UPCOMING EVENTS

LATEST BLOGS

QUERY OF THE WEEK

Virtual Workshop

Tuesday 14th September at 10:00am

Featured partners:

Keystone Property Finance

AIG

Precise Mortgages

Teachers for Intermediaries

Kent Reliance for Intermediaries

Specialist lending solutions for limited company landlords

Q – Can you please find me any lenders that will look at a client aged 63 at application looking for a residential re-mortgage? My client has a professional landlord BTL income and a small amount of pension, by the end of the term he will be in excess of 75 years old.

Virtual Workshop

Thursday 30th September at 10:00am

Featured partners:

Aviva

Kent Reliance for Intermediaries

Accord

Masthaven Building Society

NatWest

A welcome home for remortgages

TMA Club

Scottish Mortgage Awards

Legal and general gi

important ASU PRODUCT UPDATE

Legal & General have recently undertaken a full-scale review of their ASU products (Lifestyle cover and MPPI). As a result of this review they have made the difficult decision to exit the ASU marketplace for new business and renewals of existing business.

Whilst ASU represents a small part of their GI portfolio, it was important for them to ensure ongoing protection for their customers against the backdrop of sizable challenges, such as the current pandemic and economic uncertainty.

Therefore, they have selected AmTrust Europe Limited as the new insurer. AmTrust Europe Limited will be providing replacement insurance policies through the Wessex Group (WIMS Limited) to all existing customers from 1st August 2021 onwards as they exit the ASU market. There are no proposed changes to customer’s cover or terms and conditions for at least the first year of renewal and commission will continue to be paid at the same rates, however it will be moving to non-indemnity payments.

In addition, from 1st June 2021 onwards they will be outsourcing their existing in-house claims service for the policies they insure to the Wessex Group to help provide improved servicing at this extremely challenging time.

gATEHOUSE bANK

95% FTV Home Purchase Plan for FTBs and 90% for purchasers, home movers and those refinancing

Great news! Gatehouse Bank have launched their new dedicated 95% FTV Home Purchase Plan (HPP) products available to UK resident first-time buyers only. In addition, we have also launched HPP products up to 90% FTV for UK resident purchasers, home movers and customers refinancing their property.

Key highlights include:

- Up to 95% FTV now available to first-time buyers resident in the UK

- Up to 90% FTV available to UK resident first-time buyers, purchasers, home movers and customers refinancing

- Finance amounts between £100K and £500K on all products and FTVs

- All available on 2 year and 5 year fixed terms

- Up to 95% FTV on new Build Houses and up to 90% FTV on New Build Flats

- Our full HPP product range can be found here and our new Criteria for finance above 80% FTV can be found here

To provide advice on HPP products you are required to hold specific HPP permissions with the FCA. However, you may be able to refer your clients on an introduced basis, details of which can be found here.

These new products complement our existing range available to UK residents, UK Expats, International residents and corporate entities looking to purchase or refinance properties in England and Wales. Our full range of products can be found here.

Our team remains available to deal with your queries via phone and email, details of which can be found here.

West One

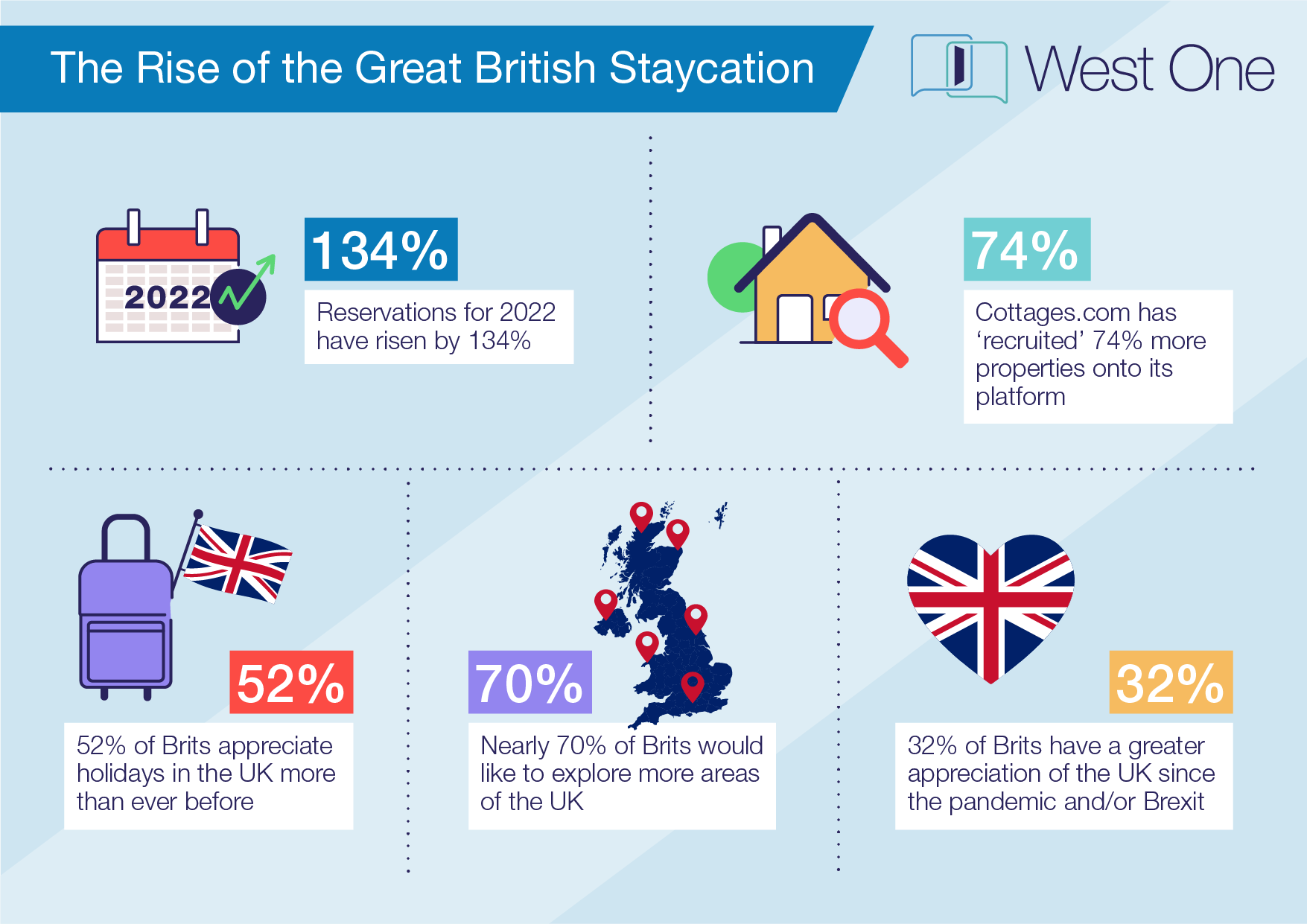

Staycation Wishlist

The number of Briton’s choosing to holiday in the UK this year has led to 2021 being dubbed the year of the staycation. This combined with the opportunity for higher profit margins has led to many property investors exploring the opportunities within the holiday-let market.

We’ve created a wish list of our top 10 UK staycation locations, looked at what the average property price is and the rental opportunities in each area.

Find out which areas have the biggest potential for holiday let landlords: https://www.westoneloans.co.uk/west-ones-summer-staycation-wish-list

Purchasing or refinancing a holiday let

At West One, our specialist buy-to-let product range is available to amateur and professional landlords looking to finance complex transactions including Holiday Lets.

Key features of our Holiday Let mortgages:

- We lend to first time landlords with no holiday letting experience.

- Available to individuals, limited companies, and expats.

- No minimum income.

- We can accommodate short term lets and serviced accommodation (Airbnb) which means the property does not have to be in a typical holiday destination.

- Holiday lets are assessed on an AST rental basis.

- The property must be suitable for standard AST rental.

- There must be no restrictive covenants relating to holiday letting (Seasonal restrictions, holiday let usage only).

- We wouldn’t lend on a holiday let complex or in an area predominantly holiday let property due to resale potential being limited.

If you have a client looking to purchase or remortgage a holiday buy-to-let, please contact your BDM or the broker support team on 0333 123 4556 or email btlbrokersupport@westoneloans.co.uk.

Kent Reliance for Intermediaries

Try our brand-new online criteria guide

Our new online criteria guide offers a complete overview of our latest product solutions, and how we can support your residential and buy to let customers – all available at the click of a button.

Limited company loans, shared ownership, HMOs and complex income – whatever the case, our guide could be essential in solving your cases.

For us, criteria is only the starting point of a conversation. Our flexible underwriting and individual case assessments, our business development managers are happy to discuss your cases – even if they don’t fit our normal criteria, so get in touch today.

LANDBAY

Landbay improves its green portfolio

Landbay launched its first green products in June and now we are making them even more competitive. They provide landlords with the means to meet tomorrow’s challenges by helping to improve existing property portfolios and become more selective when investing in purchases where extra energy efficiency measures can be promoted.

We spent time considering the issues around green mortgages but on their own they only provide part of the puzzle around helping to improve energy efficiency. We look to government to recognise the value that the private rental sector brings by offering greater incentives for landlords to be proactive in greening their portfolios. By offering rebates on the extra stamp duty levy on BTL property purchases for example, in harness with new green mortgages could provide a significant catalyst for a greener rental sector.

Two months into our green mortgage range and the interest from intermediaries has been incredible. We expect that by introducing even keener rates and a 70% LTV green mortgage, we can help more landlords move to greener alternatives.

We will continue to maintain our highly competitive stance in the market to ensure a really strong year has an even stronger finish.

Got a case in mind? Then please get in touch using our BDM Finder.

LEGAL AND GENERAL Protection

The 6 myths and misconceptions of protection #3: ‘It’s too expensive’

In his fourth blog in the series looking at the myths and misconceptions of protection, Robert Betts, Market Development Manager at Legal & General, discusses the third most common misconception why clients don’t have income protection – that protecting their income is too expensive. But, Robert says, after a closer analysis of a typical person’s outgoings, the real question is, can clients afford not to?

The mortgage lender

Self-employed homeowners struggling with debt

A third of self-employed homeowners have increased their unsecured debts and a quarter have deferred mortgage payments to prop up their finances during the Covid-19 pandemic according to research by The Mortgage Lender.

The survey, which was carried out in March this year among 1,000 self-employed homeowners, or those who want to own their own home, revealed unsecured debts, including personal loans, credit cards, and overdrafts, have risen by an average of £2,312 over the last year.

And a quarter (25 per cent) of the panel said they had taken a mortgage payment deferral, 16 per cent had taken a break of up to three months and nine per cent had deferred payments for between four and six months.

81 per cent of self-employed people in the UK kept up payments on their unsecured debt but 9 per cent missed credit card payments, 5 per cent reported an unpaid personal loan and 8 per cent failed to keep up payments on other debts.

A deterioration in their finances meant that 55 per cent felt they would not be able to borrow the amount they currently owe on their mortgage if it was based on their last year’s earnings.

The Mortgage Lender sales and product director Steve Griffiths said: “The last year has been hard for everyone but the self-employed feel as if they have been disproportionately hit by the pandemic increasing personal debt and deferring mortgage payments just to get by.

“Nearly 60 per cent of the people we asked felt their experience of the pandemic was worse than an employee and the majority didn’t receive any financial support from the Government.

“Nevertheless, there are millions of self-employed people contributing to the economy and the economic recovery. It’s vitally important there is a thriving, competitive specialist mortgage sector that is able to provide criteria and products that meet the needs of this segment of the population to prevent them from being locked out of the housing market or trapped in a home that no longer meets their needs.

“When we launched our residential range earlier this year it was with people like the self-employed, those with complex income and credit impairment in mind.”

For more information visit: www.themortgagelender.com

tbmc

Life after stamp duty – what now for BTL?

Despite the stamp duty incentive coming to an end, there are still strong drivers for landlords to maintain their portfolios and look for opportunities to make additional property purchases.

Average rental yields across England and Wales remain strong and recent data published by Fleet Mortgages supports this.

- End of stamp duty holiday

- Improved rental yields for buy-to-let

- Complex buy-to-let lenders are favoured

- Popularity of buy-to-let brokers

Foundation Home Loans

Maintaining a portfolio barometer

Here at Foundation Home Loans, we are seeing sustained interest from landlords who are looking to both diversify and expand their portfolios. The main source of this activity continues to stem from portfolio landlords and it’s important for intermediaries to keep track of how these portfolios stack up in terms of size, value and structure.

The quarterly BVA BDRC Landlord Panel research forms a good barometer for how portfolios are evolving, so here is a round-up of its Q2 insights into what a ‘typical’ portfolio looks like.

Hinckley and Rugby for Intermediaries

Offering Tailored terms

Hinckley & Rugby for Intermediaries offers Tailored Term across its entire mortgage range.

What is it?

Our Tailored Term is, effectively, a ‘made-to-measure’ add-on which is customisable to suit the needs of the applicants. It is an element which can be applied to any mortgage from our product range and allows the applicants to share the cost of the mortgage over separate time frames.

Let’s give you an example:

- The applicant requested £412,000 to purchase a new residential property

- Her mum and stepdad were joining the mortgage for affordability purposes on a Joint Borrower Sole Proprietor basis

- The applicant could afford to pay £257,000 over a 35-year period based on our assessment for affordability

- Her mum and stepdad, both aged in their fifties, could afford to pay £155,000 over a 16-year period based on our assessment for affordability

We used all of the applicants’ salaries to calculate the monthly payments without using our Tailored Term and then compared them to the monthly costings if we were to add our Tailored Term element.

Monthly payment without Tailored Term:

£2,812.31

Monthly payment with Tailored Term:

£2,122.84

The solution:

Whilst all arties are responsible for the combined mortgage debt over the longest term, the Tailored Term element has allowed the payments to be structured with £257,000 being paid over 35 years and £155,000 being paid over 16 years.

Having passed our affordability checks, we approved the mortgage at 75% LTV.

The benefits:

- All applicants found an affordable solution, with payments structured at a comfortable level

- Applicant one was able to accept financial assistance without being constrained by the age of the older borrowers

If you have an unusual or complex case in mind that you would like to discuss, please contact our Business Development Team by emailing development@hrbs.co.uk or by using live chat on our website.

PURE RETIREMENT

Unplaceables Webinar: 8th September

Join us, for September’s “Unplaceables” Zoom Webinar.

Hosted by Anna Thompson

8th September 10am – 11am

We need your cases!

As the name suggests, this webinar is all about hard to place cases, and we want to discuss your real life cases during the session. Please get in touch if you have something you would like to discuss.

We will also be joined by…

Les Pick – Head of Sales, Canada Life

Nicola Palmer – Business Development Manager, Canada Life

Peter Barton – Head of Equity Release, Ashfords Solicitors

Jane Hanlon & Craig Faulkiner – Advise Wise

vIRGIN MONEY

Say hello to our 10-day Application to Offer Service Commitment!

Getting offers to customers quickly is a great way to impress, so let us help you do that. On 31 August, we restarted our Virgin Money and Clydesdale Bank Service Commitment to send your customer an Offer within 10 days of receiving a fully packaged application. If we don’t, we’ll give them £100. Check the terms here: Virgin Money Clydesdale Bank.

Packaging your application right early on can make all the difference getting that quick Offer for your customer. Check out our Virgin Money and Clydesdale Bank packaging guides to find out what we need.

The remo rise in fall

As we approach the end of summer, make sure you’re ready for the remortgage market this autumn. Have a read of our article on retaining clients and making the most of the upcoming maturity spike.

vANTAGE FINANCE

Take ad-Vantage of our access to the bridging market

Right at the start of the bridging process, master brokers such as Vantage Finance can save both brokers and the borrower time of researching the bridging loans on the market – instead, narrowing down and presenting the best bridging loan terms to match their needs.

Why Vantage Finance for bridging finance?

- 17 years’ experience in all types of bridging finance cases

- Our extensive lending panel stretches across the high street, challenger banks, specialist lenders, and private banks, offering you unrivalled access to a wide range of products and rates.

- Our service is quick and consistent, acknowledging cases within 30 minutes and striving to deliver indicative terms within 4 hours.

- A better understanding of lender’s specific underwriting requirements means we can process applications a lot quicker.

- Expert team committed to 5-star customer service

- We offer one point of contact from enquiry through to completion, always aiming to make the process as smooth as possible.

- We provide a lifetime guarantee – if your client returns to us, you’ll always get a referral fee.

If you would like more information on the above or if you have any questions or cases we can assist you with, drop us a line or give us a call today on 01753 883195.