UPCOMING EVENTS

LATEST BLOG

QUERY OF THE WEEK

Virtual Workshop

Tuesday 9th October 2021

New Build Forum

Thursday 18th November

Platform

‘Know economic abuse’

By Brad Rhodes, Corporate Account Manager, Platform

Will any lenders look at a property with 14 acres of land, with a shares and submetered water supply with the surrounding properties?

The Mortgage Lender

What the end of furlough means for mortgages

To say things have changed in the last couple of years would be an understatement. The way a lot of us work, earn a living and pay for the roof over our heads is different now. And although the government’s furlough scheme is coming to an end, we’re not going back to the old pre-pandemic normal any time soon. The good news is that the New Normal is positively brimming with opportunities, find out why with some valuable insights from our talented underwriters.

Many people may actually be better off

Although some sectors may have suffered redundancies, many of those who’ve kept their jobs have been spending less, and may even have been able to save. That means more first-time-buyers with a deposit (particularly with our improved LTVs), and more people looking to remortgage and renovate. And working from home has inspired many to think about moving up the ladder to a bigger home.

Job vacancies and salaries are up, particularly in a number of key sectors. In fact the Bank of England predicts unemployment will rise only slightly as furlough is phased out – a much better outcome than was initially feared.

And contracts are getting better, with many new jobs coming with three or six months’ notice rather than just one. Which means more security, and potentially more successful mortgage cases for you.

We’re also finding that people on furlough have been trying new jobs, starting businesses, going freelance and generally looking to change. In many cases, they’re doing better than ever.

When a challenge is an opportunity

Of course the pandemic has caused financial problems for a lot of people. There’s been a big increase in defaults on phone bills and utilities, while a lot of people have taken advantage of mortgage holidays. Lockdown even caused a spike in relationship break-ups, throwing finances into turmoil for some.

This all means brokers are in greater demand than ever. We’ve seen an increase in advisers searching for flexible criteria for prospective mortgage borrowers experiencing ‘financial complications’.

Our view is that setbacks are usually temporary. And because all our underwriting is done by real people, giving fair consideration to even the most complex cases, we’re often able to help where other lenders won’t.

This all means brokers are in greater demand than ever. We’ve seen an increase in advisers searching for flexible criteria for prospective mortgage borrowers experiencing ‘financial complications’.

Better LTVs and criteria

At The Mortgage Lender we’ve been busy right through the pandemic, working hard to consider real-life loans for people in real-life circumstances. We’ve granted lots of new mortgages to people on furlough, for example. Now, as we (hopefully) come out of the crisis, we’re introducing new and better criteria for the New Normal. This should allow you to package even more successful cases, even for applicants with complex finances. The newly self-employed, for example, or people who rely on commission and overtime, or the ones who did miss the odd payment or two when things got tough.

We’re also bringing in new, higher LTVs. Great news for first-time-buyers, re-mortgagers and BTL landlords.

Let’s not let them down

We love to lend, and we can do that better when we know the whole story. So we ask brokers to prepare well before submitting applications. That way we’re likely to give you a successful outcome, without wasting anyone’s time.

You’ll find criteria and checklists on our website. You can also leave notes on the portal to highlight anything you think we might query. It’s always important to give us the documents we ask for, but don’t give us more than we need, as it may just hold things up.

Remember we do things the real life way, with the right people looking at applications in a supportive but responsible manner. So you can always chat through a case. Call our sales hub, or contact your local BDM. Once a case has been submitted, you can usually speak directly to an underwriter.

Saying farewell to furlough will have its challenges, but it comes with some real opportunities, too. There’s a great future ahead – and we’re working hard to make sure we’re all ready for it.

We’re here to help

Come to think of it, why not start that conversation now? Visit www.themortgagelender.com or contact our Sales Hub on 0344 257 0418

West One

Spotlight on HMO’s: An Introduction

2021 has been a strong year for the buy-to-let sector, the rapid growth of property prices in the last 12 months has resulted in rental remaining a popular option, with many priced out of home ownership. This increase in house prices coupled with changes to taxation for BTLs, safety measures and tenants’ rights means that landlords are increasingly needing to be more strategic with their approach.

An increasing number of landlords are looking to HMOs (House in multiple occupation) as a way to maximise the returns on their investment. So just what is a HMO and what are the benefits and risks involved? West One investigate…read the article in full, A beginners guide to HMOs.

Foundation Homeloans

Introducing key residential criteria

As a specialist residential mortgage lender, we can help you with your specialist residential mortgage cases. So, we thought we would introduce you to our key criteria:

- Expert solutions for clients with complex and multiple employment – from recently self-employed, directors, partners and contractors, to PAYE full and part time

- Maximise income – 100% of more types of income considered – including high levels of commission and bonuses, trust, investment and pensions incomes, share of net profits, retained profits, salary dividends

- We underwrite to your client’s individual circumstances – and our underwriters call out to you to get those cases sorted!

So it’s time you registered with us

- Experience – over 1000 years of combined sales and underwriting knowledge

- Your local Sales Manager – they will help you every step of the way

- Broker Hub – if we think you will benefit from knowing it, it’s there

So, if you have a residential client – whether they have recently changed jobs, are self-employed, have income from unusual sources, or some blips on their credit record, we can help.

Legal & General

A look back on Breast Cancer Awareness month 2021

As October’s Breast Cancer Awareness Month comes to an end, we look back over the stories shared by the people living with, or supporting those with, breast cancer.

This month we have been sharing stories about the prevalence and impact of breast cancer in the UK and around the world. Breast cancer is now the most common cancer globally, with 2.3 million women diagnosed and 685,000 deaths in 2020 alone.

With the disease on the increase, we’ve been hearing from our customers about the support they’ve received through their breast cancer diagnosis. We’ve also gone behind the scenes with our claims handlers to find out more about the specialist training they receive to help them deal with vulnerable claimants.

How breast cancer affected Natalie’s finances

Because a cancer diagnosis tends to come without warning, many people may not have the financial security in place to immediately cover income, have increased bills or rack up travel costs to medical appointments.

For Natalie, one of our critical illness claimants, her breast cancer diagnosis came at a time when she was already dealing with unrelated chronic illness and had already used the majority of her sick pay from work. She shared how critical illness created financial breathing space for her and her family.

How Lucy’s dedicated nurse helped her

When Lucy*, a single mum of two, was diagnosed with breast cancer, she found it difficult to know who to talk to. Her teenage daughter was worried her mum might die, and Lucy’s increased anxiety after her diagnosis left her feeling apprehensive and worried about her future. She was facing surgery and the possibility of chemo’ or radiation and was looking for support.

When Lucy claimed on her critical illness policy, the claims team also referred her to RedArc Assured Ltd as she has access to Wellbeing Support included in her policy. RedArc assigned an experienced, registered nurse to Lucy, who took the time to get to know her and to understand her needs during one-to-one phone calls.

Lucy told us about the practical and emotional personal support she received from her nurse, and how it helped her cope with her diagnosis.

Dealing with breast cancer claims with compassion

Our claims team are the first point of contact for individuals and families who have been recently diagnosed with an illness or have passed away. We have 20 trained claims assessors who deal with every claim with compassion and understanding. To make the process as personalised as possible, claimants are given their own dedicated claims handler to take on their case.

We understand that handling claims means speaking to people who are potentially very vulnerable. And our recent partnership with the Samaritans has given handlers the support they need in dealing with difficult conversations with their customers. Our handlers’ Samaritans’ training covers two integral skills: listening and conversations.

Listening sessions are tailored for our non-medical claims team and covers the key listening skills when dealing with our customers, while our conversations session is tailored for our medical claims’ teams. It includes the listening skills, and the addition of how to hold a conversation with our customers to ensure we can be supportive.

Find out more about our Samaritans training

For more information on breast cancer including signs, symptoms, and where to get help, visit Breast Cancer Now

*Name has been changed

TIPTON & COSELEY

Let to Buy Focus Week

As we reach the end of this month’s In Focus updates, this week we will be sharing with you some real-life Let to Buy case studies discussed during our daily Mortgage Referrals Committee meetings.

Visit our website to view our currently available Buy to Let products, or contact our dedicated BDM team using the chat facility on our website.

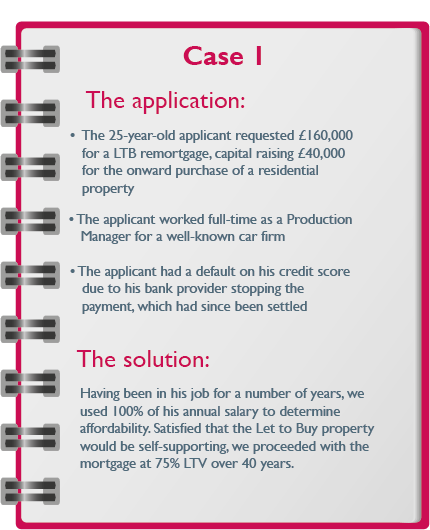

Case 1:

• The 25-year-old applicant requested £160,000 for a LTB remortgage, capital raising £40,000 for the onward purchase of a residential property

• The applicant worked full-time as a Production Manager for a well-known car firm

• The applicant had a default on his credit score due to his bank provider stopping the payment, which had since been settled

Our solution:

Having been in his job for a number of years, we used 100% of his annual salary to determine affordability. Satisfied that the Let to Buy property would be self-supporting, we proceeded with the mortgage at 75% LTV over 40 years.

Mortgage Sales & Distribution Senior Manager, Evan Crosskey, said: “The applicant in this case had been turned away from high street lenders due to the default affecting his credit score. However, due to our policy to not use credit scoring as a deciding factor, we were happy to proceed with the mortgage.”

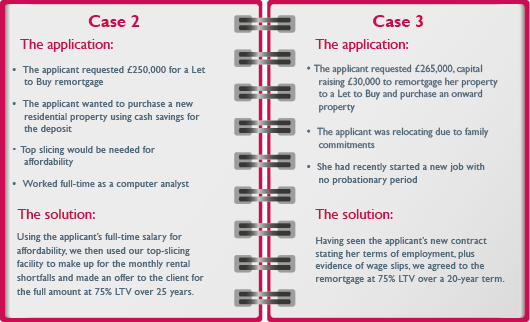

Case 2:

• The applicant requested £250,000 for a Let to Buy remortgage

• The applicant wanted to purchase a new residential property using cash savings for the deposit

• Top slicing would be needed for affordability

• Worked full-time as a computer analyst

Our solution:

Using the applicant’s full-time salary for affordability, we then used our top-slicing facility to make up for the monthly rental shortfalls and made an offer to the client for the full amount at 75% LTV over 25 years.

Case 3:

The application:

• The applicant requested £265,000, capital raising £30,000 to remortgage her property to a Let to Buy and purchase an onward property

• The applicant was relocating due to family commitments

• She had recently started a new job with no probationary period

The solution:

Having seen the applicant’s new contract stating her terms of employment, plus evidence of wage slips, we agreed to the remortgage at 75% LTV over a 20-year term.

TEACHERS BUILDING SOCIETY

A more seamless way to get from old to new

TFI Short Term Mortgages

- Do market conditions mean it might not be the right time for them to sell?

- Have they found a dream property that they want to secure straight away?

- Perhaps they need time to carry out remedial works to both a new and old home?

- Or is it just financially more prudent to leave investment funds untouched for now?

…whatever the reason, there’s no need for them to worry about crossing the bridge from old home to new.

An ERC free short term mortgage from Teachers for Intermediaries offers a penalty free solution that can help avoid financing issues taking their tolls on your clients. Find out more and contact Teachers for Intermediaries today on 0800 378 669 or visit the TFI website here.

Ralph Punter, BDM at Teachers For Intermediaries, said:

“Trying to meet deadlines for the sale of one property or purchase of another can add undue stress to what should be a simple journey from one home to the next. When you’re dealing with more unusual homes, at higher values, in more rural locations or with additional features that difficulty can be compounded, and the financial and emotional toll can be high. Whilst bridging loans offer a solution for a few months, in some cases that won’t be long enough. An ERC free short term mortgage can offer a more flexible solution.”

TBMC

Case study: Complex HMO

- Property value: £250,000

- Loan required: £187,500

- Rental income: £1,500 pcm (£300 per month, per room)

- Loan-to-value: 75%

Case outline

Our client had owned one buy-to-let property for 12 months and was now looking to purchase an HMO to maximise his rental income. His income was around £16,000 and he currently lived with his parents.

Property consisted of 5 bedrooms each with a kitchenette and en-suite facilities, a shared kitchen and large bathroom but no shared living space.

It was a large, 2 storey, leasehold flat above a parade of shops on a small high street. No takeaways or pubs immediately next to the property but present at the end of the high street.

The client planned to let the property to students.

Solution provided

Many lenders were put off by the commercial elements and lack of shared communal space. The property was deemed unsuitable for family letting.

The case was discussed with several lenders and proceeded with one who later declined the case following the valuation.

We promptly placed it with an alternative lender using the existing case details and obtained a mortgage offer.

The process from mortgage application to offer only took around 5 weeks despite the initial declined valuation.

Find out more, contact TBMC 029 2069 5400.

VANTAGE FINANCE

Making the impossible possible

Financing a property at auction or purchasing an un-mortgageable property can feel like impossible situations, however they don’t need to be. A short-term bridging loan can be used to ‘bridge’ the gap between the time of purchase and arranging a regular mortgage, making the impossible possible.

At Vantage we are passionate about ensuring your clients are able to move with the market, securing the finance they require as and when they need it. By working with Vantage Finance, you will receive bespoke financial support that is tailored to the needs of your client.

Why choose Vantage?

- Rates from as little as 0.43%.

- Applications are approved in days, not weeks.

- Up to 80% LTV and 100% with additional security.

- Loans up to £30 million+

- Terms from 1 day to 23 months.

- Fantastic commission rates for introducers.

- Adverse credit considered.

Our extensive lending panel stretches across the high street, challenger banks, specialist lenders, and private banks, offering you unrivalled access to a wide range of products and rates.

If you would like more information on the above or if you have any questions or cases we can assist you with, drop us a line or give us a call today on 01753 883195.

LEEDS BUILDING SOCIETY

We’ve re-entered the HMO market

Here at Leeds Building Society we understand that a “one size fits all” approach isn’t always best. That’s why we’ve decided to re-enter the Houses in Multiple Occupation (HMO) market, once again providing mortgages for both small and large HMOs. Using specialist valuers and underwriters we provide a service that’s tailor-made for both. Find out more: new-lending-range-B.

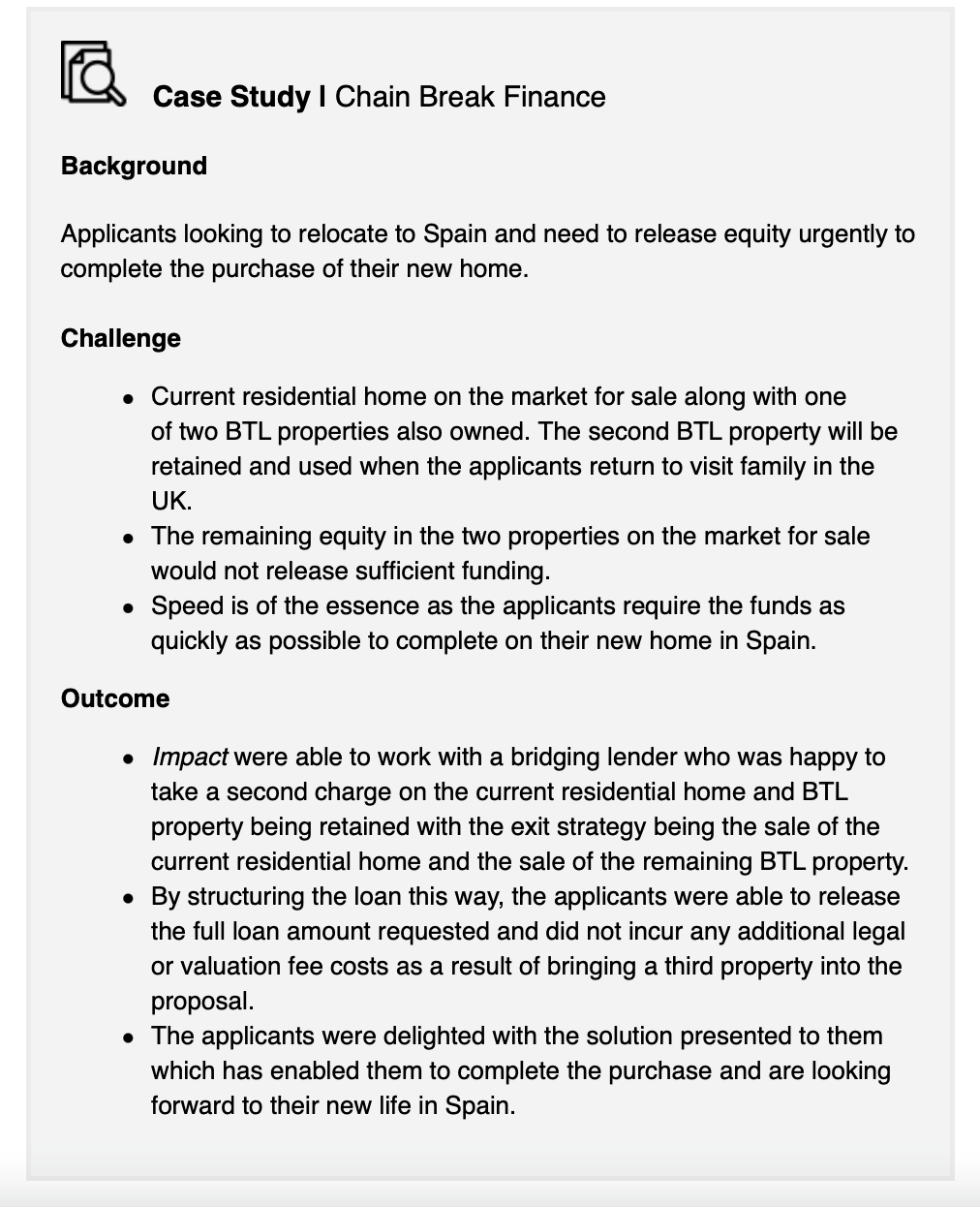

Impact Specialist Finance

Your Specialist in Chain Break Bridging Finance

Chain Break Finance is a bridging loan that helps individuals buy a new property before selling an existing property. The upside of chain break finance is that it can be arranged very quickly so that the chain remains intact, and they can move in with minimum delay.

Impact Packaging has access to a comprehensive panel of bridging lenders. We have built strong relationships with these lenders who will take a view on all aspects of an individual case, including limited distribution lenders.

Access a faster solution to your Bridging Finance by contacting

the bridging team at Impact Specialist Finance.

Call: 01403 272625

Skipton For Intermediaries

Loan to Income policy changes

LTI Policy

With effect from Monday 1st November Skipton have made the following changes to our maximum Loan to Income (LTI) caps, which will make mortgages more accessible for your clients who meet the criteria.

Key Changes

- Help to Buy and Shared Ownership: Maximum LTI 4.5

- LTV 75% or less and income over £80,000: Maximum LTI now 5

- LTV between 76% and 85% or income less than or equal to £80k or interest only: Maximum LTI now 4.75

- Income less than or equal to £40k or LTV greater than 85%: Maximum LTI 4.49

To find out more, visit our affordability calculator on our website.

Keystone Property Finance

NEW Spectacular Cashback Products

Keystone Property Finance are excited to launch their new enhanced cashback offering! This new range comprises of three different tiers for your buy to let landlord clients.

The specialist buy-to-let lender has replaced its larger loan cashback offer, which paid £750 on loans between £150,000-£500,000 and £1,000 on loans between £500,001-£1m.

The new cashback offering levels are:

- £1,000 on loans between £150,000 and £400,000.

- £1,500 on loans between £400,001 and £750,000.

- £2,000 on loans between £750,001 and £1m.

If you have any questions or need any assistance with your buy to let case enquiries, please contact Keystone’s Business Development Managers on 0345 148 9086 or email enquiry@keystonepropertyfinance.co.uk.

Hinckley & Rugby for Intermediaries

In Focus – Real life Let to Buy cases

As we reach the end of this month’s In Focus updates, this week we will be sharing with you some real-life Let to Buy case studies discussed during our daily Mortgage Referrals Committee meetings.

Visit our website to view our currently available Buy to Let products, or contact our dedicated Business Development team using the chat facility on our website.

In case you missed it, Hinckley & Rugby for Intermediaries has six new team members! Find out about our team here.

If you have an unusual or complex case in mind that you would like to discuss, please contact our Business Development Team by emailing development@hrbs.co.uk or by using live chat on our website.

Fleet Mortgages

Buy To Let Product Guide

From 3rd November 2021 Fleet have made the following changes to their Standard,

Limited Company & LLP and HMO & MUFB.

Highlights

- Rental Calculations from 125% @ 2.99%

- Up to 80% LTV

- Free / Discounted Valuations

- Lifetime Tracker Rates with no ERC’s

- Price Reductions

- All 5 year products benefit from payrate rental calculations

- IMPORTANT – COVID-19 valuation rules

Important Notices

Please read and advise your client new pre valuation requirements here.

Gatehouse Bank

Finance Criteria changes for our Buy-to-Let and Home Purchase Plans

Gatehouse have updated their Finance Criteria for our Buy-to-Let (BTL) and Home Purchase Plan (HPP) products. Listed below is a summary of the key changes.

In addition, across all our products, the term ‘Application Fee’ has been renamed ‘Product Fee’.

HPP and BTL Criteria Highlights:

- The number of bank statements required for employed and self-employed UK Expat and International resident BTL and HPP applicants has been changed to 4 months personal, 6 months business and the need for a UK credit footprint has been removed

- Overtime, commission and bonuses will now be considered for all applicants (previously essential workers only)

- Following Brexit, various changes have been made by the UK Government to the status of some UK residents from the EU. EEA/EU Nationals can have either ‘settled status’ or ‘pre-settled status’ depending on their time resident in the UK, and this may affect the documentation they are required to provide and the maximum FTV limits they are entitled to apply for. This applies to UK residents only. Please see our Criteria guides for more information

- London and big city allowances will be considered for income purposes at 100% of amount received (HPP & UK resident BTL only)

- Director/Shareholder loans will be considered (subject to terms) on BTL cases, but inter-company loans will not be accepted

HPP only Criteria Highlights:

- Maximum finance over £1m has been increased to 75% FTV from 70%

- HPP International residents maximum FTV increased to 80% from 75%

BTL only Criteria Highlights:

- Rental Top Ups are no longer allowed for International BTL applicants

- Only UK registered Limited Companies, SPVs and LLPs will be accepted on any BTL/HMO/MUFB application regardless of the location of the applicants. Therefore, offshore registered SPVs/Limited companies or LLPs will no longer be accepted

- SPVs with negative equity will not be accepted

- Director’s loans to a Limited Company/SPV will be considered but inter-company loans will not be accepted

- Child Benefit and Working/Child Tax Credits will no longer be accepted for income purposes on BTL cases

- Zero-hour contracts will now be considered for UK resident BTL applications

- Maximum age of 99 years has been removed, however, for cases where there is reliance on income to support the affordability, the maximum age remains at 85 years

Our updated Criteria guides can be found here. Products are available to UK residents, UK Expats, International residents and UK registered corporate entities to purchase or refinance property in England and Wales, details of which can be found here.

If you have any queries or require further information our team remains available via phone and email, details of which can be found here.

Key Partnerships

See how much equity your clients could release from their home in an instant

Key Partnerships, the equity release referral service, has many useful tools and resources to help your client in their decision making process including the Loan to Value (LTV) tool to help you determine how much equity your client could release from their home.

The LTV tool calculates the potential release based on your client’s age, property value and health. This can help your client understand how equity release could benefit them in their retirement. For example, if the youngest client is aged 55 with a property value of £400,000, they could possibly release up to £118,000 or 29% of the value of their property or up to £152,000 (38%) if they are unhealthy*.

See how much equity your clients could release here.

Don’t forget to register if you would like to refer your client to Key Partnerships.

*A set of simple medical and lifestyle related questions are used to work out an enhanced LTV rate. Actual rates will vary according to the specific medical underwriting of each client.