WEBINARS ON DEMAND

BLOGS

UPCOMING EVENTS

ROYAL LONDON

What’s on the menu?

FLEET MORTGAGES

Who are Fleet Mortgages? BTL case studies

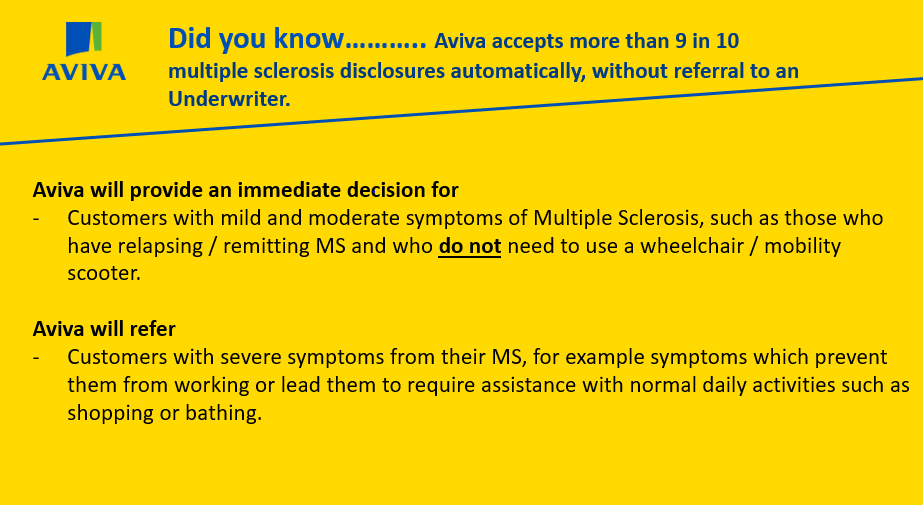

JUST

Making it personal

CLYDESDALE BANK

In the spotlight

ROYAL LONDON

Prioritising the protection conversation

HODGE

It’s time we stopped calling it Later Life

TMA Club

The age-old question for brokers

AMI

Looking head in 2022

Face to Face Workshops

Join us for our first series of Face to Face Workshops for 2022! There will be complimentary breakfast rolls upon arrival at 9:30am and plenty of opportunities to network throughout the day.

5th April – The Village Hotel Watford

6th April – The Village Hotel Edinburgh

7th April – The Village Hotel Solihull

Halifax

Work with us to get better service standards

I hope to appeal to you to seriously consider whether you need to call us for case updates and chasing for actions. Please trust that we are working hard to maintain our usual service standards during this extremely busy time.

The more you call, the more this is put in jeopardy – so please check your case tracking/broker dashboard and emails and limit your calls to those cases where exchange or completion are imminent and you need our assistance.

If you have any additional or new information relating to a specific case, please use the Contact Form which is available on our website.

The uploading of all supporting documents on submission of applications helps us to progress them swiftly so please ensure you review any emails and next steps messages to ensure we receive the information we need.

Thank you for taking the time to read this message. It really is vital that we work together without the need for update or chase calls to our processing teams in order that we can continue to provide the service you expect.

Vida Homeloans

Opportunity knocks for BTL landlords

When it comes to buy to let, it could be argued that we have seen more changes in the last five years than the previous 20. But as the adage goes, change brings opportunity.

Most recently it was announced that all newly rented properties in England & Wales will be required to have an EPC rating of band C or above by 2025*. Some claim this change presents more challenges and cost burdens leading to landlords selling up – and a detrimental effect on the private rental sector.

At Vida, as a lending specialist who really understands the market, we see things differently. Our view is that this is good news as it gives real opportunities for brokers and landlords. Besides, people also said there would be a landlord exodus with the tax changes several years back; landlords are resilient and adaptable.

SANTANDER

Working with you… Check before you submit

Detecting and preventing mortgage fraud starts at the application stage.

It’s important to verify your client’s identity, documentation and employment details.

Please check all details in the application before submitting on Introducer Internet.

Any inaccurate information could lead to a decline decision and may have potential fraud impacts which can affect your client’s credit file.

Our dedicated webpage has information on the latest types of financial fraud and scams being reported across the UK. From tips on how to spot mortgage fraud, to helping your clients recognise redirection scams when buying a home.

Barclays

Enhancement to Part and Part lending policy

Barclays are pleased to confirm an enhancement to our Part and Part lending policy, which will enable a wider group of your clients to benefit from one of our competitive deals.

Positive change to Part & Part Policy:

• We have increased the maximum LTV from 80% to 85% for all clients

This change will apply from today, Friday 18th March. Any cases started but not submitted before this date can also benefit from the enhanced policy.

Please note: the existing maximum LTV limits and criteria for the Interest Only portion of the loan remain unchanged (50% max LTV and £300k minimum equity requirement for sale of property repayment strategy, and 75% max LTV for other repayment strategies, such as sale of an existing stocks and shares ISA).

Here is a worked example of how the new LTV could apply

• In Example A, at the end of term the capital & interest repayment part of the loan is repaid, so there would be £300,000 equity left; this example would meet the minimum £300,000 equity requirement using the sale of the mortgaged property as the repayment strategy.

• For Example B, the minimum equity requirement wouldn’t apply as the repayment strategy is not the sale of the mortgaged property.

All other lending policy applies and remains unchanged.

The Mortgage Lender

More flex for incomes that are complex

With our new streamlined residential range, it’s now easier than ever to secure a mortgage for customers with unique income streams.

So, people who won’t be boxed in are now easier to place, and you can match them with the right product at competitive rates.

Take a look at how our new 4 tier range cuts the clutter:

- We consider multiple incomes, including second jobs

- We consider overtime, employment bonus, car allowance and commission for affordability

- Aside from our RL0 product range, we will not use credit scores to determine the product rate

- 50% of rental income is considered

Power of 8

Your invitation to the ‘Power of 8’ event March 2022

Working together to share industry knowledge and expertise

We’re back with a bang with our first live event of 2022!

‘Tackling Complex Cases with Confidence’

Wednesday 30th March 8:45am – 12:30pm

(Registration & breakfast buffet 8:45am – 9:30am, event start 9:30am)

Vermilion, Hulme Hall Lane, Lord North Street, Sport City, Manchester, M40 8AD – Register Here

In addition to the lender sessions on common sense underwriting and tackling complex cases, the event will also feature guest speakers:

Nicola Firth, a mortgage broker for 13 years with her own brokerage for seven, founded Knowledge Bank in 2016, the UK’s first criteria search system.

Nicola will talk about “Turning Complex into Completed” – You know the scenario; they’re good clients, the case stacks up really well….you’d lend your own money on it if you could….but it just falls outside on a technicality. Find out how Knowledge Bank is helping brokers across the country turn complex cases into completed cases….and saving them hours at the same time!

Simon Lovell, Filed Compliance Manager of TMA Club & Vicki Brady, Customer Account Manager at PRIMIS Mortgage Network.

They will be discussing the good and bad practices they see through file reviews. As well as covering vulnerable customers and the recent FCA Duty of Care paper and what that means for advisers.

TMA is a mortgage club made up of people that are dedicated & passionate about supporting Directly Authorised businesses. PRIMIS provide mortgage and protection advisers with world class support. From training, events and business development to regulatory guidance, technology and a broad product panel.

We look forward to welcoming you to this CPD accredited event!

Precise Mortgages

On the case for new build and Help to Buy

With the Help to Buy scheme due to finish in March 2023, time is running out for first-time buyers with low deposits to buy their dream new build home.

Fortunately, our extensive array of products could support your customers, even those declined by a high street lender. We’ll accept:

- Those with an adverse history

- Non-repayable family gifted deposits

- Self-employed with only 1 year’s tax calculation and HMRC Tax Year Overview or accounts.

- Applications on Help to Buy England, Help to Buy Wales and Help to Buy Scotland equity loan schemes.

Foundation Home Loans

Limited company lending: The only way is up

Just over half of landlords are now looking to purchase their next BTL property within a limited company structure, up 9% from Q3 2021. The latest iteration of the BVA BDRC Landlord Panel research for Q4 2021 highlighted that a growing number (52%) of landlords are now utilising the benefits of a limited company vehicle when adding to their portfolios. Those with smaller portfolios continue to be more likely to purchase as an individual, with this being the case for 52% of landlords with 1 – 10 properties vs. 11% of those with 11+ properties.

Legal & General

NEW electronic Declaration of Health for Intermediaries – A new online digital journey for new business

We’re pleased to announce that from 14th March 2022 we’ll be launching a new Digital process, giving you the option to complete a new business, Declaration of Health on behalf of your customer.

Our online journey in Agent Hub (OLPC) gives you the control to complete the Declaration of Health quickly and easily, helping you get your customer on risk sooner.

Watch our short video to see how it works here.

More benefits:

- We’ll let you know 7 days before a declaration of health becomes due to save you time in unnecessary delays when it’s time to put your customers policy live.

- Our pro-active approach saves you time and helps with your pipeline management and getting your business on the books without delays

- We’ll let your customer know that you’ve completed the Declaration on their behalf allowing them to check their details are correct.

- We’ve removed unnecessary paper documents and processes so no more delays with paper and postage adding delays to your customer being protected.

Skipton Building Society

How great client services create lasting client relationships

Derek Adams is joined by The Mortgage Mum’s Shelley Walker to discuss how brokers and lenders can benefit from offering great customer service.

They explore what customers can and should expect, how The Mortgage Mum creates lifetime clients and how they use social media and word of mouth to build key relationships.

About Shelley Walker

Shelley is a Senior Mortgage Broker at The Mortgage Mum, an all-female Mortgage and Protection Advice firm, who pride themselves on delivering excellent service, tailored to their clients. With over 20 years’ experience helping others and with a 5 star client rating, Shelley truly reflects The Mortgage Mum’s ethos and reputation.

Still to come on Skipton Talks:

22 March – The New Build market: how we got here and what comes next

Rachael Hunnisett chats all things New Build with Craig Hall from LSL Property Services. They talk about pivotal moments in the history of the New Build market and we get Craig’s expert take on what we can expect next in the industry.

29 March – A focus on Joint Borrower, Sole Proprietor

Learn about our Joint Borrower, Sole Proprietor (JBSP) Scheme, as Derek speaks to BDM Tracey Nash and Underwriting Lead, Charlotte Raw about our JBSP proposition. Find out how it could help your clients in different scenarios, including divorce and friends helping friends.

Subscribe today

It’s never been easier to keep up to date with our latest news and views on the intermediary mortgage market. Listen at home or on the go, and don’t miss an episode when you subscribe to Skipton Talks on your favourite streaming service.

Lendinvest

The technology making LTD Company Buy-to-Lets simpler

As part of an in-depth look into the LTD Company Buy-to-Let market, our Sales Director looks at the technology making the incorporation process and growing portfolios simpler.

Mansfield Building Society

High LTV deals and versatile criteria needed to support FTBs

Tom Molloy, Intermediary Sales Manager, Mansfield Building Society discuses the Mansfield high LTV deals and more.

We have heard from plenty of brokers and networks about seeing a swell of interest from first-time buyers of late.

The reasoning is pretty understandable – we have seen two base rate rises in three months, with more potentially on the way, and first-time buyers will be carefully considering their options.

As a result, moving now and securing a deal at a lower rate makes a lot of sense. But are lenders really doing enough to provide the funding these borrowers require?

Newbury Building Society

We hold all the cards you need

From complex incomes to ex-pats and unusual properties, we’re holding a whole deck of flexible lending cards. Take a peek at what we have in our hand, we’re not bluffing…

- Simple, rapid remortgaging and additional lending for home improvements inside and out

- Later Life Lending to borrowers aged up to 90 years and RIO mortgages

- Ex-Pat and foreign currency loans

- Bank of Mum and Dad and Joint Borrower-Sole Proprietor

- Shared Ownership with a maximum term increase from 35 to 40 years, and mortgages to 95% (new builds and flats)

- Self-employed and contractors – CIS workers are now accepted based on income shown on CIS vouchers. We can help with newly qualified professionals, or a mix employed and self-employed incomes

- BTL throughout England and Wales (subject to London restrictions), including consumer, regulated, ex-pat, holiday let and Ltd Company

- Green mortgages including additional lending for existing borrowers, and our self-build green reward

- Unusual properties, including lending on annexes

- Made to measure – even with everything mentioned above, we have a tailor made product for clients who need an individual approach to their mortgage application.

PLUS! A new secure and swift document submission service

Did you know you can now use our open banking service to send mortgage documents to us? This offers a more secure service, which will also save you and your clients time. When you place a case with us our team will send you a link.

Our helpdesk is open Monday to Friday 9am-5pm – instant chat, email, or phone on 01635 918000.

Suffolk Building Society

Spotlight on: Make older borrower cases simple with the Suffolk.

Few lending areas have seen such development as those for applicants over 55. When it comes to later life borrowers it’s not just about swapping an existing mortgage deal – we’re seeing an increasing amount of previously mortgage-free clients choosing a mortgage to fund later lifestyle choices.

And, for your clients taking a mortgage in or into retirement, this is where expert, manual underwriting can really help, as we’ll take a close look at your case rather than relying on a computer to make decisions for us.

Joan & Jim: case study.

Silver 60’s remortgaging to clear existing mortgage + gift funds to family.

- Current mortgage £150k

- Additional gift to children £100k

- £250k new mortgage on property value of £750k

- Both applicants are enjoying retirement but want to keep costs to a minimum – interest only is the preferred option.

- They have SIPPs and a private pension currently (and state pension due to kick in within the next couple of years).

- Drawdowns from the SIPP are sporadic – they only take income as needed and are using their savings for day-to-day living.

Affordability:

- Based on the private pension and what can be evidenced in the SIPP we can look to use both for affordability.

- Private pension – £30,000 p/a & SIPP value – £600,000 (x 80% of fund [buffer for fund fluctuations] = £480,000, / 15 year term = £32,000 p/a for the term of the mortgage)

- Total usable income of £62,000 per annum.

- Using the SIPP in the background made all the difference – we were able to lend £250,000 on an interest only basis over a 15 year term

Cheers to that!

The mortgage will take the applicants into their mid 70’s, on an interest only basis, with additional borrowing to support family, with downsizing as the repayment vehicle

Get in touch.

Whilst we can’t list everything we accept, or the conditions which apply, we’re on hand to help! If you want to find out more, or have a case in mind, give us a call on 0330 123 1073 (option 1).

LV= Equity Release

Meaningful Later-life Benefits

At LV=, we understand that your support for clients extends beyond their financial needs. How you demonstrate your support to clients from the early stage is crucial in the process of building a long-lasting relationship. That’s why we include two non-contractual services to our equity release customers at no extra charge – LV= Doctor Services and Care Navigator.

We are fortunate to have representatives from both of these services joining us on the day. We’ll take a more detailed look at the support available through the lens of both equity release customers and you as their adviser.

This webinar is eligible for one hour unstructured CPD.

22nd March 10-11am