Protection special edition of TechTalk

Get the latest technical support in our Protection special edition of TechTalk.

Track your online applications using the LV= Protection Progress Hub

The LV= Protection Progress Hub is an easy and convenient way to track the progress of your applications 24/7, providing you with key information that’s refreshed every 15 minutes, saving valuable time and making it easier for you to do business with LV=.

Not only can you check the status of applications, you can also add a start date and add or amend client bank details, as well as downloading acceptance terms documents.

There’s also a simple Collection Date Calculator that works out the first two premium collection dates.

All you need to do is use your Fastway quote and apply login details to access the Hub.

Not registered yet? Just email or call the LV= agency team who will set you up.

If you have any questions or comments please visit the LV= Adviser Centre, contact your usual LV= Account Manager or call 0800 032 4219.

Mortgage Vision is Now On-demand!

In March 2021, Mortgage Brain delivered a series of Mortgage Vision Masterclasses, packed with thought-provoking and insightful presentations from a variety of industry leaders. Following fantastic feedback, they have made several of the masterclasses available on-demand for free.

Each masterclass was delivered by an industry leader who provided engaging and valuable market insight on topics including

- Navigating the everchanging policy and criteria

- An in depth look at adverse credit

- Self-employed insight

- Underwriting and credit risk

You can read more about each session, find resources, and view the masterclasses on-demand here.

Build a Growth Mindset with Source

Source Insurance has announced a new week-long series of free ‘Lunch and Learn’ sessions to coincide with Learning at Work Week from Monday 17th to Friday 21st May.

Learning at Work Week launched in 2009 and has grown each year so that it has now become the biggest festival of workplace learning. Co-ordinated by Campaign for Learning, this national week aims to develop a culture of lifelong learning at work.

Along the theme of ‘lifelong learning at work’, these bite-size sessions have been created to help brokers towards building a growth mindset and making the most out of their business.

“Advisers talk to us about what they feel they need additional help and support on. Some of the common things are the softer skills like time management and cross-selling of ancillary products. This series of modules will be really useful in providing tools to help with a broker’s business.” – Lee Denton, Associate Sales Director at Source Insurance.

Topics include:

- Building Rapport – How do you create a meaningful connection with your customers?

- Cross-selling Skills – How do you boost your income?

- Objective Setting – How can you achieve your goals?

- Time is Money – How do you manage your time effectively?

- Personal Resilience – How do you positively embrace change?

- Networking Skills – Who do you need to know?

Source Insurance has always had a keen focus on lifelong learning, both internally and externally, which is why ‘supportive in how we educate’ is one of their core values. They are committed to facilitating and encouraging professional development for all Source staff. Source are passionate about supporting this same culture of continuous improvement with their brokers, by providing the LearningLab, a first-class Learning and Development scheme.

“I always encourage people to study… it just takes work, determination and commitment. Never think you know it all, and be willing to listen and learn. Take the risk and give it a go – perseverance leads to success.” – Tania Frowen, Managing Director of Source Insurance.

With a mixture of webinars and interactive workshops, brokers will be introduced to a range of tools they can utilise to hone their interpersonal skills and help them to enhance their sales process.

While it’s vital for brokers to stay up-to-date on industry legislation they should also be honing their soft skills. Many companies offer training on the latest regulatory changes, including Source themselves, while soft skills are less catered for. By honing the personal skills needed to interact with their customers, brokers will be assured they are providing the best service possible and building lasting relationships in turn accelerating their business.

These sessions are FREE for all mortgage and insurance brokers. However, sessions are limited, so register now to secure your space.

To learn more, click here.

Why landlords should turn to bridge-to-let finance ahead of the Stamp Duty Deadline

With another Stamp Duty Deadline approaching, the Director of Underwriting at LendInvest explains why landlords should turn to Bridge-to-Let finance to secure their next property ahead of the deadline.

I is for Improved Services

Great news, we’ve increased our conveyancing panel meaning you can now choose a preferred solicitor for your BTL clients.

We understand how important it is for you and your clients to work with a solicitor you know and trust, so we’ve joined forces with Lender Exchange to make this possible. Because we’ve just launched, the number of approved conveyancing firms available is small but will grow over time.

To see if your preferred conveyancer is currently on the Zephyr panel go to Lender Exchange.

Solicitors not yet on our approved list may submit their information for consideration via Lender Exchange.

Conveyancing panel information

Give Zephyr a try to see how we’ve got BTL covered from A to Z.

Find your BTL expert by region | Call 0370 707 1894 Mon-Fri, 9am-5pm

Straightforward approach to limited company cases?

Solution Found.

Highlights of our approach to limited company BTLs:

- We accept up to 4 directors

- We consider expats on limited company applications

- We are good at dealing with complex company structures

If you think our straightforward approach to limited company buy to let could help your clients, register today and let’s get started.

Meeting the changing needs of landlords

When it comes to product choice, Buy to Let has bounced back faster than the residential market since the start of the pandemic. According to Moneyfacts, in March, the number of Buy to Let products available rose for the fifth consecutive month to reach 2,333, which is the highest level since the same time last year.

This increase means that the Buy to Let sector has now recovered to 81% of pre-pandemic levels, while the residential market has reached 68% of the number of products available before the pandemic.

However, in this competitive market, rate isn’t the only battleground. Moneyfacts says that the average for both 2 and 5-year fixed rates is higher now than it was this time last year. So, how are lenders standing out against the competition?

At Pepper Money, we have recently made enhancements to our Buy to Let range. While it is always important to be as competitively priced as possible, our key focus was to deliver a proposition that better meets the profile of landlords.

One way of doing this was by lowering our minimum income requirement for individuals buying in their own name from £30,000 to £18,000. We understood that for a growing number of landlords, their Buy to Let income represents a significant proportion of their overall income. Managing a portfolio can take a lot of time, and often property investors may only work part-time or have limited additional income alongside their income from being a landlord. So, by reducing our minimum income, we are opening up our products to a broader group of potential customers.

We also increased our maximum LTV on some products, for landlords who want to make more of their capital by maximising their leverage. We introduced a whole new limited edition product line for customers who haven’t had a CCJ, secured missed payment, or Default in the last 60 months, called Pepper 60. This is a product unlike anything else in Pepper Money’s product range at the moment. Our maximum period for CCJs, secured missed payments and Defaults on other products is currently 48 months, but we recognised that the majority of landlords maintain a strong credit profile and, while some experience slip-ups, the proportion of landlord customers with recent missed payments is far lower than the residential market. So, by extending our product range to landlords without credit blips in the last five years, we can offer lower rates, even at 75% LTV.

However, product development isn’t just about rate. Cost is clearly a factor, but so too is criteria and, often it’s the small criteria changes that open up a mortgage range to a broader group of customers. Ultimately, it’s about helping you to find solutions, and so we will continue to work with brokers to continually improve our products to meet the changing needs of customers.

Caroline Mirakian, Head of National Accounts, Pepper Money

Helping your clients throughout 2020

People always say it’ll never happen to them but L&G’s claims statistics show the reality is, illness and death can hit clients and their families at any time. They’ve broken their claims statistics down by product, customer profile and top reasons to support your conversations and reaffirm the importance of having the right protection in place should the worst happen.

They’ve also provided you with the tools and advice regarding the reasons why claims are rejected and the importance of Check Your Details (CYD) to ensure all your clients stand the very best chance of having their claim paid.

Read L&G’s magazine here.

Visit their dedicated page.

High LTV for Home Improvements and Debt Consolidation

Don’t be constrained by LTV – 2nd Charge loans are available for home owners, right through to 100% LTV, from The Loans Engine (TLE).

Typical uses:

- Any Home Improvements

- Debt consolidation

- Repay bank of Mum and Dad

- Deposit for BTL or holiday home

- Tax Bill

- Any other legal purpose

A typical example:

You helped your clients move home. They would now like to renovate the property to their own taste – new kitchen/bathroom/windows, etc. You can’t remortgage or access a further advance, because you’re constrained by LTV or lending policy.

TLE can recover/release your client’s equity from the property, right through to 100% LTV if needed, and a valuation is unlikely to be required, (in most instances TLE will use a desk-top valuation/AVM).

What’s more, affordability is assessed using income and outgoings.

Call TLE on 0800 032 9595 to help your clients access the funding they need.

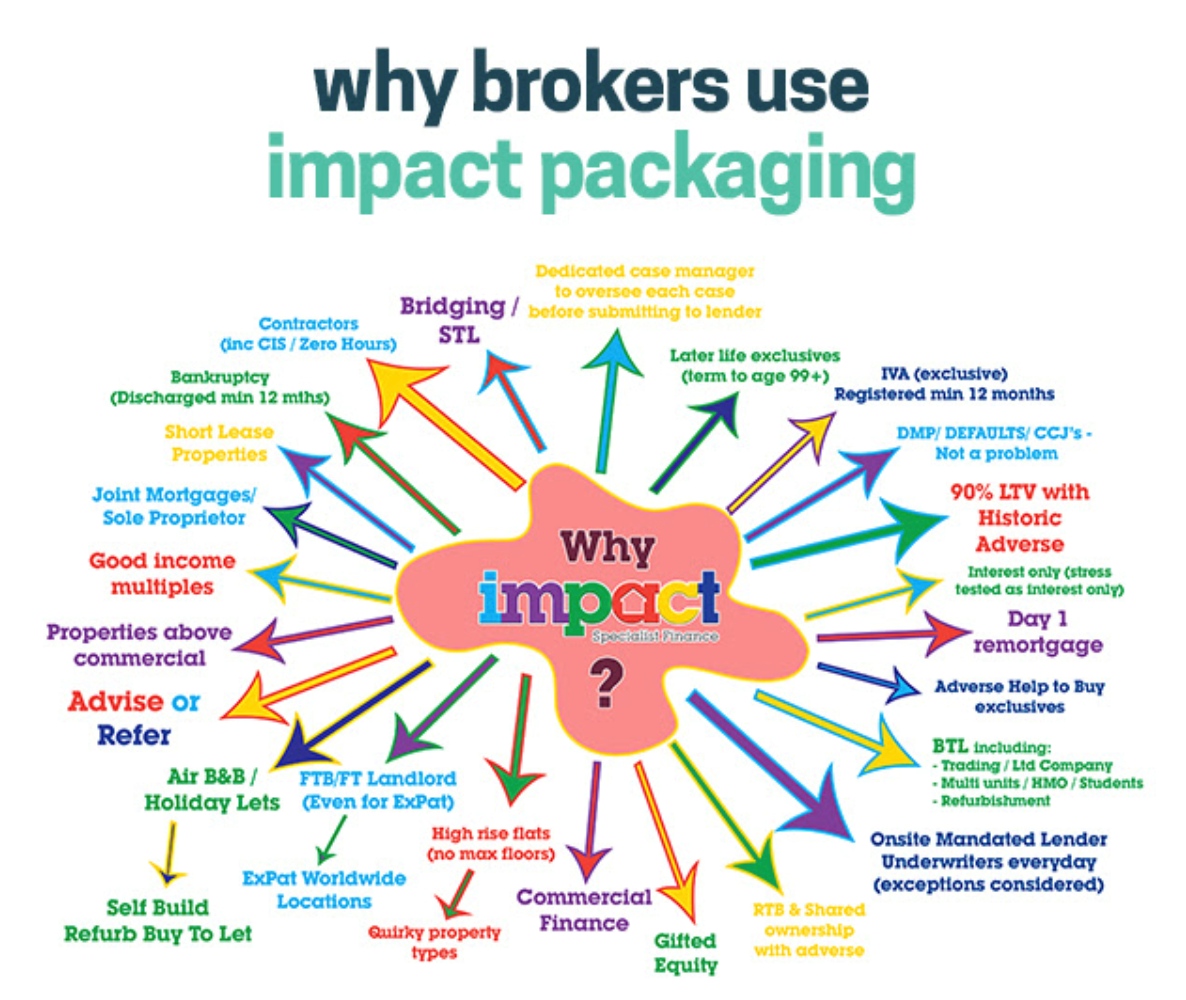

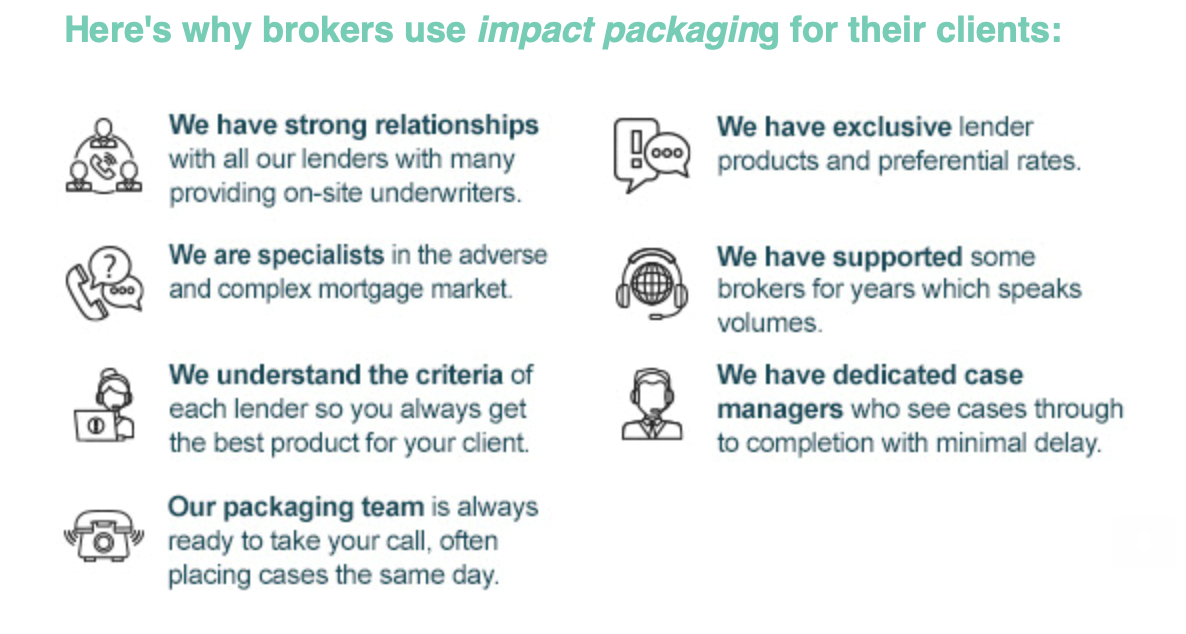

Impact packaging – for all things specialist

Impact Packaging is an award-winning, market-leading mortgage distributor and packager built on 30 years of experience and a reputation for quality and service.

Our packaging team has a wealth of experience assisting mortgage intermediaries in the placement of their cases. With strong lender relationships, impact can provide access to both exclusive products and on-site underwriters, helping ensure you are getting the best deal for your client as quickly and easily as possible.

Flexible lending up to 90% LTV for house purchase

We’re delighted to now be offering a mortgage up to 90% LTV, because for us it’s more than just the product features – it’s about how you can utilise our flexible criteria and ‘can do’ approach to mortgage lending which really makes the difference. Options available include:

• Up to 4 applicants

• Gifted deposits

• Guarantors

• Joint Borrower Sole Proprietor lending

Available in England, Wales and Scotland (subject to postcode restrictions in Scotland), for full product details, find out more below.

2 Year Discounted Rate House Purchase Only – DID147

|

Tool shows if cashbacks could benefit your lifetime mortgage clients

Do you have lifetime mortgage clients who want to reduce interest rates or maximise funds?

Our cashback calculator can help you see if they could benefit from our flexible cashback feature.

We’re right movers and shakers

We’re excited to become one of the first lenders to use enhanced automated valuation data (AVM) technology and the latest application programme interface (API) with Rightmove.

In practical terms, that means more of your residential customers will benefit from an automated valuation at the point of application and may be able to receive day-one offers (as long as the case has been properly packaged.

The technology gathers data from more sources too, which means your clients can take comfort in the knowledge that they’ll have the most up to date mortgage valuation for the property.

Rightmove

“By moving to our enhanced Automated Valuation Model, Skipton are benefitting from the increased accuracy, consistency and functionality that the new model offers, pulling in millions of data points from our property database and surveyor data records. Rightmove is committed to restless innovation and making home moving easier across the UK, and we’re excited to begin this roll-out of our new and improved tool.”

Karen Appleton, Head of New Lending, Skipton Building Society

“One of the ways we’re Making Things Easier for You is by combining the latest technology with the human touch, and working with Rightmove will help us achieve that. We believe the AVM and API technology will help us provide a faster more accurate service to you and your clients.”

Improved Process and streamlined proposition

We are constantly listening to our Intermediary Partners and have recently made the following changes to help improve our service to you and your customers:

- Removed the requirement for customers to declare whether they have previously been furloughed

- Halved our mandatory document and shopping list requirements resulting in less documents required for decisioning

- For example, removing the need for bank statements to support every case – these will only be requested when our Underwriters feel they are absolutely necessary

- Streamlined our proof of residency address requirements, by only requiring evidence of the applicant(s) current address

- Simplified our SPV criteria

- Scrapped the standard need to verify income on FTB/FTL Buy to Let applications, up to 80% LTV

- Stripped back our documentation requirements

All of these will result in much quicker and more consistent decisions for you and your customers.

But we haven’t stopped there. There are a number of other changes being planned to improve our service to you, so watch this space for further details. And keep an eye on our website where we update our service levels daily, so you can see exactly how we are doing.

Please call one of our Telephone BDM’s today on 03300 246 246 to see how we can help you.

Two key appointments represent the ‘perfect combination’ for Darlington Intermediaries

DARLINGTON Building Society has made two key appointments to strengthen its relationships with mortgage brokers across the country.

Amanda Smith and Sarah Rose have become Business Development Managers with Darlington Intermediaries, which was given its own brand by the Society two years ago as part of its drive to introduce mortgage solutions with increased flexibility.

And Chris Blewitt, who took over as Head of Intermediary Distribution at the start of the year, has described the appointments as “the perfect combination of experience, knowledge and connections”.

Changes to their lending to Non-UK Nationals criteria

- Maximum 80% LTV

- Applicants must have been resident in the UK for a minimum of 2 years (evidenced through Passport stamp or other immigration documentation) & working for this length of time.

- Have a valid UK work permit/visa with at least 2 years remaining.

- Employed applicants only and subject to UK tax

- Hold a UK Current Account

- The applicant(s) should be of a professional standing and working in one of the following sectors – Education, Healthcare, Finance & Banking, IT or Legal.

For EU, EEA (Including Iceland, Norway and Liechtenstein) and Swiss citizens, evidence that they have successfully applied for Pre Settled will be accepted – these will be subject to a maximum LTV of 80% and the criteria detailed above.

Where the applicant has been granted permanent rights to reside or Settled status (with permanent Leave to Remain) these are acceptable under our normal Underwriting Criteria.

Irish Citizens do not need a residence document as they have the right to reside and applications from Irish Nationals should be assessed on normal underwriting terms.

A series of blog features

As part of their commitment to providing first-class adviser support, Pure Retirement have rolled out a series of blog features designed to equip you with a clear understanding of the factors involved in lifetime mortgage lending.

The first instalment, by Underwriting Team Manager, Gavin Hancock provided a closer look into the Pure Underwriting Team and how they can help you achieve the best possible lifetime mortgage solution for your customers.

The next feature puts the spotlight on the Property Management Team, as Portfolio Manager, Michael Wrigglesworth introduces the team and the roles involved in engaging with a customer’s estate in the event of their death.

The series of posts concludes with a feature by Senior Comms & Editorial Executive, Gareth Ware on the latest customer and market trends, providing you with up-to-date expertise that could help you enhance your service to clients.