WEBINARS ON DEMAND

ROYAL LONDON

What’s on the menu?

FLEET MORTGAGES

Who are Fleet Mortgages? BTL case studies

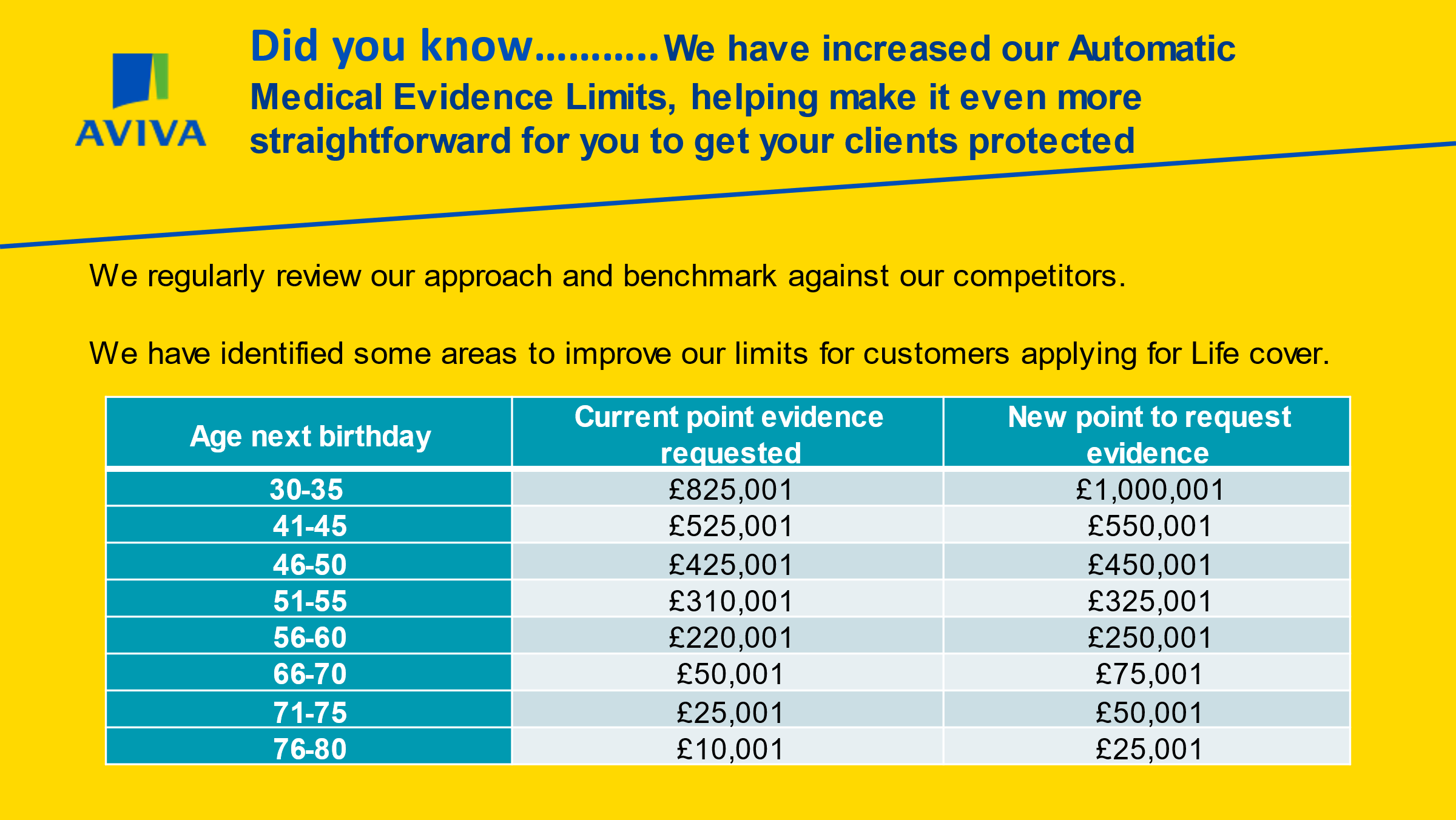

JUST

Making it personal

UPCOMING EVENTS

Last chance to register

We are down to the last few remaining spaces for our Face to Face workshop taking place in Watford next Tuesday, 5th April. Join Justin Hawes, along with four of our partners and a member of our compliance team for thought-provoking presentations, breakfast rolls and plenty of opportunities to network throughout the day.

5th April 9:30am – 12:30pm – The Village Hotel Watford

BLOGS

ACCESS EQUITY RELEASE

Why are so many people releasing equity from their homes?

ROYAL LONDON

Prioritising the protection conversation

HODGE

It’s time we stopped calling it Later Life

TMA Club

The New Build market: how we got here and what comes next

In this week’s Skipton Talks podcast, features New Build powerhouse, Craig Hall from LSL Property Services. He will remind everyone all of the key events that have impacted the New Build market since 2008.

And that’s not all – they also discuss the future of the market and what brokers should expect in the next few years.

About Craig Hall

An expert when it comes to the New Build market, Craig Hall is Director of New Home Financial Services at LSL Property Services. Craig has 27 years of financial services experience, having worked for some huge brands such as Barclays, Bradford & Bingley and Legal & General in several senior positions, across Mortgage Intermediaries and New Build.

Halifax

Changes to the Halifax Housing Price Index

To calculate the percentage loan to value (LTV) when a product transfer (PT) is required, we use an indexed valuation figure which is updated quarterly by the Halifax Housing Price Index (HHPI). Ahead of the next changes to HHPI, expected in April, we wanted to take this opportunity to remind you that our online PT process allows you to produce an instant quote and illustration for your client, however the process does not allow you to save an application and resume.

If the illustration is not progressed through to offer, any future changes to the HHPI may negatively or positively impact on the LTV and therefore product(s) available.

To ensure the product is secured for your client, a PT application must be progressed through to offer.

Visit us online www.halifax-intermediaries.co.uk

Santander for Intermediaries

Updated accountant’s certificate

To make it easier for your self-employed applicants we’ve updated the accountant’s certificate to capture more information upfront. It’s available to use on our website from Wednesday 30 March. The following updates have been made.

- New section (section F) which needs to be completed for all cases. The section covers the impact of Covid and if the applicant has an outstanding BBL or CBIL.

- New question needs to be answered if ‘Yes’ was ticked for Alphabet share structure.

- New drop down for accountant’s qualifications. Instead, they choose the professional body that awarded their qualification and tick to say whether they’re an Associate or Fellow.

What you need to do

Please continue to email the certificate to the accountant/client. The accountant will be able to complete it on screen, print it off, sign it and return it to you or your client. Please check the accountant has fully completed it before you upload it to MATS with your client’s other documents. Alternatively, the accountant can complete the certificate by hand.

We accept accountant’s certificates that are produced and signed by an accountant that has a qualification with a professional body we’ve listed in the lending criteria section of our website.

This new accountant’s certificate will be dated April 2022 and should be used straightaway.

Pipeline rules

We’ll continue to accept the old certificate (dated September 2020) on full mortgage applications (FMAs) already submitted on Introducer Internet by close of business on Sunday 10 April 2022. Any FMAs submitted from 6am on Monday 11 April will need to use the updated accountant’s certificate.

The Loans Engine

Clients looking to exit their development loan?

If your clients are looking to exit a development loan quickly, we may have the solution.

Our lenders have a range of fast, flexible borrowing options designed to assist clients in these circumstances.

Even more importantly, it doesn’t matter whether they’re looking to sell or keep their facility, there are options available for both.

Developer exit loans (sell facilities)

- Solutions from £200k

- Terms up to 12 months

- No limit on borrowing amount

BTL loans (keep facilities)

- Terms up to 5 years

- Solutions from £150k

- No ERCs in the last 2 years of the term

Call our team to chat through any case today. If we can help, we’ll happily speak with your client so you can focus on your core business.

West One

Providing a pragmatic approach to £2.9m BTL portfolio

Specialist lender, West One Loans has successfully completed a £2.9m, complex buy-to-let loan. Working with a landlord who already had outstanding mortgage balances of £7.3m, West One provided finance to purchase five standard residential properties and three houses in multiple occupancy (HMO) properties.

The eight properties were owned in the borrower’s personal name and the requirement was to transfer them into the limited company that had been formed to hold the portfolio. There were two other lenders also supporting the clients move from personal to limited company structure, benefitting from the portfolio incorporation relief rules.

“When it comes to financing large complex buy-to-let portfolios, selecting the right lender is crucial.” Explained Andrew Ferguson, Managing Director for the buy-to-let division at West One.

“For complex cases you need a safe pair of hands and at West One our individual approach to underwriting means that we review each case on its own merits, ensuring we support clients to secure the purchase or remortgage that they require in a smooth and timely fashion.” He added.

Find out more and read the case study in full here: https://www.westoneloans.co.uk/news/case-studies/a-pragmatic-approach-to-lending-securing-a-2.9m-buy-to-let-portfolio

Just

Faster Just For You Lifetime Mortgage applications on Air Sourcing

New link on Air Sourcing makes it quicker and easier to apply for Just For You Lifetime Mortgages.

Check that your Air Sourcing account is linked to a Just Adviser portal account, then you’re away: Do your rate comparisons, create KFIs and apply online.

Impact Specialist Finance

Fast solutions for a second charge loan

Are your clients looking to fund a short term loan? If yes, have they considered a Second Charge Bridging Loan?

A second charge bridging loan could be the ideal solution for those who already have a mortgage secured against their property but require further funds for a short period of time.

Impact SF has access to a comprehensive panel of bridging lenders, including limited distribution lenders. We have built strong relationships with these lenders who will take a view on all aspects of an individual case.

Access a faster bridging solution, call the Impact team on 01403 272625 or email bridging@impactsf.co.uk

Legal & General

A Covid-19 look back: How has the pandemic impacted UK businesses?

Two years have passed since the emergence of the Covid-19 pandemic in the UK. In early 2020, most of us could not have imagined what lay ahead.

In the face of incredibly difficult times, the country pulled together, the NHS re-confirmed their enormous value to us, and the power of protection came to the fore. For those who had it in place, or not, it made such a difference – for opposing reasons. Now, perhaps more than ever, society can appreciate that the unexpected could happen at any time.

Zephyr Homeloans

Remortgaging for Portfolio Landlords

Our Zephyr RSMs have been getting out and about in the spring sunshine and meeting brokers at events in Gatwick, Twickenham and Coventry. You can see where we will be next week at the bottom of this email.

On Tuesday our Product Range was refreshed, so make sure you check out our new rates. We also had a great turn out for our webinar, which saw our RSM, Elliot Newey, alongside our Head of Marketing, Tim Newman, and supported by Telephone BDM, Gemma Cauwood provide an introduction to Zephyr Homeloans and our buy to let mortgage criteria.

The session covered:

– Zephyr products and criteria

– Insights into underwriting

– How to submit business

– A live Q&A session

If you missed out you can watch the full webinar online now.

Help Zephyr Hit 1000 followers!

If you don’t already, know Zephyr’s LinkedIn page is really close to the 1000 followers landmark, please take the time to follow them on LinkedIn to help them hit their goal.

The posts they send out are a mix of product/criteria updates, thought leadership pieces and promotional messages, so hopefully you’ll find it useful to see what Zephyr is up to.

To see the Zephyr page, please click this link, or just search for Zephyr Homeloans next time you’re on LinkedIn.

Newbury Building Society

Quirky properties? They’re right up our street

If you have a client who is hell-bent on a converted church or has their heart set on a Grand Designs-style modern construction of glass and steel, you need to talk to a lender who can lend on unusual properties, a lender who is willing to accept these quirks.

That’s us! We can work with the quirks!

While unusual homes may represent a challenge to many lenders, we are happy to talk to you about lending on homes with something a little bit different…

- Properties with annexes or outbuildings

- Modern Methods of Construction (MMCs)

- Semi-commercial and multiple properties on one title.

- Converted properties – Churches, Shops, Pubs

- Listed and thatched properties

- Flying freeholds

- No maximum acreage

Don’t forget…

- Our instant chat service is available from Monday to Friday, 9am-5pm

- No credit scoring! All cases are assessed on their individual merit

- We can split mortgages (by term and / or repayment vehicle)

- Tailored, individual underwriting

- All types of incomes and a range of currencies considered.

Plus: Introducing a new secure and swift document submission service

Did you know you can now use our open banking service to send mortgage documents to us? This offers a more secure service, which will also save you and your clients time. When you place a case with us our team will send you a link.

Contact us today to discuss your requirements!

Vantage Finance

What are the benefits of using a master broker for bridging finance?

A master broker, like Vantage Finance, can save both you and your clients time when it comes to researching the bridging market and sourcing the best possible solution.

So why should you choose Vantage as your master broker of choice?

- 18 years of experience operating in the specialist finance market

- Strong partnerships with a panel of bridging lenders, with access to exclusive rates to us

- Through our experience, we have an in-depth understanding of lender’s specific underwriting requirements which can lead to quicker processing of applications.

- Effective, efficient communication throughout

- We offer a lifetime guarantee – if your client returns to us, you’ll always get a referral

- Applications approved in days, not weeks

Find out more about bridging with Vantage Finance here: https://www.vantagefinance.co.uk/short-term-and-bridging-loans

For any questions, enquiries, or cases you’d like to talk through, drop us an email or give us a call today.

T: 01753 883195

E: enquiries@vantagefinance.co.uk

W: https://www.vantagefinance.co.uk/contact-us

Central Trust

Listening to your feedback

Effective immediately the Portal will return and display the True Surplus Figure on each and every application based on our internal affordability model.

We hope that the enhancement to the portal will give brokers back their confidence in placing business with central trust, as they can now be certain of the affordability position of the applicant.

In addition to the above, where affordability may trigger the need for a Bank statement, the portal will automatically refer the application to the mortgage desk for assessment.

The mortgage desk will review the income and expenditure entered and will call you to discuss whether a bank statement is needed to move the application forward, or whether alternative documentation can be provided to evidence lower items.

I would like to thank you for your continued support and feedback in helping us improve our service and customer journey

If you have any questions please call the mortgage desk on 0800 980 6086 or email mortgagedesk@centraltrust.co.uk

The Loan Partnership

Lender panel, Selina Finance drawdown facility

One of The Loan Partnership lender Selina Finance have a second charge product with a twist !

They are on a roll with second charge products with great affordability underwriting. Have another look at Selina Finance’s USP’s and you’ll understand how they can help brokers convert more deals and increase revenue. Their service is still market leading and remains their main objective.

- Income multiples up to 6x based on nett disposable income

- No ERC on many plans

- Up to 130% LTV

- BTL 2nd charge 90% LTV

- 50/50 split on all fees & commission

- All 30 staff CeMap qualified, we give the advice

- Loans for any purpose

- Only 50% of cases need a valuation. Other 50% on AVM’s & drive by

- Self employed 1 year up to 100% LTV

- 3rd charges, shared ownership

- Adverse ignored after 12 months. Recent adverse accepted with a satisfactory explanation

- Fair fee scale

- Whole of market on second charges. New Selina limited availability Drawdown product, ideal for school fees

- Recent mortgage arrears accepted on a rate for risk basis

- Equitable charges can be used where consent for a second is a problem

- Follow us on Linkedin and Twitter to receive product updates as soon as we do

- Bridging with no ERC

- Any type of Commercial/ Semi Commercial/HMO/ BTL enquiry considered

- Call 01923 250090 or email info@theloanpartnership.co.uk . 9.00am-8.00pm Mon-Fri

Marsden Building Society

For Older Borrowers, because twists and turns happen – even in later life

We appreciate that, even later in life, your clients can go through major events such as marriage, divorce and children. That’s why we launched into the later life market to offer our expertise, supported by individual underwriting which is key to reviewing these types of cases. Below are some real-life examples of enquiries we’ve received and how we’ve been able to support them.

Meet Paula & Tom

Paula (56) has been living in her home for over 20 years. She’s currently working as a receptionist earning £18,000 per annum. She’s been dating Tom (64), who’s currently renting, for the last 5 years and they are now engaged to be married. Tom owns his own company and is a director drawing a salary of £42,000 per annum.

Paula would like to do the following:

- Remortgage her current £100,000 mortgage, adding Paul to it

- Borrow an additional £20,000 for home improvements

The property is worth £315,000 so 38% LTV. The clients would like a 10-year term on interest only. Tom also has a SIPP in the background worth £400,000.

What we said:

In this scenario we would insist that Paula sought independent legal advice regarding the transaction. In terms of income, we were able to accept Paula and Tom’s earned income plus 5% of Tom’s SIPP (£20,000). This gave us a total income of £80,000 and there were no issues with affordability. We were able to offer a 10-year term as Tom intended to continue working beyond state retirement age to 75. Due to the nature of his self-employment being IT related, we could accept earned income for this application on an interest only basis with downsizing as the repayment vehicle, as it was an acceptable option due to the minimum equity requirement based on region being met.

Meet Richard

Richard (62) lives in his unencumbered property but is going through a divorce. Staying in his home is important to him so he needs to remortgage to satisfy the divorce settlement. Richard works part-time at a school earning £9,000 per annum but he also has a private pension paying £24,000 per annum. The property is worth £250,000 so Richard needs to borrow £125,000.

What we said:

In this scenario we’re happy to accept the earned income up to age 75 due to the nature of his work, his plans to work beyond state pension age and 100% of his private pension. This gave us a total income of £33,000 so the case fit income multiples. As Richard’s outgoings were minimal, we had no issues around affordability. The reason for capital raising was acceptable to us so we were able to offer a 13-year term on interest only.

Meet Gail & George

Gail (58) and George (74) are married and have a 15-year-old son. Their existing mortgage has come to the end of its term and their existing lender won’t extend. They’d like to continue their interest only mortgage for as long as possible. They currently owe £80,000 and the property is worth £425,000. Gail is a house wife and George receives both state and private pension income.

What we said:

We understand that even in later life applicants may still have dependants we need to factor in for affordability. In this scenario, at 19% LTV we were able to offer Gail and George a 9-year term on interest only. George’s combined pension income totalled £35,000 so there were no issues with income multiples or affordability.

Got a case in mind?

Contact the Marsden’s Product and Intermediary Account Manager, Katie Broome, or call their Broker Support Team on 01282 440583*.

HSBC

Important changes to our residential lending policy

With effect from, Monday 4th April, we will be making the following changes to our residential lending policy:

Interest Only

We are reducing the sole applicant minimum income criteria for Interest Only applications from £100,000 to £75,000 per annum. For joint applications, at least one applicant must continue to meet the sole applicant minimum income criteria. Please note, minimum income excludes bonuses, commission, overtime and rental income.

Loan to Income (LTI)

We will be changing our joint income threshold criteria for applications with an LTV less than or equal to 90% from £40,000 to £50,000.

| LTV | Joint income | Max. income multiples |

| <=90% | <£50,000 | 4.49x |

| >=£50,000 to <£100,000 | 4.75x | |

| >=£100,000 | 5.50x | |

| >90% | All incomes | 4.49x |

Our Broker website will be updated shortly to reflect the above changes.

Further information

Chat with us or call our Broker Support Team on 0345 600 5847 (Monday to Friday, 9am to 5pm).

Manor Mortgages

Semi-Exclusive: 70% LTV BTL for UAE Ex-pats

We have an ex-pat BTL semi-exclusive meaning we can place 70% LTV BTL cases in the UAE, as well as Europe, USA, and many more.

Please submit any cases for UAE ex-pats before Monday 25th April.

- BTL up to max LTV 70%

- 5 year fixed

- £500 cashback towards legal costs for remortgages

- Applicants must be working for recognised large organisations that have a UK presence

- Must have a mortgage track record in the UK within the last 12m

- Customer must be a British passport holder or have permanent rights to reside in the UK

- Applicants must have a UK bank account

- Paid within 48 hours of completion

Royal London

Focusing on conditions that matter

We’ve improved our Critical Illness Cover by adding new definitions, and enhancing others to make protection simpler for your clients and really focus on the conditions that matter.

What you need to know

- Two new full definitions – Crohn’s disease and Syringomelia/Syringobulbia

- Three new additional cover conditions – Severe sepsis, less severe cardiomyopathy and less severe heart failure

- Five updates to existing full definitions – Bacterial meningitis, third degree burns, deafness, coma and chronic lung disease

- Two updates to existing additional cover conditions – Third degree burns and partial loss of sight.

- One update to an existing Children’s Critical Illness Cover definition – Spina bifida

Need more information?

Use our updated definitions search tool to view all of our Critical Illness definitions – including ABI+, additional conditions and child-specific conditions (available with Enhanced Children’s Critical Illness Cover).

Teachers for Intermediaries

Complex client income got you on the ropes?

With our experts in your corner there’ll be a knockout solution

Clients who are asset rich can often find it hard to secure a mortgage thanks to unusual income profiles, including these scenarios:

- Owning a substantial, high value property

- Having substantial cash, investments and/or pensions

- Recently completed a divorce

- Income from large maintenance agreement following divorce

Appearing to have low income relative to borrowing needs.

Helping those with a typical income shouldn’t feel like being on the ropes. Whatever makes their income unusual, we treat each applicant as they are – unique. TFI is confident in finding mortgage solutions for atypical clients. There’s no need to skate round obstacles – we can evaluate a variety of financial assets for income, using potential drawings on investments to boost their affordability.

UNUSUAL INCOME: PROBLEM SOLVED

We recently arranged a short term mortgage for a couple in their 70s looking to purchase and update the perfect retirement home, selling their current property at a later date.

State pension income was insufficient for affordability, but by monetising a SIPP worth £500k we created sufficient income, avoiding an expensive bridging loan and allowing them to purchase and then sell chain free.

KNOCKOUT SOLUTIONS

- Part repayment/part interest only solutions available

- Income from pension, savings, investments and property assets taken into account

- Bonus acceptance up to 75% LTV

- ERC free short-term lending also available

Buckinghamshire Building Society

Case Study 2 – Impaired credit

Derek has been living with his mother and is supporting her financially with everyday costs and her mortgage repayments. His mother Sally is a pensioner and Derek is a full-time HGV driver. Sally took out an equity release mortgage around ten years ago and together they have decided to remortgage and add his name to the application.

| House Price | 200,000 |

| Loan Required | 79,000 |

| Loan to Value (LTV) | 39.6% |

| Single Income | 39,000 |

| Income Multiple | 2.01 |

Whilst the applicants could comfortably afford to re-mortgage, Sally’s current mortgage was on a high interest rate. It had seen her initial equity release loan double over ten years. They were having trouble finding a new lender on a better rate due to Derek’s adverse credit. He had defaulted on some payments in 2017 during his marriage breakdown, but was able to demonstrate that these had either been settled or would be satisfied by date of application.

Although Derek had impaired credit, his history of re-paying this debt added strength to his application. He was already supporting his mother with every day bills and her current mortgage.

The Society was able to offer a lower interest rate which will see the mortgage paid off before he reaches retirement and puts both applicants in a more comfortable position in terms of affordability. Regular overtime offered to Derek in his job provided additional strength to the application.

At Buckinghamshire Building Society we:

- Manually underwrite, looking at each case individually

- Assess cases on affordability not income multiples

- Go above and beyond to find a solution to your cases

- Soft search at DIP stage based on credit search, not score

To find out more about our full product range, please visit www.bucksbs.co.uk/intermediaries/all/

Vida Homeloans

Self employed & contractors mortgage guide

As the lending specialist, we are here to assist all contractors, including those with a less than perfect credit record.

We have listened to your feedback and are pleased to announce a range of enhancements to our contractor criteria, to help get life moving for your clients.

Highlights:

> Enhanced affordability: 48x weekly rate for self-employed contractors

> Day 1 contractors considered where at least a 1 year track record of employment within same line of work

> CIS workers now only need to provide 1 year’s SA302 and tax year overview along with the last 3 months’ payslips or invoices

> All LTVs and Adverse Tiers available to contractors

Plus, reduced minimum time requirement in 2nd job down to 3 months

Please see attached our new Self Employed and Contractors Guide, and our updated Criteria Guide, Residential Application Checklist and Mandatory Documents Guide that reflect these updates. These will also be available to download from our website on Friday 1st April.