WEBINARS ON DEMAND

BLOGS

UPCOMING EVENTS

ROYAL LONDON

What’s on the menu?

FLEET MORTGAGES

Who are Fleet Mortgages? BTL case studies

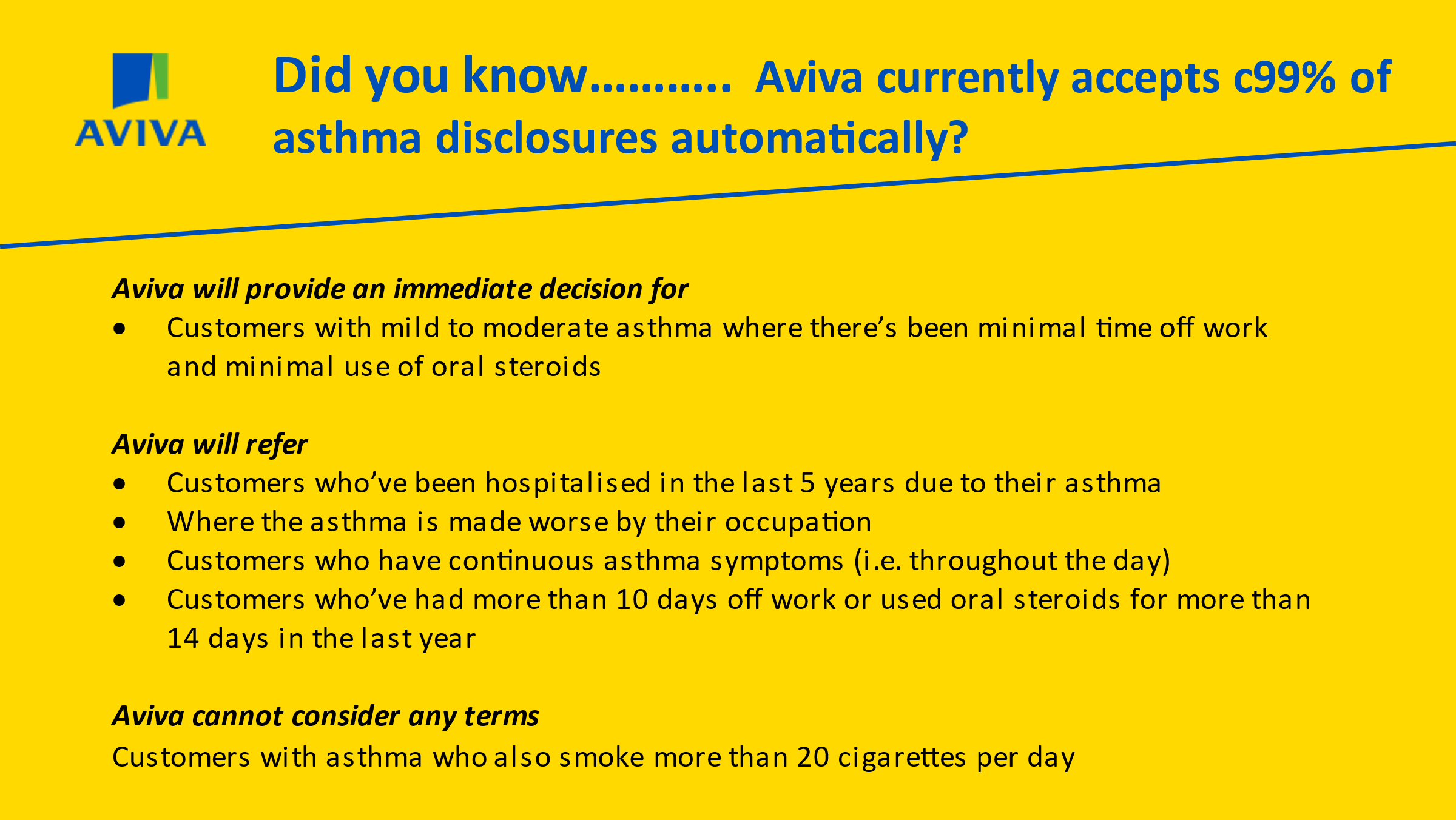

JUST

Making it personal

CLYDESDALE BANK

In the spotlight

HODGE

It’s time we stopped calling Later Life, well Later Life

TMA Club

The age-old question for brokers

AMI

Looking head in 2022

Virtual Protection Workshop

Date: Friday 18th March at 10am -12:30pm

CPD: 2.5 hours

Click here to register.

Face to Face Workshops

The dates and locations for these events are below.

5th April – The Village Hotel Watford

6th April – The Village Hotel Edinburgh

7th April – The Village Hotel Solihull

Halifax Intermediaries

Product Transfer Revaluations

From Monday 28 February if you request a property revaluation as part of a product transfer (PT) application you need to make the customers aware they may receive a text message from our surveying partner e.surv as part of the valuation process.

If e.surv do not have adequate information to complete a remote valuation – from their usual desktop tools / resources – they will use a new service called Remote Valuation Assist to ask the customer for further detail on their property.

The customer will receive a text message with a link from e.surv, asking them to confirm a few basic details of their property – number of bedrooms, bathrooms etc. and then to take photos of their property – front, rear, bedrooms, kitchen, bathroom and submit these to e.surv.

If e.surv already have adequate information available to complete a remote valuation they will not contact the customer and e.surv will decide when they use the new service depending on property type etc.

e.surv will look to use the information and photos provided by the customer using Remote Valuation Assist to complete a remote valuation. If they are still unable to complete a remote valuation they will arrange an internal inspection of the property at no cost to the customer.

If the customer does not provide the information / photos requested within 48 hours, or chooses not to provide these, an external appraisal will be arranged. The customer cannot request a particular type of valuation and the revaluation is for lender purposes only.

Wherever possible a correct mobile number for the customer should be provided on the screen when requesting a PT revaluation.

This process will allow e.surv to complete more PT revaluations by remote valuation thereby increasing the speed of the revaluation process for customers.

Instructions and support on how to use the link will be provided to the customer on the text message received from e.surv together with confirmation of how the data will be used.

Please see guide to Remote Valuation Assist with some common FAQs.

Vida Homeloans

Key Worker Guide

Our Key Worker Mortgages are for essential skilled workers employed in the public sector who provide vital community services.

Highlights

- Qualifying applicants can borrow up to 5.5X their total income, applied to all parties to the application

- Up to 90% LTV including fees

- Second job income & shift allowances accepted

- At least one party to the application needs to be a Key Worker

- Fee Saver option available – One free valuation on properties up to £500k, £0 product fee and £250 contribution towards legal costs

Newcastle Intermediaries

Launch of Self Employed Products

These products are designed to support newly Self Employed clients who have been trading for less than 2 years and the product range includes the following highlights;

- Competitive Two Year products available up to 80% LTV;

- Choice of a fee assisted product which offers a free standard valuation providing choice for our customers;

- 10% overpayment facilities across all products, which supports your clients who require the flexibility to make lump sum overpayments. This is in addition to the £499 regular monthly overpayments already permitted;

Full product details will be found on http://www.newcastleis.co.uk/products.aspx upon launch however if you need any specific details in the meantime please let me know.

Loughborough Building Society

Re- Launch 5.5 x Income Product!!

We recognise that some borrowers are able to afford a loan however the income multiple reduces their borrowing power. Whilst those borrowers will still need to demonstrate the ability to afford the new mortgage through an affordability assessment, they will be able to borrow up to 5.5x their income

Suitable borrowers will be able to take advantage of a 3.49% Fixed Rate for 5 years with a £999.00 completion fee, up to maximum 80% LTV and a maximum loan of £750,000.00 (Free Valuation) First Time Buyers, Remortgage, Purchase Acceptable

Key Information:

- Minimum Income £50k Sole Applicant & £75k Joint Applicants (This product is not specific to “professional” applicants, it is instead based on applicants earnings regardless of their Job type)

- Minimum Loan Size £200,000.00 (This could help applicants who have other financial commitments, Loans, Credit Cards etc)

- Maximum Loan Size £750,000.00

- Maximum LTV 80%

- 5.5 x income is only available on this specific product, (Shared Ownership, BTL, Specialist Self Employed, Family Assist, JBSP is not permitted)

- Self Employed (Remember we can consider Salary, Dividends and Net Profit which could help with the income multiples)

- We ignore probation periods

- Sub-contractors that have been subcontracting to the same firm for 6 months treated as employed

IMPACT SPECIALIST FINANCE

Fast Solutions for Auction Finance

Are your clients looking to purchase an auction property and need funds urgently? If yes, have they considered

Auction Finance?

Auction Finance is a bridging loan for when clients wish to purchase a property at auction but require funds in a short amount of time to complete a full payment within the deadline.

Impact SF has access to a comprehensive panel of bridging lenders. We have built strong relationships with these lenders who will take a view on all aspects of an individual case, including limited distribution lenders.

Access a faster bridging solution, call the Impact team on 01403 272625 or email bridging@impactsf.co.uk

Royal London

February was National Heart Month

Putting your clients’ wellbeing at the heart of what we do.

With 1 in 2 of us experiencing a heart or circulatory condition during our lifetime and with over 12% of Royal London critical illness claims paid out for Heart Attack in 2020*, it’s important as ever that your clients protection is about more than money.

The British Heart Foundation suggest a few ways that people can improve their heart health. These include keeping track of blood pressure, exercising daily for 20-30 minutes, trying to eat healthy and remembering to be kind to yourself

Our Helping Hand service gives new customers more than they might expect with access to a range of hand-picked early care medical services, so they have the help and advice they need to stay fit and healthy and improve not just their heart health but also their overall mental and physical wellbeing.

Supporting your clients’ heart health

New clients can find out their heart health score with access to PAI (Personal Activity Intelligence). They can link their wearable devices to measure the impact of physical activity on the heart. Find out more

Exercising daily

By using TrackActiveMe, a physical wellbeing app new clients can chose from a range of programmes based on their age, exercise habits and type of work to help mobilise and strengthen their bodies. Programmes include low impact Pilates, Yoga, stretching and strengthening. Find out more

Be kind to yourself

Thrive: Mental Wellbeing is an app available to new clients that offers personalised advice to help improve their mental wellbeing. Find out more

Advice to stay healthy

New advised protection customers have access to Health Hero which offers 24/7 access to virtual GP consultations by experienced, NHS doctors. Find out more

The Money Marketing podcast series

Listen to the Protection & Wellbeing series in association with Royal London on the benefits of wellbeing services as part of a protection plan. Listen now

Mansfield Building Society

JBSP makes a real difference for landlords too

Tom Molloy, Intermediary Sales Manager, Mansfield Building Society

It’s no secret that life can be tough for a would-be first-time buyer. House prices have risen at an incredible rate since the start of the pandemic, making purchasing a home more challenging, even before you consider the difficulties wannabe homeowners can face in building a sufficient deposit.

It’s little wonder that so many buyers have had to turn to help from their friends and family in getting onto the housing ladder (and, truth be told, lenders have been creative and innovative in designing products to accommodate this need for family support). A perfect example has been the rise of products such as joint borrower sole proprietor (JBSP) mortgages.

At The Mansfield, we have seen first-hand what a valuable tool JBSP mortgages can be for those taking their first step onto the ladder, and its popularity amongst brokers and borrowers alike. However, JBSP can be utilised in far more ways, not just to support struggling first-time buyers, especially if, like The Mansfield, lenders extend this flexible approach to other lending segments.

Indeed, JBSP can be an excellent option for landlords too.

A different approach for landlords

JBSP and the buy-to-let sector may seem like odd bedfellows at first glance, but in practice this form of lending can prove incredibly useful.

For example, some lenders may subject first-time landlords to higher interest rates and more costly fees to counter-balance the risk involved, with the borrower paying the price.

However, that would-be landlord can sidestep this issue through a JBSP mortgage, should they purchase alongside a parent or loved one who is already involved in the rental sector.

There can be tax benefits too. Take a married couple, where one partner is an additional or higher rate taxpayer, while the other pays the basic rate of Income Tax, or is a no-tax payer. Through a JBSP mortgage the couple may be able to purchase a buy-to-let property in the name of the lower earner, ensuring a more tax efficient return on their investment.

Flexibility pays dividends

Using JBSP for buy-to-let is a useful example of how a more flexible approach from lenders can help more clients access the funding they need. There’s nothing necessarily complex about lending in this way, and yet some lenders take such a prescriptive approach to their criteria that they would not even consider it.

In fact, all too often lenders are happy to turn away from cases where there is any perceived complexity, whether that’s the client’s employment status, income streams or the nature of the property used as security. This is unnecessary though – there are perfectly good borrowers, with acceptable circumstances, who are unfairly denied funding because of the rigid attitude of some lenders.

At Mansfield Building Society, we pride ourselves on doing things differently, and that means embracing a more flexible and versatile approach to assessing cases.

Rather than look for immediate red flags that allow us to say no, our underwriters are encouraged to get to grips with the nuances of each case so that they better understand borrowers as individuals and what they are looking to achieve.

We firmly believe that advisors value lenders that go the extra mile and that by being more flexible with cases (which might ordinarily be labelled as ‘complex’) we will win the hearts and minds of brokers now and for the long term.

A common sense approach

Joint borrower sole proprietor lending is available across The Mansfield’s standard range of residential and buy to let mortgages. You can find out more about product availability at mansfieldbs.co.uk/intermediaries.

If you’ve got a case on your desk that requires a common sense approach to lending then please pick up the phone to our Broker Support team on 01623 676360 or visit https://www.mansfieldbs.co.uk/intermediaries/.

Legal and General Protection

The need for protection

With people living and working for longer, we’re making changes to our critical illness products to meet the changing need for protection.

You’ll be able to offer longer policy terms on all our critical illness products. In doing this, you can help us support more people and ensure they have the required cover in place.

- Increasing the maximum policy expiry age, from their 70th birthday to their 75th birthday

- Increasing the maximum policy length, from 40 years to 50 years

The need for protection

Financial commitments are encroaching further into our later lives, and because we’re living longer, periods of ill health could interrupt the reliable income needed for later life financial commitments.

That’s why it’s important to ensure your clients have the required level of protection, should the worst happen. Critical Illness Cover provides your clients with financial breathing space so they can focus on what’s important – their road to recovery. And now it’s there to protect even more people, for longer.

Find out more about our critical illness offering and how it can be tailored to suit different budgets and needs.

West One

Financing a holiday let

Our specialist buy-to-let product range is available for existing or first-time landlords wishing to finance holiday lets in their personal names or through a limited company SPV.

Key features of our Holiday Let mortgages:

- We lend to first time landlords with no holiday letting experience.

- Available to individuals, limited companies, and expats.

- No minimum income.

- We can accommodate short term lets and serviced accommodation (Airbnb) which means the property does not have to be in a typical holiday destination.

- Holiday lets are assessed on an AST rental basis.

- The property must be suitable for standard AST rental.

Find out more about our approach to holiday lets in this short video: https://www.youtube.com/watch?v=GRPvxZNSWgY

To discuss a case or register as an introducer please get in touch with the West One team here: https://www.westoneloans.co.uk/buy-to-let-mortgages#introducer

Lendinvest

How lenders can make Buy-to-Let remortgaging simpler

With a busy year ahead for the Buy-to-Let remortgage market, our Director of Buy-to-Let looks at how lenders can make every remortgage deal simpler.

Vantage Finance

Your Trusted Partner in Expat Buy-to-Let Mortgages

As borders reopen and covid restrictions ease brokers are experiencing a notable increase in expert mortgage enquiries. However, the number of lenders offering suitable products is relatively small so placing these cases can be a challenge for brokers.

This is where Vantage Finance can help, our extensive lending panel stretches across the high street, challenger banks, specialist lenders, and private banks, offering you unrivalled access to a wide range of products and rates suitable for your expat clients and foreign national landlords.

If you have a question or a case, you would like to discuss then please do not hesitate to get in touch with the team at Vantage:

T: 01753 883195

E: enquiries@vantagefinance.co.uk

W: https://www.vantagefinance.co.uk/

Gatehouse Bank

Reduced Buy-to-Let Rental Rates for new customer applications of £500k or more for a limited time

We are delighted to announce that from Wednesday 2nd March Gatehouse have introduced a Limited-Edition range of £500k and above Buy-to-Let (BTL) finance products with a rate reduction of 0.5% and a fixed fee of £5,000. This offer, which applies to our 2 year and 5 year fixed term products, is available for a limited tranche of funds and extends to all BTL customers including HMOs and MUFBs where applicable.

Please note that these Limited-Edition products could be withdrawn with no advance notice once the allocated tranche of funds is utilised. You should therefore submit your fully packaged applications as soon as possible as only applications that have been submitted, signed by the customer and received by the cut off time will be accepted.

Our product range is available to UK residents, UK Expats, International residents and UK registered corporate entities looking to purchase or refinance property in England and Wales. Our full range of products can be found here.

If you have any queries or require further information our team remains available via phone and email, details of which can be found here.

The Mortgage Lender

Buy now, regret later?

Buy now, regret later? Read how this fast-growing phenomenon is impacting mortgage applicants.

Findings include:

- The history and growth of BNPL

- The pitfalls for customers

- What the government plans to do and when

- How you can help your clients now

Read the full article: https://themortgagelender.com/content-hub/broker-guidance/buy-now-regret-later

Precise Mortgages

How top slicing could support your buy to let customers

Top slicing enables customers to use surplus portfolio and/or earned disposable income to prove they can meet any financial stresses, rather than using the rental income of the property alone.

It’s available across all of our buy to let schemes, which includes limited company, personal name tax structures, portfolio and non-portfolio.

Helping your landlord customers secure the loan size they need, we’re on the case.

- Allows landlords to meet the rental cover calculation for short-term products

- Greater flexibility around loan size

- Provides access to properties with lower rental yield.

- Offered across our entire buy to let mortgage range

Skipton For Intermediaries

Skipton Talks is back for a brand new series

We’re really excited to announce that our popular webinar series, Skipton Talks, is back with four brand new episodes. Only this time, they come in the form of podcasts which you can listen to on your favourite streaming service!

Our regular hosts, Rachael Hunnisett and Derek Adams are joined by experts from across the intermediary mortgage market to discuss topical issues and hopefully make your job a little easier in the process.

Don’t miss an episode

- 8 March – Skipton Talks on International Women’s Day

On International Women’s Day, Rachael is joined by our Senior Mortgage Product Lead, Jen Lloyd, to talk about their experience as women rising the ranks in the mortgage industry, and why more female representation at a senior level is so important.

- 15 March – How great client services create lasting client relationships

Shelley Walker from The Mortgage Mum speaks to Derek about how they approach service in their business, and what they expect from us as a lender. Including useful hints and tips on making the most of social media, customer testimonials and podcasts.

- 22 March- The New Build market: how we got here and what comes next

Rachael chats all things New Build with Craig Hall from LSL Property Services. They talk about pivotal moments in the history of the New Build market and we get Craig’s expert take on what we can expect next in the industry.

- 29 March – A focus on Joint Borrower, Sole Proprietor

Learn about our Joint Borrower, Sole Proprietor Scheme, as Derek speaks to BDM Tracey Nash and Underwriting Lead, Charlotte Raw about our JBSP proposition. Find out how it could help your clients in different scenarios, including divorce and friends helping friends.

Subscribe today

It’s never been easier to keep up to date with our latest news and views on the intermediary mortgage market. Listen at home or on the go and don’t miss an episode when you subscribe to Skipton Talks on your favourite streaming service.

Metro Bank

Mortgages for those with a less than perfect credit profile

MORTGAGES FOR THOSE WITH A LESS THAN PERFECT CREDIT PROFILE

If your customer has a less than perfect credit profile, they may still be eligible for a product from our Core Range – subject to application score and full assessment.

We can look at a customer with:

- £500 of unsatisfied CCJs or defaults

- £1000 of satisfied CCJs or defaults within the last 3 years. No limit if satisfied over 3 years ago

- Missed or late payments if they don’t exceed a status 2

- Settled IVAs, arrangements or debt management plans

- Discharged bankrupts as long as 3 years has passed since the initial bankruptcy order

- Repossessions accepted after 6 years

Great news… If your customer doesn’t meet the requirements for our core range, they may still be able to proceed on our Near Prime Range.

For full details on the points above and our full near prime lending criteria please refer to our Lending Criteria Guide and Product Guides. All cases are subject to full assessment and a credit score pass.

Contact us

Our BDM Team are here and available to help with new case queries. Please get in touch with your BDM or call our Broker helpdesk on 020 3427 1019

Foundation Home Loans

How we are turning ‘Generation Rent’ into Generation Buy’

The Government’s Levelling Up White Paper focused heavily on the housing market, specifically looking at what it might do to turn, in its words, ‘Generation Rent’ into Generation Buy’. Here’s how we are part of that movement to increase the number of first-time buyers in every region of the country.

You said, we listened… How we have improved our communication with brokers

You told us your preferred channel of communication with your Foundation regional account manager is via the telephone, closely followed by Teams or Zoom calls – Here’s how we have changed our process to meet your needs. Click here to read the full story.

Swap rates changing – how we are working with you

In our market, rates and product pricing are always going to be a major discussion area and a constant point of attention, not just in terms of what is happening in the here and now but importantly, what happens over a number of time horizons.

Guardian

HALO – It’s shining brighter than ever

We’ve added a neurological support partner to our claims support service, HALO, so our claims service now takes even better care of your clients

HALO, the claims support service that’s as unique as each claim

We all know that a payout alone is rarely enough when families make a claim. So, we’ve strengthened our claims support service, by partnering with Krysalis, a consultancy that provides specialist therapy for people diagnosed with neurological conditions.

As around 1 in 6 people in England* have a neurological condition, you can imagine just how valuable this is to your clients. It can make a real difference to people living with Parkinson’s or motor neurone disease, and to those who have suffered a stroke or injury to the brain, spine, or central nervous system.

The impact of a neurological condition can be huge, both for the person affected and for those closest to them. We want to help critical illness claimants live the best life possible following diagnosis of a neurological condition, and we believe adding neurological support to our HALO claims service helps us do this.

*Source: neuro-numbers-2019.pdf (neural.org.uk)

Together with our other partners, Legacare and RedArc, they allow us to provide policyholders and their immediate families with a broad range of medical, legal, and financial support services.

Pure Retirement

Your February Update: New Resources, and Upcoming Events To Support You

Welcome to your monthly Pure update, a collection of business news and resources spanning the last month. As we continue to support you in helping your customers achieve the retirement they deserve with our lifetime mortgage solutions, we wanted to give you a chance to catch up on anything you may have missed.

Our New Quarterly Report

Our latest quarterly report is now live, bringing you the key headlines over Q4 in terms of customer demographics, consumer habits and market updates.

The latter half of the year contributed heavily to a record year for the sector, so why not have a look at some of the key factors that contributed to it, and what it could mean for the later life lending market in 2022.

Illuminating The Journey Into Later Life

As lifetime mortgage specialists, we’re dedicated to ensuring that neither you, nor your clients, are left in the dark.

Click here to learn more about what we stand for and how we can support you – whether that’s through innovative products, our resources to help you make the most of the market opportunities, or by supporting your customers throughout the mortgage term with our first-class follow-on care.