WEBINARS ON DEMAND:

ROYAL LONDON

Business Health Check

LEEDS BUILDING SOCIETY

Shared Ownership

ROYAL LONDON

Business Protection

LATEST PARTNER BLOGS:

L&G PRO

Meeting Consumer Duty Obligations

FLUENT MONEY

Consumer Duty: Principle 12

FLEET MORTGAGES

Looking Ahead At The BTL Market In 2023

Paymentshield

Changes to our quote journey

Paymentshield’s optimised Home Insurance quote journey is already making a huge difference to those advisers who have used it so far. Allowing for speedier quotations and improved conversion.

Due to this success, we’ll be removing the option to complete a quote using the old Home Insurance quote journey from 30 June 2023.

This will mean when you log into our unique Adviser Hub, you’ll only see the option to start a Home Insurance quote using our new journey. Don’t worry, if you have any pipeline quotes, these will be unaffected.

If you still haven’t tried the new journey or would like to know a bit more about this newest development you can get in touch with our Sales Team on 0345 0615 700 or completing our contact us form

E.surv Chartered Surveyors

Green Watch

Each month e.surv Chartered Surveyors share their Green Watch, a round-up of stories and guidance on energy efficiency and sustainable practices. This month’s issue covers:

- Property Market

- Green Finance

- Retrofitting

- Overheating

- Action to Minimise Flood Risk

- Green Business

Click here to read and download the May 2023 issue of Green Watch

Foundation Home Loans

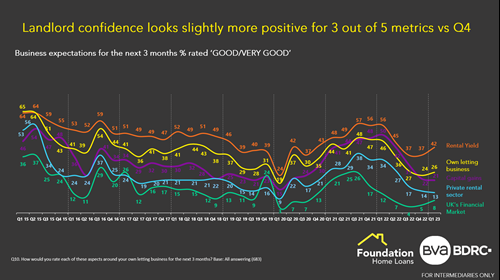

Rising landlord confidence and rising rents

As an intermediary-only lender, we fully understand the importance of the advice process, and this has become increasingly apparent in a buy-to-let marketplace which got that little bit tougher for landlords and a little lighter when it comes to confidence levels of the back of well-documented events over the later part of Q3 and early Q4 2022.

Thankfully, we are now benefitting from increased economic stability and some renewed levels of confidence. This was evident in the Q1 2023 BVA BDRC Landlord Panel report – brought to you in conjunction with Foundation Home Loans – which outlined that landlord confidence was up slightly when compared to Q4 2022.

Confidence was reported to have increased across 3 key metrics: rental yields (+5%) UK financial market (+3%) and landlord’s own letting business (+2%). Confidence in both capital gains and the wider private rental sector remained broadly stable.

Not registered yet? Register with Foundation today!

Confidence in landlord’s ‘Own Lettings Business’ also saw a slight improvement on Q4 data. Larger portfolios (11+ properties) reported the highest levels of optimism at 30%. Regionally, those in the South West are more confident about their lettings business at 33%.

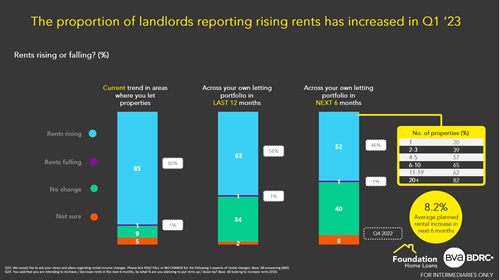

The proportion of landlords reporting rising rents increased in Q1 23. Landlords will also continue to increase rents further over the next 6 months. On average, rents will increase by 8.2%, although the smallest landlords (with a single property) will again seek the highest increases at 11.4% (up by 2.7% vs. Q4). Increased running costs continue to be the main cause of planned rental increases.

On a regional basis, landlords with rental properties in Wales are most likely to report seeing rents increasing at 90%, (slide 34) while landlords operating in Central London and the South East are most likely to have increased rents in the last 12 months. (slide 35)

The combination of rising confidence and the inevitable nature of rising rents is an interesting one for landlords, lenders, intermediaries and tenants. Many other factors are influencing the BTL market which is slowly picking up pace as greater levels of competition emerge and opportunities continue to present themselves for those landlords who are in this for the long haul.

Kent Reliance for Intermediaries

The home of handcrafted mortgage solutions

At Kent Reliance for Intermediaries we know that every case is different and whilst some lenders may not be able to help, we see the potential and cut through complexity.

Our strength lies in our flexible common sense approach with a willingness to consider cases that fall outside of our standard criteria.

Our underwriters individually assess each case enabling us to find tailored solutions for your buy to let and residential clients.

Landbay

Like for like remortgages featuring enhanced ICR

Maximise your clients’ affordability with our new Like for Like remortgages featuring a reduced ICR stress test and a variable fee structure.

These two-year fixed-rate products are for standard properties, available for trading companies, and come with a variable fee structure.

Please visit our website or contact your local BDM for full details.

Melton building society

SUPPORTING FIRST-TIME BUYERS

Mutual building societies have been helping people to buy a home for many centuries, and at Melton Building Society we strive to continue this well into the future. Here, we’ll explore how Melton stands out in supporting different types of applicants and the value we bring to their homeownership journey, starting with first-time buyers.

While niche criteria play a vital role, mutual building societies truly shine through their manual underwriting approach and common-sense underwriting principles. At Melton, we provide brokers with direct access to our underwriters, ensuring clear and seamless communication.

Precise Mortgages

Is your landlord customer worried about the increase in corporation tax?

Jon Hall, Group Managing Director at OSB Group, explains why most landlords don’t need to worry about the rise.

I can’t remember the last time there was an official Budget delivered that contained good news for buy-to-let landlords, and this year’s was no exception. The rise in corporation tax from 19% to 25%, initially proposed in last year’s Budget, then scrapped in September’s ‘fiscal event’, was reconfirmed in The Spring Budget and took effect on 6th April. The increase should draw much-needed revenue into the Treasury’s coffers, at the same time reducing post-tax income for a number of landlords holding properties in limited company structures.

Since George Osborne announced the phasing out of tax relief on buy-to-let mortgage interest payments in the Budget of 2015, it feels as though practically every year has brought new conditions making it harder for landlords to run a profitable business. Add in the current challenges posed by a huge rise in the cost of borrowing, and you can forgive buy-to-let borrowers for feeling the pressure.

But there is a silver lining to the corporation tax hike cloud: it is only likely to impact the very largest portfolio landlords. In fact, purchasing property within or switching an existing portfolio to a limited company structure is likely to remain a tax-efficient option for many property investors seeking tax-efficient strategies to galvanise their balance sheets.

Impact Specialist Finance

Residential Bridging available via Impact Packaging

Octopus are on hand if a client urgently requires finance, or they may have long-term refinancing in place, but need more time before their other lender is ready. They can also provide a loan on a property that your client lives in, plans to live in or cannot sell before completing a new purchase.

Residential Bridging Loan Highlights:

- Regulated & Unregulated up to 70% LTV

- Loans from £100k to £1m

- AVM (Automated Valuation Models) available

When can Octopus carry out an AVM?

- Regulated and Unregulated bridging

- Reduced legal due diligence

- Houses, bungalows and flats not within a block

- Open market purchase or refinance

Download Octopus Real Estate’s latest product guide

Take a closer look at Octopus’ product guide to help find a solution for your residential bridging cases.

Have a case you would like to discuss? Call the impact bridging team now on 01403 272625

The Nottingham for Intermediaries

Making it easier for contractors to secure a mortgage

The world of work is evolving at pace and as a mutual building society we’re committed to ensuring our mortgage proposition helps meet the changing needs of modern borrowers.

That’s why we’ve announced the first of a series of changes to our mortgage criteria, designed to help more individuals in their pursuit of home ownership. The changes will streamline the mortgage application process and expand eligibility for a broader range of borrowers.

The first changes go live today (21st June) and see us reduce the minimum length of time a contractor must have worked on fixed-term contracts in the same profession to just 12 months. In addition, there is now no minimum time required on their current contracts and contractors working via an umbrella company are acceptable, using 46 weeks income.

Click here to find out what The Nottingham have changed and why.

Vida Homeloans

The V-Hub 6 months on

When we launched the V-Hub at the end of 2022, we knew that providing rapid, direct access to decision makers would create a service proposition that delivered consistently elevated levels of broker support.

We wanted to create a service and experience offering that brokers could really put their trust in.

Following a strategic review, we looked in depth at the communication channels we had with our intermediary partners and listened to their feedback, which resulted in the launch of the V-Hub. Creating a centralised support hub and new engagement model was a bold approach but we recognised that providing direct access to underwriters was critical to be able to turn around our service, provide consistency and avoid miscommunication or processing delays.

Every colleague that we have in the V-Hub is fully trained and thoroughly understands our products, proposition, process, and our approach to underwriting. Intermediaries can now dial one main number, select option three and be put straight through to a mandated underwriter to get the answers they need quickly, easily, and accurately.

Zurich

Protecting IHT gifts with protection

As more estates face an inheritance tax liability, we are expanding the options available to help advised clients cover the cost.

A five-year deep freeze for many tax allowances and thresholds is putting greater emphasis on estate planning for those who face an inheritance tax (IHT) liability.

As advisers know, it is vital to forward plan. Various planning approaches can be used to help clients mitigate an IHT liability, from lifetime gifting to investing in assets that attract business relief and maximizing pensions, which can be passed on tax efficiently.

Another valid and frequently used option to address IHT is to make provisions to meet the liability. One effective way to do so is through a joint life second death insurance policy.

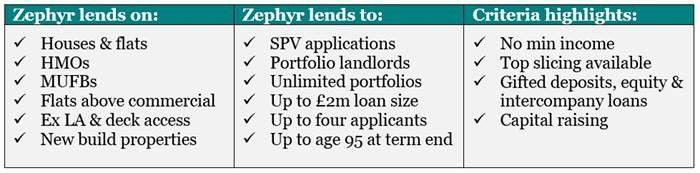

Zephyr Homeloans

Is it time to try Zephyr?

It was great to see so many brokers join the ‘Limited Companies’ Criteria Clinic on 12th June. If you were able to make it, we hope you found it useful and learnt something about Zephyr and the types of BTL cases we can help with.

Next time you have any queries give us a try! In the meantime, here is a bit of information about us.

As an award-winning specialist BTL lender, Zephyr can support you and your landlord clients.

At our heart is broad criteria for individuals and limited companies across a range of property types, including HMOs, MUFBs, new builds and flats above commercial. We can lend on large portfolios, like this example.

And with manual underwriting, provided by underwriters you can speak with, and a dedicated BDM to provide a helping hand, you will have peace of mind knowing your case is in safe hands.

But the thing that really stands Zephyr out is our people, who every day strive to provide the best possible broker service. Don’t just take our word for it though; 100% of brokers say they are happy/delighted with the service from our BDMs and Regional Sales Managers *

*Survey completed by 157 brokers who had a mortgage offer from January 2021 to May 2023. All brokers who answered the questions about their BDM/RSM gave positive scores.