WEBINARS ON DEMAND:

ROYAL LONDON

Business Health Check

LEEDS BUILDING SOCIETY

Shared Ownership

ROYAL LONDON

Business Protection

LATEST PARTNER BLOGS:

FLEET

Looking Ahead At The BTL Market In 2023

KEYSTONE

Multi-Title Split For Portfolio Landlord

GUARDIAN

It’s Time To Get On The Front Foot

Mansfield Building Society

Right to Buy with multiple income sources and background adverse credit

Here at The Mansfield, we take a personal and common sense approach to borrowers’ circumstances to offer a little Versatility for complex cases. In this case study, we helped a family with a Right to Buy purchase when there were multiple income sources and historic adverse credit.

The property itself was a mid-terraced house in London. The open-market property value was £440k, however the Right to Buy purchase price was actually £327,700.

The applicants were a married couple with one child and were looking to borrow the full amount of the Right to Buy purchase price over a 20 year term.

The main applicant was self-employed with income from a shop, a partnership with brothers and background commercial Buy to Lets.

The main applicant also had a County Court Judgement (CCJ) from 2018 that had been satisfied around 10 months prior to application. The second applicant was a nursey worker who had some minor defaults dating back over a year ago.

We were able to help this family secure their mortgage on our Versatility range, considering the Right to Buy at 100% of the purchase price, the self-employed multiple income sources and the historic adverse credit.

A flexible, common sense approach

If you have a case that needs a flexible and personal approach to lending, call our Intermediary Sales on 01623 676360 or email brokers@mansfieldbs.co.uk.

Impact Specialist Finance

Are your clients looking to renovate their property? Have they considered Heavy Refurbishment Finance?

A heavy refurbishment loan is a short-term loan required for larger jobs that aren’t just cosmetic. This could involve, work that requires planning, is structural or that will result in a change of use to the property.

Impact Specialist Finance Impact has access to a comprehensive panel of bridging lenders. We have built strong relationships with these lenders who will take a view on all aspects of an individual case, including limited distribution lenders.

Access a fast bridging solution, call the Impact Bridging team on 01403 272625 or email bridging@impactsf.co.uk

Just

Vulnerability – a term people often won’t identify with

So how can you help them? Do you have a system in place to flag a client’s vulnerability during your interactions with them? Our template wellbeing checklist may be a good place to start.

Aldermore

Play our interactive EPC game

To help you support your landlord clients we’ve created an EPC game which shows what improvements could be made to a typical property to bring it in line with a minimum EPC level C.

BM Solutions

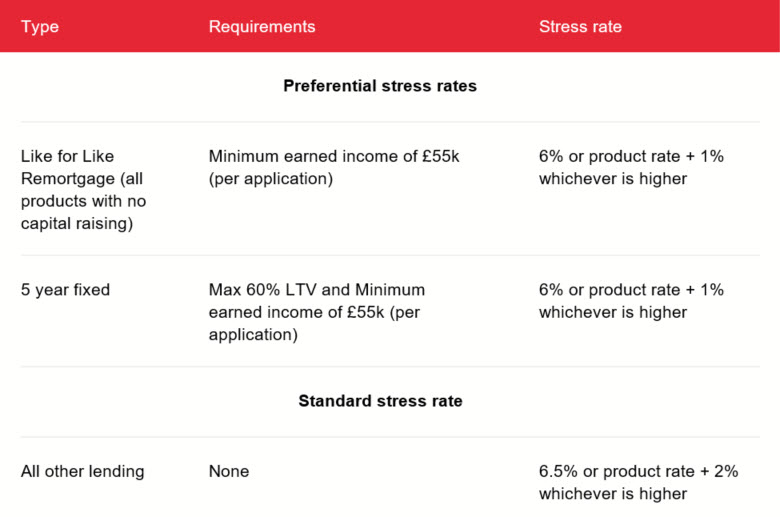

Updated stress rates

From Monday 6th March, we are removing the maximum 60% LTV restriction for qualifying like for like remortgages.

The stress rate for all like for like remortgages is now 6% or pay rate +1%, whichever is higher, for qualifying customers. To qualify customers must have a minimum income of £55,000 or more across the application (Applicants 1 and 2 only).

Qualifying income can be made from:

- All employment

- Self-employment

- Pension income

- Profit from UK land and property.

Example: 2 year fixed like for like remortgages, rate 5.1% = stress rate of 6.1%

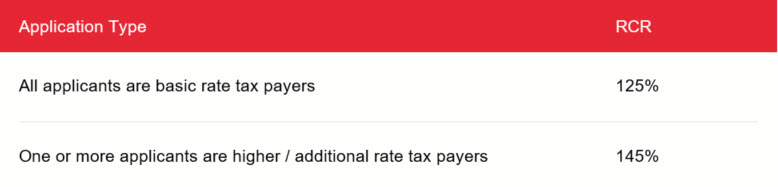

Rental Cover Ratio’s (RCR) remain unchanged

To work out which RCR is applicable, the below income is used to establish whether customer earns over £50,271 pa (£43,663 pa in Scotland).

- All employment

- Self-employment

- Pension income

- 80% share of the gross rental income for all properties that the applicant will own on completion.

Example: Joint purchase application with existing BTL gross rental income of £10,000pa and new purchase rent of £10,000pa = £8,000 per applicant

Further borrowing

- 125% RCR if all customers are basic rate tax payers and 145% if one or more customers are higher / additional rate tax payers.

- Stress rate is 6.5% or pay rate +2%, whichever is higher.

If you have any queries, please refer to your Business Development Manager.

The Exeter

It’s HealthWise time!

Did you know that our member benefits app, Healthwise, could save your clients up to £1,800 a year? For the past two years, we’ve launched our annual HealthWise report and it’s back again! Let’s have a look at the highlights from the year…

- In 2022, our members gave our services an average score of 4.7/5

- On average more than 3 out of 5 are repeat users of the service

- The number one service was Remote GP appointments, accounting for 61% of usage

To see how your clients are using HealthWise, why not grab a coffee and have a read of our report?

Lendinvest

How much do AVM’s save brokers and their customers?

LendInvest crunched the numbers and found how many days brokers can save waiting on valuations – and how much money they can save their clients – when they use AVMs.

TSB

BTL Stress Rates criteria changes

From Tuesday 7th March, TSB made changes to its lending criteria.

Buy to Let stress rate

- The stress rate applied to Buy to Let applications is Please see the table below for more information.

| Application Type | Less than 5 year products | 5 year or more products |

| Re-mortgages with no additional borrowing (excluding residential to BTL / Let to Buy) | Higher of 6.50% or product rate +1% | Higher of 6.50% or product rate +1% |

| All other application types (including residential to BTL / Let to Buy) | Higher of 7.50% or product rate +2% | Higher of 6.50% or product rate +1% |

Stress rate for background Buy to Let mortgages

- The stress rate for background Buy to Let mortgages, on Residential mortgage applications is reducing from 7.00% to 6.50%.

Any DIPs or pipeline applications started before 7 March, won’t be impacted by these changes.

For more information please contact your National Account Manager.

The Mortgage Lender

Real life lending stories, all together in one place

At The Mortgage Lender (TML), we are proud of our supportive, can-do approach. We call it Real Life Lending, and it’s how we’re able to help brokers like you get the right outcomes for your clients, even in complex, challenging cases.

We’ve put together a collection of studies, featuring recent real life cases. Each example highlights how great collaboration can deliver successful outcomes, for everyone involved.

Find out how we:

- Fast-tracked a complex FTB case in just five days where the self-employed client had a history of missed payments

- Worked with a specialist property finance comparison site to put together a complex BTL package, including 14 separate mortgages for one experienced landlord

- Coordinated a complex refinance deal by getting three specialist lenders to work together

We’re publishing new case studies on a regular basis. Take a look and contact your BDM to discuss your own case.

Melton Building Society

Shared Ownership return to market USP’s

Melton Building Society return to the Shared Ownership market with the launch of their new products.

Melton’s Shared Ownership USP’s are as follows;

- 90% max LTV on new build houses (flats 60% LTV)

- Family gifted deposits considered up to 50% of purchase price

- 5% builders deposits & incentives considered

- Available across England & Wales

- Restricted staircasing clauses considered

- No credit scoring

- Satisfied adverse 4 years + disregarded

- Manual underwriting

For full details of our products and A-Z lending criteria, please visit our website www.themeltonbrokers.co.uk or call our dedicated Broker Sales Team on 01664 414144 option 1.

MPowered Mortgages

Launches with mortgage clubs

In case you missed it, here at MPowered Mortgages we’ve expanded the distribution of our prime residential range.

You can access our suite of products by registering today.

Why your customers will love MPowered

- Free valuation available on every application

- £500 cashback for every remortgage case

- Up to 5.5x LTI available for employed applicants

Register now to access our suite of products

- Fill out our quick and easy registration form

- We’ll verify your FCA number and details

- Within 24 hours, we’ll notify you to confirm your access

Market Harborough Building Society

Launches multi-generation mortgages

Developed in response to a growing number of enquiries from intermediary partners, the new products are designed to meet the needs of family and friend groups who want to buy a home and live together.

Suitable for groups of up to four applicants, the multi-generation mortgage range caters for a wide range of complexities including unusual properties (including those with annexes and large acreage) and non-standard income.

Key features of the range include:

- No family connection required

- Interest only solutions available

- Lending up to the age of 85, and a maximum LTV of 75%

- Joint borrower, sole ownership solutions available

You can read more about the new multi-generation mortgages here. Alternatively, please call the Intermediary Team on 01858 412345.

LiveMore

Why LiveMore are the go-to partner for 50-90+ cases

LiveMore products are designed specifically for your 50-90+ clients. Here are some unique ways LiveMore can help when service or products make a case tricky.

Service

- We offer direct access to our underwriters – talk on the phone throughout your case

- They manually underwrite every case, so your client always gets a fair hearing

- Our simple quote and application process helps us to make quick decisions

Products

- Retirement Interest Only (RIO) is up to 75% LTV. Term Interest Only (TIO) is up to 65%

- Our 5 and 10-year fixed rates are available across a range of loan sizes

- If you call your client each year to check in, our Ongoing Proc Fee rewards your time and care

Sound helpful for a case you’re working on? Get in touch to discuss. You can do that by clicking here.

Landbay

Landbay hosts Spotlight Webinar on BTL affordability

Register now for Landbay’s online session exploring affordability in the current buy-to-let market. Get a better understand how to calculate affordability and how you can help your landlord clients in these challenging times.

2 PM Friday 24th March. You can REGISTER HERE.