to the challenges recent times have brought

FOUNDATION HOME LOANS

Do your portfolio landlords have full awareness and understanding of the new EPC legal requirements?

As one of the first specialist lenders to launch a green mortgage offering, our ongoing aim is to help a variety of borrowers to benefit from energy-efficient properties, and positive and feedback from our intermediary partners suggests that a growing number of landlords, homeowners and potential homeowners are becoming more environmentally conscious when it comes to their homes and investments.