AMI

PROTECTION VIEWPOINT 2022 – HAVE YOUR SAY

AMI Protection Viewpoint is back for a third year and we’re calling on all mortgage and protection advisers to complete our short survey.

Click here to complete.

Why should you get involved?

• It takes less than five minutes to complete.

• Your knowledge is essential to give us a deeper understanding of how protection is viewed and sold.

• It will help AMI shape our strategic plans on protection over the next 12 months.

We would be grateful if all mortgage and protection advisers working within mortgage advice firms, whether members or not, could complete the survey to give us the best possible set of representative results.

Thank you for your support in what we realise are busy times.

We plan to share our findings alongside sponsors L&G and Royal London in a launch event on 3 November. To find out more about Viewpoint, please click here.

Would you like your firm to feature in this year’s report?

We’re looking for firms to comment on this year’s market research findings. If you’d like to register your interest, please email info@a-m-i.org.uk.

Coventry For Intermediaries

Positive Changes to how we perform credit checks

From 18th August, Coventry for intermediaries will be making positive changes to how they perform credit checks on client’s mortgage applications. When brokers are obtaining an Agreement in Principle they’ll now record a soft footprint against a client’s credit record. It’s only once the full application is submitted that a hard footprint is left.

Jonathan Stinton, Head of Intermediary Relationships says “We understand that hard credit checks can cause a concern for anyone purchasing a home, and especially first time buyers. This is one of many exciting developments happening this year to really help brokers give their clients the best experience.

If you would like more information visit coventryforintermediaries.co.uk or call on 0800 121 7788.

ESBS

NEW MIXED-USE MORTGAGE

ESBS have recently launched a new mixed-use mortgage to assist people who wish to run or set up a business from their home.

Many people changed their working situation over the Coronavirus pandemic, with spaces for home offices becoming essential for many looking to move house. Working from home isn’t just reserved for office employees though. With a mixed-use mortgage, a room within an existing property can function as a business space giving certain professions the flexibility to set up their businesses at home including beauty therapists, dog groomers, and counsellors.

For more information on the ESBS mixed mortgages visit: https://www.esbs.co.uk/mixed-use-mortgages/

INTERBAY COMMERCIAL

TEMPORARY INCREASE OF MINIMUM LOAN SIZE

InterBay increase minimum loan temporarily to £1m loan amount (excluding Holiday lets & InterBay Bridging) from 5pm tonight.

FOUNDATION HOME LOANS

REMINDER OF 1 DAY SERVICE TIMINGS – WHY USE FOUNDATION FOR YOUR NEXT BTL CASE?

Foundation Home Loans currently have turnaround times of 1 day for DIP referral, application and underwriter review.

Why use them for your next BTL case?

Who for?

- Experts in individual or limited company applications

- Up to 4 directors & no personal guarantees needed for shareholders

- Limited companies/SPV with complex structures

- Shareholding can include other companies

- Newly formed SPV’s and flexible deposit sources including Intercompany loans

- No min income or employment/self-employment history

- First time landlords considered

- Ex-pats considered as individuals or limited companies

How much?

- Up to 85% LTV & Loans up to 2m (on core range)

- ICR of 125% for limited company borrowers and basic rate taxpayers

- No limit to portfolio size, subject to maximum borrowing of £5m with Foundation

- Portfolio in the background stress tested at 100%

What for?

- HMOs: standard to 6 bedrooms, large up to 8 bedrooms and MUBs: up to 10 units

- Short term lets in personal or SPV structures

- Day 1 remortgages

- Products without ERCs

- Range of Green mortgages for properties with EPC rating A-C

Why not try the loan calculator now?

PARAGON

INTERMEDIARY UPDATE

Welcome to the latest edition of Intermediary Update, where we provide you with a round-up of some of our latest news and blogs.

In this month’s edition, we take a look at the current trends in the market, including a breakdown of everything you need to know about the Government’s newly published Fairer Private Rented Sector (PRS) White Paper. We also introduce two brand new reports where we explore the rental sector energy challenge and examine the changing face of HMOs.

MARSDEN BUILDING SOCIETY

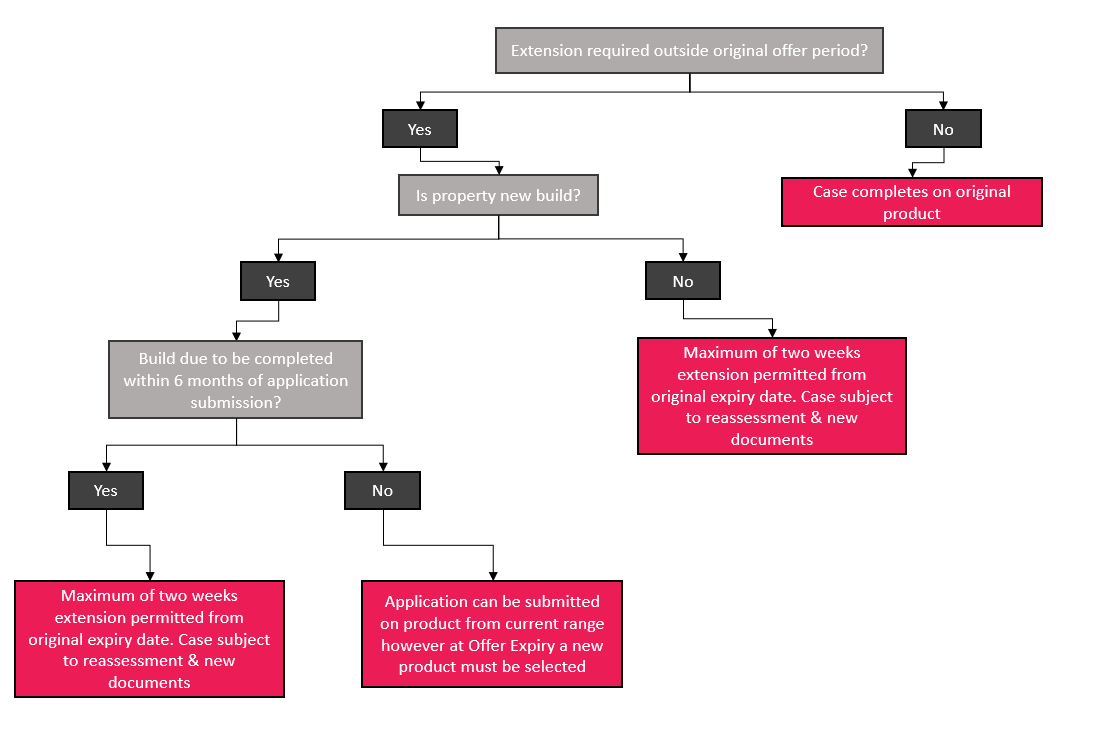

SHARED OWNERSHIP: CHANGES TO THEIR OFFER PROCESS

We’ve made some important changes to our offer process for Shared Ownership cases. Please find below an outline of the changes that come into effect immediately.

- New build applications accepted up to 95% LTV, even if the build isn’t due to complete within six months.

- Offers valid for 6 months and can be extended up to a further 6 months, subject to a new product being selected.

- Grace period of 2 weeks provided for offers due to expire which can complete on the original product selected.

- No re-offer fee applicable on Shared Ownership cases.

Got a case in mind?

We’re here to answer any questions you may have, so whether you have a case in mind or want to talk about our products and criteria, we’re happy to help – just get in touch.

GATEHOUSE BANK

TEMPORARY WITHDRAWAL OF BTL AND HOME PURCHASE PLAN PRODUCTS

Over the past few weeks, we have seen an unprecedented level of demand for our Home Finance products. In light of this, we have taken the decision to temporarily withdraw all Buy-to-Let and Home Purchase Plan finance products from sale at 5.00pm today (Tuesday, 16 August).

Whilst we understand that this will cause some inconvenience for you and your customers, we believe that these changes are the right thing to do, in order to manage the service levels we are able to provide.

Any valid DIPs that you wish to progress must proceed to a fully packaged application, including the customer’s signature, and be received via our online application system by 11.59pm on Thursday, 25 August. Cases received that are not fully packaged or remain unsigned after this date, will not be progressed.

We will continue to manage all existing cases as quickly as possible and your BDM remains available to assist you and discuss any queries regarding the changes outlined above.

We apologise for any inconvenience caused and thank for your continued support.

PAYMENTSHIELD

LAUNCH OF NEW CUSTOMER PLATFORM

On Monday 15 August, Paymentshield launched a new online platform for policyholders, replacing their existing customer portal, which will enable customers to have more control over their Paymentshield policies.

The new platform will enable Paymentshield customers to view all their policies in one place and allow them to make changes to personal details such as their name and email. In addition, policyholders will be able to amend their payment details and payment date as well as being able to renew their insurance online all without needing to pick up the phone to speak to us.

A key focus when developing the new platform has been improving user experience, which is why Paymentshield took a mobile first approach to ensure the site can be easily accessed from any mobile device, offering policy holders more freedom to access their insurance whenever and wherever they need to. Customers will also have easy access to the dedicated webchat from within the platform should they need any assistance.

This platform has been designed to make customers, and advisers’, lives easier and is just the latest in a string of planned innovations this year. Just last month Paymentshield added new features to Adviser Hub and increased Home Insurance quote validity to 180-days.

Jon Bowen, Customer Director at Paymentshield, says:

“By giving customers more flexibility and anytime/anywhere access, they can make changes to their policy in a way that suits them. For example, they can make card payments within our secure online platform without having to speak to anyone – offering greater convenience, and for some, making them feel more comfortable in the process.

“We also hope that in launching this new platform, it provides a strong selling point for advisers when they’re having GI conversations with their clients. And for existing Paymentshield policyholders, we’d urge advisers to encourage them to sign up in order to receive the benefits the platform provides.

“This launch is a significant step in helping customers actively manage their insurance and us supporting advisers and partners in enhancing the customer experience they provide but this isn’t the end of this development – we’ll be seeking to add more capabilities and will continue to evolve the platform over the coming months.”

Customers can sign up for the platform here – https://my.paymentshield.co.uk/

BM SOLUTIONS

CRITERIA CHANGES

From Monday 15 August we will be making changes to our criteria to further support landlords:

• The minimum age at application is changing from 25 to 21 years old.

• First time buyers (FTB) can apply for a Buy to Let (BTL) mortgage if at least one other applicant on the same application is a current UK property owner – evidence of current property ownership maybe requested. FTB cannot make a sole BTL applications.

If you have any queries, please contact your Business Development Manager.

KENSINGTON

THE WITHDRAWAL OF HELP TO BUY: A CATALYST FOR CHANGE AND INNOVATION IN THE NEW BUILD MARKET

Eloise Hall, Interim Head of National Accounts at Kensington shares her thoughts on the withdrawal of Help to Buy.

CHL MORTGAGES

CASE STUDY – LIGHT REFURBISHMENT

The Client

A limited company with two directors recently purchased a three-bedroom freehold house worth £300,000 at auction.

The directors wish to refurbish the house and then rent it.

The Issues

The property requires modernisation, to include installation of a replacement roof covering, replacement kitchen and bathroom, together with general redecoration and improvement throughout.

They expect the property value after the works have been completed to be around £375,000.

The Soluton

Here at CHL Mortgages, we fully accept limited company structures.

Our new refurbishment product range is available to individuals and limited companies and is applicable on standard buy-to-let properties, small houses in multiple occupation (HMO) and small multi-unit freehold blocks (MUFBs). The range consists of three products: Light Refurbishment, Cosmetic Improvement and EPC Improvement.

The Light Refurbishment is ideal in this case. It has been designed for works not requiring building regulation sign off and includes works that can be signed off under the Competent Person Scheme.

So, if you have a limited company buy-to-let case where light refurbishment is required, then why not speak to us on 01252 365 888, contact your BDM or visit www.chlmortgages.co.uk/intermediaries