LATEST PARTNER BLOGS:

Paymentshield

Advise or refer? Ensuring the best possible outcome for your clients

TMA Club

Are Finfluencers putting your customers at risk?

Fleet Mortgages

BBR cuts should bring more competitive mortgage pricing

Lendinvest

Creating the future of BTL mortgages

Kensington

Our Low Deposit mortgage solutions

For your clients who are first time buyers and/or have a smaller deposit.

- Up to 95% LTV rates available

- Right to Buy up to 100% LTV of the discounted purchase price

- Shared Ownership 85%, 90%, and 95% LTV options, subject to affordability

- New Build up to 90% LTV of houses and flats, enhanced cashback for energy ratings of A or B (and C if BTL)

Kensington accept Gifted Deposits from immediate family members across all their products. If your client needs this, please complete their Gifted Deposit pdf.

Santander

MATS will be temporarily unavailable

Our Mortgage Application Tracking System (MATS) in Introducer Internet won’t be available from 7pm on Friday 26th April until 8am on Monday 29th April.

This means your brokers won’t be able to track mortgage applications, upload documents or upload/receive MATS messages.

You will still be able to submit cases during this time, however your brokers and their clients won’t receive any confirmation emails until Monday 29th April.

We’re sorry for any inconvenience caused.

Vida Homeloans

FTBs with adverse credit

Name: Katia & Lorenzo

Employment: Employed

Resi/BTL: Residential

Purchase/Remo: Purchase

Amount borrowed: £106k

LTV: 59%

Product: Vida 6 / 2 year fixed

Katia and Lorenzo want to buy their home

Katia and Lorenzo are first-time buyers who want to use the Right to Buy scheme to purchase their long-term home.

They had some adverse credit

Over time, the couple has built up a significant amount of adverse credit, including 5 defaults for Lorenzo and 3 for Katia due to recent redundancies. Once their employment was established again, they entered into Debt Management Plans to take ownership of their finances and get them under control.

Lending into Retirement

The loan term takes the oldest applicant to age 75, which meets our lending into retirement policy as they’re both under 50 and more than 10 years away from their anticipated retirement ages.

Evidence was obtained that they’re contributing to pensions, and the Vida later life lending form was received with supporting ID.

Onwards and Upwards

By taking a 2-year fixed rate, Katia and Lorenzo can continue to repair their credit history, with the aim of remortgaging at a more favourable interest rate in the future.

With the help of their Broker and Vida, they are finally able to get a Right to Buy mortgage on their home.

The Mortgage Lender

The FCA’s rules on consumer protection, and how they’ve settled in

In any business it’s good practice to prioritise the customer’s interests, and that’s particularly true of the financial services industry.

We welcomed the Financial Conduct Authority’s latest policy on Consumer Duty. But what are the new regulations, and what impact have they had on our day-to-day work?

Reliance Bank

We have Improved our Broker Registration Process

We have listened to your feedback and introduced a quicker and simpler Broker Registration Process to help Advisers onboard with Reliance Bank.

RBL Mortgage Operations Team now ask for the following items only:

- Proof of Professional indemnity insurance

- Due Diligence Questionnaire

- Signed Broker Terms of Business Agreement

- Mortgage Pack

We only register at Firm or Network level. Individual Adviser registration is not required once your Network or Firm has been onboarded.

Reliance Bank Mortgage Operations Team now have ownership of the Broker Registration Process which gives us more control and will help improve the onboarding experience.

Please complete and return forms via email to Mortgages@reliancebankltd.com ensuring that you attach a copy of your Professional Indemnity Insurance.

We do not accept electronic signatures.

Our standard SLA is 3 working days but should you have a case ready to submit, please do let us know.

Please refer to the Mortgage Pack (above) for information on how to submit a case.

Should you have any further queries, please contact the team on 020 7398 5422.

- Option 1 – New Business and applications currently in progress

- Option 2 – Existing Mortgage Enquiries (including registration requests)

Or email us at Mortgages@reliancebankltd.com

Legal & General

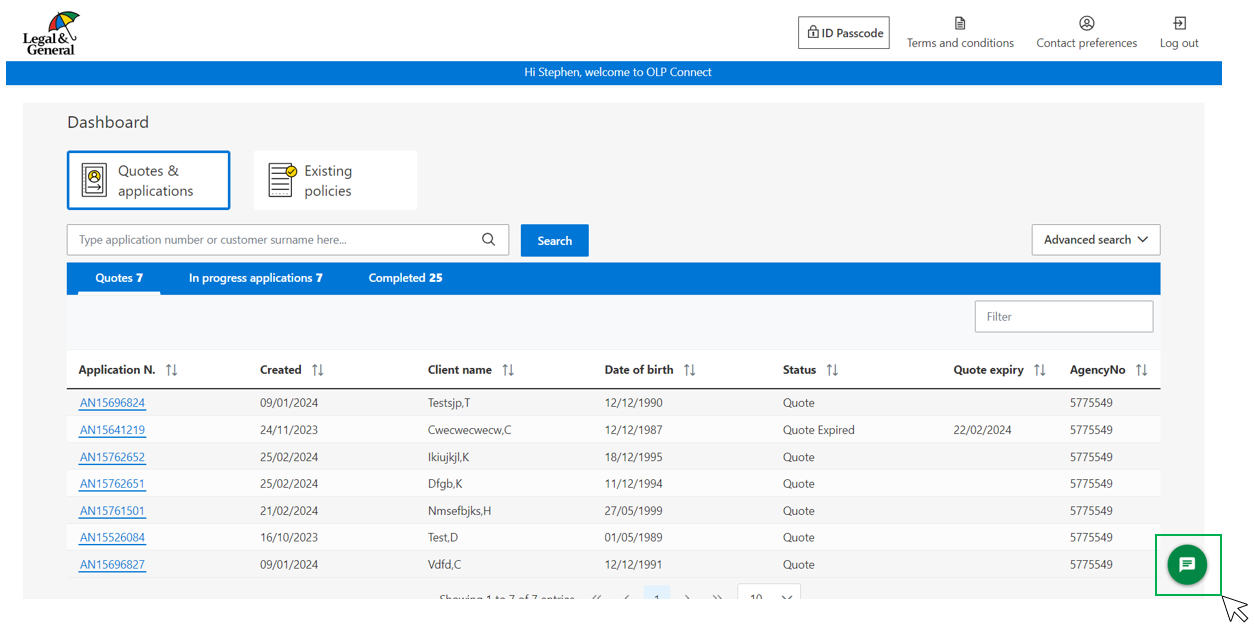

Your Virtual Assistant Gets a Fresh Look in OLP Connect!

Starting from April 29th, we’re introducing a fresh look for your Virtual Assistant in OLP Connect! Say goodbye to the old ‘Help’ button and welcome the smart new chat icon. It’s conveniently located at the bottom right of your screen. Simply click on this icon to access the same great features you’re already familiar with.

Our Virtual Assistant is here to assist you with a wide range of tasks, from pre-sale underwriting and new application queries to providing support for existing policy information and helping you find relevant documents.

Need to chat with us about a new or existing policy? Just click on ‘Live Chat’, and our Virtual Assistant will seamlessly connect you to our dedicated support team. Remember, Live Chat is available Monday to Friday, from 9 am to 6 pm.

Saffron Building Society

Maximising New BTL Opportunities in These Turbulent Times

The Buy to Let (BTL) market has experienced a vast transformation over the past couple of years – not only have landlords had to adapt to a far higher interest rate environment, but also the gradual withdrawal of mortgage interest tax relief, stamp duty land tax reform, cuts to the tax free allowance on capital gains and stricter mortgage underwriting rules. In response, we are seeing fewer landlords entering the market, with the total value of new BTL lending only reaching £6.3bn in the fourth quarter of 2023, a fall of 55.4% on Q4 2022, according to UK Finance.

Despite all this, market reports indicate that the BTL sector is still growing, with existing landlords now looking at different ways to grow their portfolios to navigate the challenging market conditions. In response, lenders are adapting to focus more on complex, higher value business. Particularly as inflation continues to fall, lenders are offering more attractive rates and criteria on BTL products tailored for limited companies. Changing to a limited company structure can also be considered for those landlords who are suffering from cuts to the tax free allowance on capital gains; by operating their BTL properties through a limited company, landlords can decrease their tax liability.

Alongside this, we may see growth in EPC rating-linked mortgage deals that favour those with more energy efficient properties of ratings A-C – a move which could allow landlords to increase the return on their investments.

Some landlords have also found that they are able to maximize their rental income by investing in Houses of Multiple Occupants (HMOs) and Multi Unit Blocks (MUBs), which are able to cater to a growing band of university students, young professionals, and even elderly individuals looking to downsize.

As the market diversifies and landlords look to pursue these new opportunities, a greater value is being placed on products with flexible criteria. Brokers should be well versed to guide their clients on those available, with Saffron offering a range of flexible BTL products that are well suited to a myriad of scenarios. We offer Limited Company BTL mortgages for different borrower types, including first time buyers, portfolio landlords, and new special purpose vehicles (SPVs). Saffron offers lower ICR’s of 125% of the product pay-rate used for all “pound for pound” re-mortgages, irrespective of an individual’s personal tax position. We also offer Expat BTL mortgages, and in March we launched a new product for expat landlords which has a fixed £2,500 arrangement fee.

Despite the pressures facing landlords, the BTL market is undergoing a shift in focus as landlords explore new opportunities. By adapting and evolving, lenders can support borrowers looking at these avenues and stimulate growth in this important part of the housing and mortgage markets.

Zurich

Helping your clients when they make a claim

Our bereavement guide is designed to help your clients when they make a claim on their life policy, at what we recognise is a key moment of truth.

We know that losing someone close is incredibly difficult.

The interactive guide provides a range of useful information beyond the basics of simply notifying a bereavement to Zurich. It includes practical guidance and signposting to help them navigate the often-challenging process of who to notify and what to do, as well as providing a range of emotional support services to help those recently bereaved deal with their loss.

Our new guide features:

- A step-by-step guide to notifying a claim with Zurich Life Protection.

- How to get in touch with agencies like HMRC or DWP using the Governments ‘Tell us Once’ service.

- Useful information about Zurich Support Services and other charitable organisations who can provide emotional support when dealing with grief.

- Where to find guidance around probate, postal redirection, and things like pension tracing or death in service benefits.

- Signposting to organisations who can help when dealing with debts or support for funeral costs.

- A jargon buster of technical terms and what they mean.