WEBINARS ON DEMAND:

ROYAL LONDON

Business Health Check

LEEDS BUILDING SOCIETY

Shared Ownership

ROYAL LONDON

Business Protection

LATEST PARTNER BLOGS:

L&G PRO

Meeting Consumer Duty Obligations

FLUENT MONEY

Consumer Duty: Principle 12

FLEET MORTGAGES

Looking Ahead At The BTL Market In 2023

Legal & General

Commission on Policy Authorisation

From 30th May 2023, Legal & General will revert back to paying on policy authorisation. You do not need to take any action and the new commission structure will apply automatically to all standard indemnity commission policies put on risk from this date. You will also receive a separate email communication from L&G on 19th May 2023 outlining the change.

18 months ago, Legal & General had really good intentions to lead the market in the change to their commission payment terms but since then the landscape has changed significantly. Legal & General hadn’t anticipated this at the time of implementation and have since received overwhelming feedback from key partners, firms and advisers that this is a blocker to business and the impact it is having during a cost of living crisis. As such, Legal & General has made the decision to revert back to paying on policy authorisation.

Impact Specialist Finance

Residential Portfolio & MUFB exclusive via Impact Packaging

This exclusive 5 Year Buy to Let product is now available to Multi-Unit Freehold Block and Standard Residential Portfolio clients. With a loan size between £1-5 million with a maximum LTV of 77% over a 10-year term, speak to Impact to learn more about this exclusive product.

Highlights:

- Available on Residential Portfolios and MUFBs

- Loan size between £1m and £5m

- Max LTV of 77% gross (inc. Arrangement fee)

- Lend on aggregate value of MUFB’s up to 20 units

- Term Length: 10 Years

- ERC: 5% in fixed period

- Exit Fee: 1%

- Arrangement Fee: 4%

- Impact pays a 0.50% procuration fee on mortgage completion

Have a case you’d like to discuss? Get in touch with the team now on 01403 272625

Accord Mortgages

Affordability Improvements

We’ve reduced the minimum household income threshold for lending above 4.49x LTI to £60,000 (from £70,000), for LTVs up to 90% (85% for new build) including the Boost LTI range – which offers increased LTI options of up to 5.5x income.

This can help you help even more of your clients find a place to call home by providing more flexibility to achieve their borrowing goals – whether they’re first-time buyers, those looking to move up the property ladder or remortgaging.

| Transaction Type | Income below £60,000 (joint or sole basis) | Income above £60,000 (joint or sole basis) |

| Standard Purchase and Remortgage up to 90% LTV | 4.49x | 5.0x (5.5x with Boost LTI) |

| Standard Purchase and Remortgage up to 95% LTV | 4.49x | 4.49x |

| New Build Purchase up to 85% | 4.49x | 5.0x (5.5x with Boost LTI) |

| New Build Purchase above 85% | 4.49x | 4.49x |

Newcastle Intermediaries

Doubles offer period to six months

Newcastle Intermediaries has doubled the validity period of its borrower loans to six months.

The broker-only arm of Newcastle Building Society says the move will help buyers in “property chains where the process can take longer, or customers looking to re-mortgage well ahead of their current deal expiring”.

The changes to its offer period affects purchase and remortgage customers, while the offer period for new build applications remains at nine months.

Newcastle Building Society head of intermediary mortgages Franco Di Pietro says: “Borrowers looking to buy a home or remortgage can experience uncertainty during the process, particularly those who find themselves in a chain.

“We want to ensure we’re able to support a broad range of borrowers as effectively as possible and, after listening to broker feedback, we’ve taken the decision to increase our offer validity period to help ease some of the pressure facing borrowers, providing greater peace of mind at a time that we know can be stressful.”

Mansfield Building Society

Flexible lenders left to fill the HTB hole

Lender flexibility is crucial for borrowers looking to purchase a new-build home.

That’s true irrespective of whether they are utilising a Government support scheme or a type of mortgage that makes the most of family help, such as a guarantor, gifted deposit or our Family Assist product.

We know that there is no shortage of would-be homebuyers who are keen to get onto the ladder, but are held back because of the way some lenders look at affordability. It may be that the lender will not consider additional income sources, or because there is some other level of apparent complication in their circumstances.

This supposed complexity is only added to by the fact that the property is a new build, since we know that some lenders approach this form of property with a heightened sense of cynicism.

If lenders persist with overly stringent affordability assessments, and a particularly cautious eye when new build is involved, then borrowers of all kinds may struggle to access the funding needed for these purchases.

However, there remains a subset of lenders, like Mansfield Building Society, who put the focus on manual underwriting and understanding the intricacies of an individual case. By being more flexible and more versatile in the way we assess cases, we are better placed to support borrowers purchasing a new-build property, no matter how they plan to finance that purchase.

There may be no direct replacement for Help to Buy, but lender flexibility can play a significant role in aiding borrowers in achieving their new-build dreams.

A common sense approach

If you’ve got a case on your desk that requires a common sense approach to lending then please pick up the phone to our Broker Support team on 01623 676360 or visit https://www.mansfieldbs.co.uk/intermediaries/.

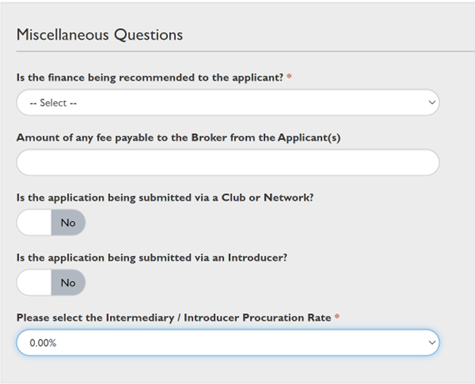

Gatehouse Bank

Advance Notice of changes to Procuration Fee information

We are writing to give you advance notice that we are introducing changes when completing a DIP for your clients so that all procuration fee information is captured within the KFI that you present to your customer.

Until now, the procuration fee had been formulated in the background. With the changes we are implementing you will now be required to select the appropriate procuration fee information at DIP stage for both the route you are submitting business and the product being recommended. The changes are as follows:

- To provide more clarity, the existing question ‘Enter broker fee’ has been changed to: ‘Amount of any fee payable to the Broker from the Applicant(s)’. In this box you will need to enter the amount of any fee you are taking from the customer for providing your services.

There are three new questions which will now also appear:

- Is the application being submitted via a Club or Network? if answered yes, a dropdown list of Clubs and Networks will appear to be selected. This question will automatically default to no unless you click ‘yes’.

- Is the application being submitted via an Introducer? this question will automatically default to no and as a broker, there is no need to change this option.

- Please select the Intermediary / Introducer Procuration Rate: this is a mandatory question and will ask you to select from a dropdown list of different rates with an explanation of what they relate to.

If you have any queries or require further information our team remains available via phone and email, details of which can be found here.

Melton Building Society

NAVIGATING CHOPPY WATERS: How MBS Lending is Supporting Borrowers with Impaired Credit

There’s no denying that we’re navigating choppy waters through unprecedented times and mortgage borrowers are feeling stretched. What with the Covid pandemic, the war in Ukraine, Liz Truss’s car crash of a budget, plus the rising cost of living and inflation, it’s not surprising that more and more people are facing financial difficulties.

As a result, missed payments, defaults and CCJ’s are becoming increasingly common amongst borrowers. In 2023, the year of the re-mortgage, many customers will be coming to the end of their existing deals in a completely different situation to when they first took out their mortgage. As lenders, it is our responsibility to serve these customers and provide them with the best possible solutions.

Fortunately, there are now many lenders that consider impaired credit and other such scenarios that require a common-sense lending approach. The majority of these lenders are smaller building societies that offer specialist lending solutions.

MBS Lending, a subsidiary of Melton Building Society, is a specialist lender focusing solely on residential mortgages for customers up to 70% LTV with impaired credit.

We can consider cases such as existing IVA & DMP, up to 3 missed mortgage payments in the last 12 months, and even day 1 discharged bankruptcy. What’s more, MBS Lending offers a manual underwriting approach, a variety of niche criteria elements, and a seamless application origination portal powered by fintech Mast. This allows brokers access to a state-of-the-art platform where they can submit, track, and manage applications.

MBS Lending re-launched the full product range on February 17th and has since seen a demand in enquiries for adverse cases. Our statistics show that 20% of all enquiries to the Sales Desk since the launch have been related to impaired credit.

As we enter the year of the re-mortgage, it is vital that we consider the changing financial landscape and provide our clients with tailored solutions that meet their specific needs. With MBS Lending, you can rest assured that you have a reliable partner who understands the complexities of impaired credit cases.

To find out more, visit www.mbslending.co.uk or contact the dedicated sales team on 01664 414144 (option 1 for new sales enquiries) or email sales@mmbs.co.uk

Key Partnerships

Working with a trusted specialist referral partner

By now, you’ve likely heard of the Financial Conduct Authority’s (FCA) new Consumer Duty principle being introduced on 31 July 2023. This new principle requires firms to act to deliver good outcomes for their customers. Therefore, if you’re proposition is tailored towards an individual or small number of solutions, you still require a wider field of vison to understand whether your client may benefit more from products, propositions, or services that you don’t provide.

Therefore, if you work with customers over 55 but don’t have equity release permissions, you should consider finding a trusted specialist referral partner, like Key Partnerships.

By working alongside Key Partnerships as your equity release referral specialist, you gain a complementary solution to your existing capabilities, with no need to give any equity release advice yourself.

Want to find out more about working with Key Partnerships? Read this blog here.

Pure Retirement

Consumer Duty and Vulnerable Customers: Are You Prepared?

Pure Retirement have added to their blog series explaining the purpose and impact of the upcoming Financial Conduct Authority (FCA) regulations on Consumer Duty.

In this blog, they explain the second of the three cross-cutting rules: “A firm must avoid causing foreseeable harm to retail customers.”

The latest piece of content contains examples of firms causing foreseeable harm, gives context around how firms can avoid foreseeable harm and what this rule does NOT expect of a firm.

They will also be holding the third webinar in their Consumer Duty series, “Consumer Duty and Vulnerable Customers: Are You Prepared?”, 7th June at 10am.

Join Managing Director of Later Life Living, Simon Chalk, as he discusses the characteristics of vulnerability, and what you need to do to accommodate your customers’ vulnerability, to ensure that they experience the best outcomes.

Precise Mortgages

How Precise Mortgages’ are meeting Consumer Duty

On Monday 31 July, the Financial Conduct Authority (FCA) is introducing Consumer Duty which sets higher and clearer standards of customer protection across the financial services industry.

The Duty requires all of us to consider the needs, characteristics and objectives of our customers – including those with vulnerabilities – and how we behave, at every stage of the customer journey.

Precise Mortgages’ have created a Consumer Duty Hub which outlines the roles and responsibilities expected of us. You’ll also find details about what we’re doing as a business to meet them and provide good outcomes for your customers, as well as copies of our fair value assessments.

Halifax Intermediaries

affordability changes

Halifax have increased the qualifying loan to value (LTV) from 75% to 90% for an enhanced maximum loan amount when selecting a 5 year+ fixed rate mortgage product, this will expand the number of purchase or remortgage customers who can benefit.

We are also further improving some of the loan to income (LTI) caps applied as part of our affordability calculation:

- For like for like remortgage customers with no additional borrowing, who receive employed income only, up to 75% LTV and subject to credit score a 5.50x LTI will apply where the standard LTI would normally be below this level

- For employed incomes only of £50,000-£75,000 and LTV 75.01-85% the standard LTI is being increased from 4.75x to 5.00x

Following the affordability changes made this year these changes will help us support even more financially resilient customers with improved affordability outcomes.

For the 5 year+ fixed rate enhancement to apply the whole loan amount must be on a 5 year+ fixed rate, and if porting a product from an existing Halifax mortgage the remaining term on the ported fixed rate product would also have to be 5 years+.

The increased LTI for like for like remortgages would not apply for remortgages on an Affordable Housing scheme (shared equity or shared ownership) where a 4.49x LTI will still apply.

Please see our website Criteria section ‘Affordability, LTI and Income Multiples’ for more information on our LTI limits. This section and our Mortgage affordability calculator will be updated.