Changing Applicants on an Application

This is an important reminder on application amendments relating to customer names.

Once you’ve started keying an application and you wish to change the order of the applicants, or add / remove an applicant, it is extremely important that you do not amend one customer details to those of another customer. This applies to all changes on Decision In Principles or Full Applications whether fully submitted or not. Please follow the steps below to ensure the data is correctly allocated to the right customer:

- To change the applicant order:

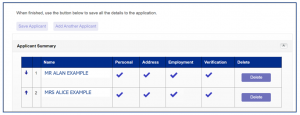

- In the ‘Applicant Summary’ table at the bottom of the ‘Personal Details’ screen use the ↓ and ↑ arrows on the left-hand side to amend the order

- Click ‘Submit’ button.

- To remove an applicant:

- If you have an application with more than one applicant and you want to delete the first named applicant, you must change the applicant order so applicant one becomes applicant two; then you will have the option to delete applicant two

- In the ‘Applicant Summary’ table at the bottom of the ‘Personal Details’ screen use the ‘Delete’ button on the right-hand side to remove an applicant

- Click ‘Submit’ button.

- To add an applicant:

- Click ‘Add Another Applicant’ button on ‘Personal Details’ screen

- Complete new applicant details

- Click ‘Save Applicant’

- Click ‘Submit’ button.

Under no circumstances should you change any information keyed in name, date of birth or other personal details fields from one individual to another. Please also see this information on our website.

Loughborough launch Holiday Let Mortgages

Earlier this week the Loughborough Building Society launched Holiday Let Mortgages:

Criteria

- Up to 75% LTV

- Up to 60 Days permitted for applicants own use

- Rental Coverage is set at 130% at 5.5% regardless of the applicant(s) tax position

- Holiday Let rental assessment is required from a local agent confirming the number of lettable weeks and the total expected annual rental income.

- It will be a condition of the mortgage that a holiday lettings management company be in place for the duration of the let, Arbnb acceptable provided this is in addition to the lettings management company. (Can not be solely let via Arbnb)

- Must be a homeowner or have previous experience of home ownership

- Minimum income of £25,000.00 single or joint (combined)

- Minimum Loan £25,000.00

- Minimum Property Value £90,000.00

- Minimum Age 25

- Properties in England & Wales – (Flats by referral)

Don’t forget, you can currently only access the Loughborough Building Society via TMA!

Packaging 95% LTV applications

95% LTV mortgages are available through the government mortgage guarantee scheme.

Evidence required for employed applicants:

- Three months’ personal bank statements.

- Latest monthly payslip or if paid more frequently than monthly, last four weeks’ payslips required.

- Completed mortgage guarantee declaration.

Please note where any applicant is self-employed these applications are not eligible for the mortgage guarantee scheme at this time.

A video Q&A with our underwriters

We want to help you submit business more easily. So, we asked our underwriting team to share some tips to do just that.

In this short video, Steve Bowers, Senior Underwriting Manager and the team, answer a series of underwriting questions and provide tips to save you and your clients valuable time.

Grow your business with Metro

Why brokers use Metro Bank?

- NEW – Self-employed – profit before taxation plus directors remuneration can now be used. An average is taken over the last 2 years if 100% of shareholders are on the mortgage and sustainability of the business can be confirmed.

- 95% LTV Residential mortgage 2, 3 & 5 year fixed – purchase and pound for pound re-mortgage, available on flats and houses, maximum loan size of £675,000

- Joint borrower, sole proprietor on both Residential and Buy to Let – only where the additional borrower(s) is a close family relative, up to 4 applicants with all 4 incomes considered

- Near Prime products for customers with a less than perfect credit profile and/or low credit score

- Up to 5.5 times income multiple for professionals and high earning customers through our Professional Range

- Enhanced contractor and fixed term contract worker policy, On-shore umbrella contractors are acceptable

- Second homes up to 85% LTV – Airbnb accepted up to 90 days per annum

- Buy to Let – 5 year fixed stress test is 4.0% at 140% of the mortgage interest amount calculated, maximum age is 85, top slicing from earned income accepted to support Buy to Let applications

- Furlough accepted up to 80% loan to value

- We use 50% Bonus/Commission/Overtime from the last years P60

A festival of lending criteria changes

Available now | You’re on the guest list

HEADLINERS

Later life: using pension asset as income

More flexibility when using SIPP and pension funds for affordability assessments and income multiples – for applicants over 55, we’ll divide 80% fund value of a SIPP/pension fund that isn’t being drawn by the mortgage term and use the resulting figure in our calculations. We’ll have to see a recent statement showing the value.

Self build: day one remortgage

We can now accept an application within 6 months, if your client shows as the land owner on the Land Registry prior to application

SUPPORTING ACTS

Self employed & contractor

- Accepted up to 90% LTV

- Gov support loan considered if no loans taken in 2021 & loan not spent (evidence required funds remained in account)

- For accounts covering 2020 (or April 2021 SA302s) we’ll use latest figure if no more than 20% increase (if >20% will use average). Note: average of last 2 years as standard.

- Self-employed grants up to 90% LTV, if no grants taken in 2021

- Day rate contractors up to 80% LTV, click here for more info & search contractor

Other

- Debt con accepted – max 75% LTV

- Consolidation of 2nd charges accepted (subject to origin not being for debt con)

- Payment holidays – none in last 3 months

- Applicants on furlough not accepted

- Bonus, commission and overtime – can take 100% if guaranteed & evidenced in contract (otherwise will take 50%)

CRITERIA CLINIC

First Time Buyers (Types of deposit)

Join us for our next LIVE Criteria Clinic at 10am on Monday 16th August where we will be answering your questions on criteria relating to First Time Buyers (Types of deposit) and helping you place those cases.

This Clinic will be hosted by our CEO and Founder, Nicola Firth and joining us to answer your questions and give you some valuable insight into this area of lending on Monday are:

Harpenden Building Society – Jacqui Turner, Business Development Manager

Reliance Bank – Gareth Byrne, Head of Mortgages

The Tipton – Richard Groom, Head of Mortgage Sales

Mansfield Building Society – Anna Deakin, Business Development Manager

Attendees who attend the full session will be sent learning certificates which can be used for CPD.

We encourage brokers to ask questions during the event, but if you would like to provide us with any questions you have in advance, please supply when registering below. We will do our best to get through as many as possible during the live session.

Aug 16, 2021

10:00

New Pepper Premier Packager Residential Exclusive range available from TFC

Exclusive products up to 85% LTV on Pepper 18 + 12 (only 80% available to wider distribution)

Exclusive product up to 80% LTV on Pepper 6 (only 75% available to wider distribution)

All products in the range feature £150 cashback

L&G Fracture Cover – Protecting against the cost of injury

Fracture Cover for an additional £5.90 per month when they take out personal protection. Providing peace of mind that should your client get injured, they’ll have some financial protection in the event of a valid claim. It can be added to life insurance, critical illness, income protection and rental protection policies.*

With Fracture cover, your clients get:

- Multiple claims per year with a maximum pay-out of £7,500

- Cover for specified injuries such as, 20 different fractures, 9 different joint dislocations, Achilles tendon ruptures and knee ligament tears

A chance to win £250 with a short survey

Your feedback is important to us, that’s why we’ve sent you a short survey to complete.

Those who complete the survey before 27 August will be entered into a free prize draw to win a £250 amazon voucher. Terms and conditions apply.

Watch whenever you want, from wherever you are

Our summer webinars are now available to watch on demand on our Skipton Talks hub and on our YouTube channel (subscribe to get easy access to the latest webinars).

We were delighted that so many of you registered for the live webinars and joined our discussions on topics including efficient mortgage advice, what valuers really think, and the role of technology in the future of the intermediary market. And now you can watch the webinars again.

Watch our webinars on the Skipton Talks hub now.

Not to be missed

Thanks for rating our summer series 4.69/5 stars* and for telling us what you think, too. We’re busy working on the next series of webinars and can’t wait to share them with you. Sign up for email alerts to get updates on when you’ll be able to book your space.

*based on 972 brokers who responded between 10 June – 22 July 2021.

In your words

Here are a few of our favourite comments from the summer series and a word from your Skipton Talks host.

‘Very impressed with the professional presenting skills from all in the webinars, by far the best I’ve seen.’

‘The webinar Series that Skipton run is amazing, I really look forward to Thursday mornings. It’s the highlight of my week.’

‘Great webinars- short, concise and relevant information.’

-Mortgage Broker feedback from 2021

“We had a fantastic time putting together the summer series, thank you to so many of you for joining us for the live webinars! It’s been a joy to read through all your feedback, rest assured, we read all of your suggestions and are putting many of them into action for our next instalment of webinars. Watch this space for more details.”

Rachael Hunnisett, Host & National Accounts Lead.

Residential clients that are self-employed directors with retained profits? Sorted.

Richard and Julie are 50 & 51 and married with three children living at home. They have fluctuating and multiple sources of income including retained profits from their established plumbing business. Unfortunately, a small issue with HMRC four years ago due to a rogue accountant means their credit rating has taken a hit.

They are wanting to raise an additional £50k on their existing £200k to improve their 4-bed house in Essex worth £650k.

BE GI: STRONGER TOGETHER VIRTUAL CONFERENCE

Paymentshield invite you to join them at their “Be GI: Stronger Together” virtual conference on Tuesday 14th September from 9:45am.

The conference will build on the theme of embracing general insurance (GI) and sharing ideas and best practice to really help advisers make the most out of the GI opportunity.

It also aims to help strengthen the adviser community, offering an opportunity to ask questions, share your views and find out how Paymentshield can help you to properly protect your customers and build a reliable income stream.

Paymentshield have introduced a new format to this event. The day will be starting with a keynote focussed on the opportunities in the market, especially around GI sales to remortgage clients. But for the rest of the day, there’ll be a choice of two sessions at any one time.

Attendees will be able to choose from either a panel discussion focussed on hot topics within the industry such as the FCAs new rules around fair pricing, or a GI specific session which will be led by one of Paymentshield’s regional sales managers. This means throughout the morning you can pick and choose which topic or style of session you prefer.

Guest speakers to be announced…

Paymentshield will also be recognising advisers and firms who’ve gone above and beyond over the past 12 months and celebrating their successes in their second annual awards ceremony.

Once registered, you’ll be able to request a branded conference notepad and pen to be sent straight to your door.

Register now to discover how we can all be Stronger Together

BTL UPDATES VIDEO

Effective today, we are implementing a range of changes which will simplify and enhance our Buy to Let proposition. These enhancements will help us support even more customers with their Buy to Let goals.

What’s Changing

- Two new simplified indication calculators: One for ‘Small Landlords and Like-for-like Remortgages’, the other for ‘Portfolio Landlords and First-Time Buyer Buy to Lets’.

- Lower Stress rate of 4.5% for 5 year products and Like-for-Like Remortgages – With two maximum lend options shown on calculators.

- For Small Landlords and Like-for-Like applications, Brokers select client’s tax band for assessment, no proof of income is required on submission and the application will proceed through a reduced underwriting process – This means a quicker journey for the broker and customer.

- Removal of Loan-to-Income (LTI) cap for Small Landlord and Like-for-Like applications, meaning the maximum lend will be based on the subject property’s rental and the clients tax band.

- Removal of top-slicing for Small Landlords and Like-for-Like remortgages. In order to help build a strong and simplistic foundation for our Buy to Let proposition, we have removed any top-slicing ability of these type of applications. Income will still be used towards Portfolio Landlord and First-Time Buyer applications.

For a high-level overview of the changes, please view our new animated Buy to Let video

To complement the above changes, we have created a new Buy to Let Hub, which can be accessed here. We have also updated the Buy to Let entry on our A-Z of Lending Criteria Page.

If you have any questions, please speak to your BDM.

Limited edition HMO

We’re pleased to announce that we’ve re-launched our two limited edition products for Houses in Multiple Occupation (HMOs) and multi-unit blocks.

And for a limited time only, for multiple property applications we are only charging one application fee! Ring the TMA helpdesk on 0330 303 0236 or Speak to your Paragon Regional Manager to take advantage of this offer.

Top 5 Residential Criteria

We’ve got Olympic fever at the Melton, so we thought we would bring you our top 5 residential criteria to represent the Olympic rings. The below criteria can be used alongside our standard residential products and also our Shared Ownership, Help to Buy, Right to Buy and Retirement Interest Only products.

1.) No credit scoring in Society – We don’t credit score in Society, this is great news for younger borrowers, first time buyers or those that have perhaps had historic impaired credit. We don’t have a debt to income ratio either. We do credit search and we use Experian.

2.) Manual underwriting – We manually underwrite each case individually. This means we can apply a common sense approach and a degree of flexibility, instead of a computer says NO approach.

3.) Gifted deposits – We can consider family gifted deposits up to 50% of the purchase price. This isn’t restricted to immediate family members either. We can also consider gifted equity and small deposit contributions from vendors and employers by referral.

4.) Max 4 applicants – We can consider up to 4 applicants on an application. Where they are immediate family members we can use 100% of all incomes for affordability purposes. Having parents on the mortgage will also mean they are named on the deeds.

5.) Max age 80 – We can consider using earned income up to age 80, subject to feasibility of their job role. This means if your customer is a back seat company director or in an admin based role, we can consider using their income to age 80. If the applicants are already retired and we are using pension income, we don’t have a maximum age.

Please visit our website www.themeltonbrokers.co.uk. If you have any queries please call our Broker Support Team on 01664 414144

Take ad-Vantage of Bridging

With annual house prices at a 17 year high in June 2021 and house prices up 10.5% YoY, there has never been a better time to consider bridging finance to renovate, not relocate.

These short-term, interest-only loans are ideal for auction purchases, home improvements and renovations, fixing broken property chains, raising money for business purposes or just cash flow.

This summer, take advantage of bridging, coupled with super-fast completion times and loans up to 85% LTV.

If you would like more information on the above or if you have any questions or cases we can assist you with, drop us a line or give us a call today on 01753 883195

Don’t forget to enter our summer prize draw for your chance to win a luxury summer hamper!

Click here to enter: https://www.vantagefinance.co.uk/take-ad-vantage-this-summer

Another reason to consider lifetime mortgages?

Post lockdown, more city-dwellers are seeking homes with more space, boosting some regional property markets and values.

This could be another reason to consider a lifetime mortgage for your later-life clients.

Use our updated client profile map to see what lifetime mortgage clients look like around the UK.

HELPING YOU GROW YOUR BUSINESS

Introducing capital repayment

If the past 18 months have taught us anything, it’s that having options is essential for brokers and customers alike.

Hodge is a name synonymous with interest only lending but, after speaking to you, we know your customers are looking for more choice when it comes to their financial planning. So, we’re delighted to introduce capital repayment across all of our 50+ and Holiday Let fixed-rate products.

From August 10th we’ll be able to accept repayment mortgages for customers looking for the security of a repayment loan.

If you have clients reaching the end of an interest only term, wondering what to do next, they now have more choice with Hodge. Whether they’re remortgaging to improve their home, or hoping to gift to family, Hodge can help with the moments that matter.

For holiday let clients wishing to repay the mortgage and own an unencumbered property to retire to, or even to pass on to future generations, this could be the solution they’ve been looking for.

With maximum LTV’s of 75% and no minimum equity requirement, we can help you provide your customers with a repayment mortgage offering the added benefit of our specialist service and flexible expertise.

What makes us different?

For 50+ Mortgages, at Hodge we…

- Consider earned income, both employed and self-employed, up to a maximum age of 80

- Look at both pre and post retirement income, there’s no upper age limit if the mortgage is affordable on pension income

- Can lend up to six times income on a like-for-like remortgage

- Lend from age 50 with a maximum term of 41 years.

For Holiday Let Mortgages, at Hodge we…

- Don’t require a minimum income

- Allow 90 days personal occupancy

- Accept first time landlords and Air B&B with up to 3 properties considered

- Lend from aged 21 to age 95.

Don’t forget, your customers still have the option of an annual 10% overpayment facility across our entire range as well as the flexibility of our Early Repayment Promise, where they can sell-up and repay in full without early repayment charges, for added peace of mind.

Capital repayment will be available to new Hodge customers from August 10th.

We’re working on a repayment calculator, but as we want to ensure we take into account all of your customers’ circumstances and income streams, for now if you have a case, we’d like to provide you with one-to-one support, talk to us to find out more.

Use the button below to get in touch with your dedicated Hodge expert. Or visit our Intermediary website to read more about or repayment mortgage here.

TMA UPCOMING EVENTS

Protection HiiT Series

Tuesday 21st September, 10:00am – 11:00am

TMA Virtual Elevate Conference

Thursday 14th October, 10:00am – 02.30pm

CLICK HERE

QUERY OF THE WEEK

Q – Which lenders are ok with a public footpath running through the client’s land on a residential self-build application?

Please give our broker support desk a call on 0330 303 0236 for more information.

LATEST BLOGS AVAILABLE

NatWest

A welcome Home for Remortgages

Hodge

Did you know, Hodge can help your clients make the next years, the best years.

New Build Bulletin Launch

Welcome to the first issue of our New Build Bulletin!

Precise Mortgages

Helping broker’s take on adverse credit during adverse times

CLICK HERE