AVIVA Protection

On demand CPD opportunities

Aviva 2023 claims event

CPD 2 hours

Synopsis: Revisit Aviva’s 2023 claims launch where we look at our individual claims data, how value added services support the customer and hear from customers about how Aviva have supported them.

Book your place now!

Making the most of the claims report

CPD 30 mins

Synopsis: Join Aviva as they walk you through the 2022 claims report and how to best use this with your customer

Making the most of the claims report

MacMillan Q&A

CPD 30 mins

Synopsis: Hear from our partner Macmillan, to understand how the current cost of living rises are impacting Cancer patients

Q&A with Macmillan

Aviva Digicare+

CPD 30 mins

Synopsis: Join us as we demonstrate the value of benefits available via the award winning DigiCare+ app

Aviva DigiCare+ giving customers protection from day one

Global Treatment

CPD 30 mins

Synopsis: Take a deep dive into the Global Treatment product, covering the what, when and most importantly why you want to be talking to your customers about it

Global Treatment – everything you need to know

Send to customer

CPD 1 hour

Synopsis: Find out how to use send to customer, an enhanced journey which allows customers to take control and complete their own underwriting questions.

Customer Launch Event (4275462) (on24.com)

Ask the Experts: Opportunities in the rental market

CPD 1 hour

Synopsis: Join us as we look at the size of the rental market, we look at the demographics of the market and gain an understanding of tenants and how to engage them.

Opportunities in the rental market

Ask the Experts: Global Treatment

CPD 1 hour

Synopsis: Join us as we look at the impact of Covid on a cancer diagnosis, why people might travel for treatment and the global treatment customer end to end process.

Global Treatment

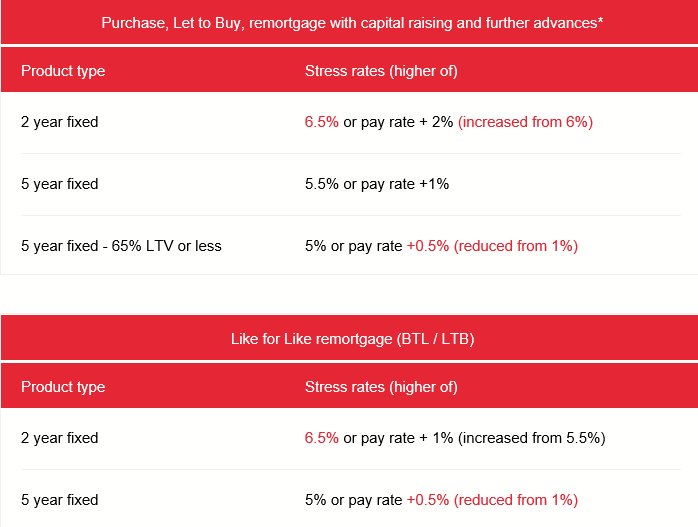

BM Solutions

changes to stress rates

To ensure that we continue to lend responsibly, from Thursday 7 September we are making changes to the way we assess the affordability of our mortgage applications.

Changes include:

- Reduced pay rate plus margin for 5 year fixed like for like remortgage stress rate

- Reduced pay rate plus margin for 5 year fixed 65% LTV or less

- Increased minimum stress rates for all 2 year fixed.

Use our online calculator to get an accurate borrowing figure.

*For further advances to qualify for 5 year stress rates the total loan, including all existing balances, must be fixed for 5 years or more at point of application.

These changes will apply to all new Decisions in Principle and Full Applications started on or after Thursday 7 September. For the current stress rates to apply a full application must be keyed before 8pm Wednesday 6 September.

The website and online calculator will be updated to display and calculate the new stress rates.

If you have any queries, please refer to your Business Development Manager.

Launch of Top Slicing for Buy To Let applications

We are pleased to announce the launch of Top Slicing for qualifying BM Solutions Buy to Let (BTL) applications from today Thursday 7 September.

Top slicing enables customers who have a shortfall in their required lending, to use a proportion of their earned income when the rental income for the BTL property is not sufficient to hit our standard rental cover ratio (RCR) calculation.

Minimum Top Slicing Qualifying Criteria

- Not available for Portfolio Landlord customers

- Not available for Let to Buy customers

- Minimum income £100k per application (First two applicants)

o PAYE

o Self-employment

o Pension

o Profit from UK land and Property - Minimum stressed 125% RCR – below this, the standard RCR calculation is offered

- Maximum stressed 145% RCR – Over this, the standard RCR calculation is offered.

IMPORTANT INFORMATION

- Please ensure that all commitments and income are keyed accurately

- Any inaccuracies will delay an application and may affect the loan being offered

- The rental calculator has been updated to assess Top Slicing affordability Birmingham Midshires (bmsolutionsonline.co.uk)

A full affordability assessment will be carried out as part of an application automatically to ensure that it meets our minimum top slicing requirements and that the customers have enough disposable income to cover any rental shortfall required for any requested loan.

If an application doesn’t meet our top slicing requirements the standard rental cover ratio calculation will apply and the max loan available will be offered.

If an application meets our top slicing requirements and the customers have available disposable income an increased loan maybe offered up to the maximum RCR amount. This amount could be lower than the requested loan but higher than the standard RCR assessment amount.

Any changes to an application would result in a reassessment and a different amount of lending could be offered, including up to the standard rental cover ratio amount.

The Intermediaries website will be updated to reflect these changes.

If you have any queries, please refer to your Business Development Manager.

Bath Building Society

Introducing our new Broker Online system

Hot on the heels of our new online decision in principle form, we have launched a new version of our Broker Online full mortgage application process.

The new portal offers a slicker process and additional functionality to provide a much better online experience with us, including:

- Simpler application form with intuitive questioning to avoid repetition.

- Bespoke packaging requirements to ensure you know exactly what our underwriters require before submission.

- Automatic updates will be issued at appropriate milestones to help you keep on top of the process.

Recent improvements to our online Intermediary experience also include real time updates for our service levels, a new affordability calculator powered by L&G and live chat electronic assistant, Bea, available (alongside the team in office hours) to answer lending criteria questions 24/7.

There’s a lot going on and further updates are coming soon, but in the meantime if there’s anything you think we can do to make your experience with the Society better, look out for the next Intermediary feedback survey in your inbox and let us know.

HSBC

We’ve improved our Foreign National lending policy

With effect from today, Friday 1st September, we’ve made the following enhancements to our Foreign National lending policy:

EU Settlement Scheme

- EU citizens who were granted a pre-settled status under the EU Settlement Scheme will be eligible for standard lending policy. Their share code status must still be confirmed.

- EU citizens who arrived in the UK after 31st December 2020 were not eligible for the EU Settlement Scheme and the Foreign National policy should continue to be applied.

Minimum 12 months working in the UK

- Foreign national customers will no longer be required to prove they have worked in the UK for a minimum of 12 months. Standard employment policy and evidence requirements apply.

- The requirement to have lived in the UK for 12 months has not changed and must continue to be evidenced.

Our Broker website will be updated shortly to reflect the above changes.

Further information

Chat with us or call our Broker Support Team on 0345 600 5847 (Monday to Friday, 9am to 5pm).

Hodge

Walking in the shoes of today’s RIO customer

If life begins at 40, then why would we treat over 50s as though it’s time to start winding down and setting aside time to browse retirement home brochures?

According to NIH research those over forty see themselves as 20% younger, which probably isn’t a surprise to anyone reading this who’s hovering around the big 4-0.

So, is fifty the new forty? And when did we say life begins?

At Hodge, we’re all about shattering stereotypes, especially negative ones. And excuse the pun, but ageism is an age-old problem. So, when it comes to thinking about what today’s RIO customer looks like, we first need to remind ourselves what fifty actually looks like.

Picture this…

Picture someone in their twenties. What are they likely to be doing? Saving for a house. Out socialising every weekend in bars and clubs. Forging their new career path. Getting married. Travelling the world. Starting a family. They could be any number of those things, simultaneously.

Now picture someone in their fifties. Did socialising, shopping, travelling or buying a house spring to the front of your mind? If not, here is why it should. are the fastest growing age group in the UK. They make up 35% of the population but contribute 76% to the UK’s financial wealth and just below half of its consumer spending. Over fifties outspend every other age bracket in recreation and culture, cars, food, alcohol, travel, household goods and services.

We may put this luxury of higher disposable income down to the generational wealth gap. Over 50% of baby boomers owned homes by the age of thirty and with surging house prices comes increased wealth. The reality is many homeowners have their equity tied up in their property. Or they may be paying or looking to move to interest-only mortgages to keep outgoings lower.

We know RIO is a niche product for a niche market, we understand affordability and all that comes with it can seem daunting, but we’ll work with you every step of the way until you speak RIO like a pro. From BDM support to underwriters who believe in common sense and the human touch, we’re always working with you. Hodge has your back.

We have an established history in the later life lending space, having been founders of the first equity release mortgage back in 1965. We focus on what the customer wants, that’s why we’ve fully taken the plunge into alternative, specialist over 50s’ mortgage lending. Our goal, to drive innovation in the market and meet the needs of the ever-changing face of today’s over 50s borrower. Their retirement, however, that may look and everything that comes next, no longer follows a stereo typical path, so neither do our mortgages.

LiveMore

Changes to bank statement requirements

We wanted to let you know about some changes we’ve made after some feedback from brokers.

Previously, we requested bank statements for all cases. As LiveMore lend to ages 50 and over, we know that it’s not always ideal to get bank statements from your older clients.

That’s why we’ve changed our policy so we no longer require bank statements for most cases.

There are some exceptions; such as adverse credit, non-standard income (e.g. foreign income) and self-employment. Otherwise, I hope you find this is a useful change.

We’re always looking for ways to make your experience better and help you to place more cases with clients over 50. That’s why LiveMore offers more affordability, more property types and more products

Paymentshield

Launching a new referral service

Paymentshield has launched a new referral service meaning advisers can now more easily offer insurance to every client.

We’re able to offer your clients advice on your behalf ensuring those customers receive full continuity of service following the advice they received during the mortgage process.

As soon as a client is referred to Paymentshield you’ll be able to track their journey from start to finish so you have full transparency of progress and the ultimate outcome.

This service is currently being rolled out to appointed representatives of most of our network partners. If you’d like more information on if it’s available to you, please contact us using the form below.

How does it work?

Referring to Paymentshield is easy! All we need is your client’s name, contact details, the type of insurance they need help with and when they’d like us to contact them.

Step 1 – Login to Paymentshield’s Adviser Hub

Step 2 – Go to the referral section from the main menu

Step 3 – Decide to complete the referral form yourself or share a link with your client

Step 4 – Submit the form with the client’s name, contact details and when they’d like to be contacted

Step 5 – Check the details then leave it to us

Skipton Building Society

Skipton Talks Technology with Mortgage Introducer & Mortgage Brain

Watch Skipton’s latest videocast hosted by Mortgage Introducer.

Tune in to hear from the experts Jonathan Evans, Skipton’s National Accounts Lead and Neil Wyatt, Sales and Marketing Director at Mortgage Brain Group where they discuss the development of tech in the mortgage market, and how it’s helping to deliver better outcomes for consumers, brokers and lenders. Whilst not forgetting the importance of the human touch.

Tune in to the latest video to hear from the experts.

The Exeter

Income risk calculator – you can now add your logo!

We’re committed to helping experts like you grow your business. That’s why we’ve enhanced our Income Risk calculator to allow you to co-brand. Simply upload your details, your logo and create professional customer facing documents.

The Mortgage Lender

Economic update – September 2023

We’ve teamed up with 4most Economic Consultants to provide you with a monthly economic update. The update for September is now available to download.

The update covers:

- Inflation and interest rates

- Labour market

- Housing market

- Rental market

- Mortgage market – Activity

- Rate analysis