THE TMA AWARDS ARE BACK…

Have your say!

We recently announced our TMA Awards are back for 2021!

Every year we like to celebrate the hard work and loyalty of our member firms, of all shapes and sizes, and we’re over the moon to be able to see some of you again face to face in November as we celebrate your successes at our Annual Awards on Friday 12th November.

As always, our partner award winners are chosen by you – our valued members.

If you believe you’ve received support from our partners over the last 12 months that deserves to be recognised, vote for them in the relevant categories.

Voting will be open until 5pm Friday 13th August – have your say!

TMA are winners of the Money Age Mortgage Awards!

Thank you to everyone that voted for us in the Money Age Mortgage Awards.

We appreciate the support throughout 2020 and the start of 2021.

#GoingFurther #MAMortgageAwards

Launches ‘First Homes’ mortgage

Chorley Building Society is one of the first lenders in the UK to launch a First Homes mortgage, in support of the UK Government’s scheme.

First Homes are a new form of affordable housing and the scheme aims to help first-time buyers onto the property ladder, with a minimum 30 per cent discount on market price on certain new builds. Prices for properties must not exceed than £250,000 outside of London, or £420,000 in Greater London. The discount is also passed on with any future sale of the property to first time buyers.

The Society are offering a 2 year discount mortgage with an initial rate of 2.39% (a discount of 2.85% from the Society’s SVR) and this is available with up to 95% LTV, of the discounted purchase price.

Kim Roby, Customer Services Director commented: “We are very pleased to be among the first providers in the UK to support the new government backed scheme. It’s important to us, as a mutual, to be able help first-time buyers take their first steps into home-ownership. The scheme prioritises key workers and we are very proud to be able to offer this to some of our most hard-working and dedicated members of the community.”

The Society’s mortgage product also features a green incentive with a £250 cashback available for properties that are EPC rated A or B and provide the EPC certificate no later than 3 months after completion.

Head of Lending, Liz Pearson said: “The ‘First Homes’ initiative is the third Government backed scheme that the Society now offers. Our Help to Buy and Shared Ownership mortgages have proved popular and we’re very pleased to be able to support the Government’s scheme, which is part of their commitment to deliver 1 million homes by 2024.”

Notes to Editors

Chorley Building Society was founded in 1859 to help local mill workers buy their homes and 161 years later, the Society still remains true to its traditional, mutual values of providing an individual service to all its members.

The Society has three retail branches in the North West of England with its head office in Chorley, Lancashire.

For further information on the products mentioned please contact:

Clare Mahood

M: 07879 848958

E: cmahood@chorleybs.co.uk

Launched an Intermediary Product Switch Portal

We’re thrilled to announce that we’ve launched our Intermediary Product Switch Portal for a seamless and simple way to undertake a product transfer for your clients.

Product transfers have been the lifeline for brokers over the past 14 months and are on the increase, with more and more brokers transacting them, rather than them being done by the mortgage provider direct with the client. The challenge for brokers is that legacy systems weren’t built for product transfers and so can be clunky, need a great deal of manual intervention and ultimately eat away at the broker’s time.

We have developed a bespoke solution, in conjunction with brokers, that provides tailored market leading products, offering the best options for the client and can be arranged in 15 simple clicks, taking less than 15 minutes.

To read more about our new Product Switch Portal, take a look here.

Self-employed insight report

Our latest research shows how the self-employed have been impacted by Covid, the difficulties they’ve faced over the past year and how they’re feeling.

We’re ready to hit the road!

Our relationship managers are dusting off their work clothes and looking forward to getting back into the field. They’ll be happy to meet up face to face or virtually.

How to guide on financial crime

During the first 3 months of lockdown in 2020, £11m was reported to have been lost to scams. See how you can identify and defend against financial crime in our new guide.

Self-employed clients income

We’ve been listening to your feedback and have updated our self-employed criteria to allow for the various government support options that your clients’ may have used.

- We have removed the requirement for evidence of funds to support 3 months mortgage payments for all customers, including the self-employed

We can accept income evidence for:

– SEISS Grant/Business Support Grants;

– Job Retention Scheme Payments and Bounce Back Loan;

– Coronavirus Business Interruption Loan

- We can accept cases where the business has previously had employees on furlough, as long as this has not been within the last 3 months.

Please refer to the buttons below for full details of the income evidence requirements or to learn more about our mortgages for your self-employed clients.

Life and Critical Illness cover offers extensive cancer cover and support

As cancer is a condition your client is more likely to claim for, it’s important that they’re supported by a comprehensive policy that will be there when they need it most. LV= Life and Critical Illness cover offers extensive cancer cover and support for your clients beyond the financial payment.

- We cover a wide range of cancers across our full and additional payment definitions.

- £1,000 payment to help your client with any initial costs. This is paid on evidence of diagnosis if their condition and treatment meets the criteria for any of the cancers covered by this policy.

We understand that the impact of cancer isn’t just financial.

- LV= Doctor Services your client and their partner gets access to medical services, including remote GP appointments, second opinion and mental health support.

- Member Care Line including access to a 24/7 counselling line.

- Maggie’s we work with Maggie’s, a cancer charity that provides support for people living with cancer.

To find out more about LV= Life and Critical Illness cover, visit LVadviser.com, contact your LV= Account Manager or call us on 0800 032 4219.

Need to find out the latest on your pipeline applications? Check the Protection Progress Hub

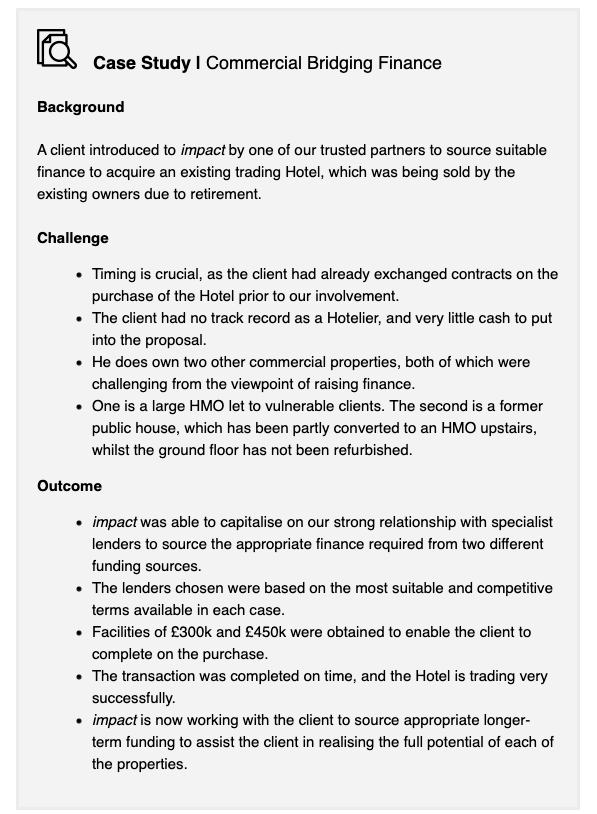

Commercial Bridging Finance

Commercial Bridging Finance is a type of short-term loan that businesses use as they seek a more long-term funding option. This bridges the gap in cash flow so is useful for enterprises who need an injection of cash over a limited period.

Impact Packaging has access to the whole of the market for Commercial Mortgages and Business borrowing. We have built up strong relationships with mainstream lenders, private lenders and lenders that will take a view on all aspects of an individual case, including limited distribution lenders.

Access a faster solution to your Commercial Bridging Finance by contacting Clive Smith, Senior Commercial Consultant at Impact Specialist Finance.

Call: 01403 272625

clive@impactsf.co.uk | impactpackaging.co.uk

Greener Mortgages

We launched three new products last week. The first is a new £1,000 cashback Intermediary Exclusive 5 Year Fixed Rate with £995 fee — be sure to check how much that cashback could save your customers.

The other two are new Greener Mortgage products, which expand our Greener proposition into Shared Ownership. They’re fixed rates available on new builds with an energy efficiency rating of ‘A’ or ’B’ (as shown by an EPC, PEA, or SAP), at 85% LTV, and from 2.28%.

We’ve also reduced selected rates across our Core and Product Transfer ranges by up to 0.52%. Check our Mortgage Update or website to see our latest product details.

New optional repayments feature

Pure Retirement has introduced a new optional repayments feature and a direct debits facility across their Sovereign range, meaning Pure now offer ERC-free partial repayments across their whole product range. The additions feed into a wider, continued commitment to offering product flexibility and the freedom to manage their plans in a way that suits their circumstances.

Alongside the product’s wide lending criteria and downsizing protection, customers now have the flexibility to make annual partial repayments of up to 10% ERC-free within 12 months. The addition of a direct debits facility follows on from its success on Pure’s Classic products, enabling regular monthly repayments with minimal effort and negating the need for customers to arrange payments every month.

FOUNDATION HOME LOANS GREEN ABC PURCHASE MORTGAGE FOR PROPERTIES WITH EPC RATINGS A-C

Foundation Home Loans, the intermediary-only specialist lender, has today (6th July 2021) launched a set of Green ABC mortgage products specifically for buy to let purchases.

The new range consists of three new two-year variable discount rates available to individual landlords as well as limited companies seeking to purchase a property on a variable rate without early repayment charges, and are priced according to the EPC rating of the property.

- Up to 75% LTV

- 2% product fee

- No ERCs

- For purchases up to £1m

- Variable Discount rates

- Available to individuals as well as limited companies

- No limit to the background portfolio size, subject to a maximum of £5m with us

ICR is calculated at 5.5% and stress tested at 125% for limited companies and basic rate tax payers, and 145% for other landlords.

Why use Foundation for your next BTL case?

- Individual or limited company

- Limited companies with complex structures

- Up to 4 directors

- Newly incorporated limited companies acceptable

- ICR of 125% for limited company borrowers and basic rate taxpayers and 145% for others

- No minimum term of employment/self-employment and no minimum income

- Up to 80% LTV on core range

- Loans up to £2M on core range

- No limit to portfolio size, subject to max borrowing of £5m with us

- Cater for specialist properties such as HMOs, short term lets and Multi Unit Blocks

- HMOs: up to 8 bedrooms and MUBs: up to 10 units

- Products for first time landlords

- Ex-pats considered for limited companies only

- Green Mortgages available for purchase and remortgage

Launch of the Just For You Lifetime Mortgage Fixed Early Repayment Charge (ERC) option

On Wednesday 30 June we launched our Fixed ERC option offering clients a guaranteed cost if they choose to pay off their lifetime mortgage early.

With a choice of Fixed or Variable ERC, you can make your lifetime mortgage solutions even more personalised and recommend the one that suits your clients best.

Introducing the 6 myths and misconceptions of protection – and how to bust them

In the first of a series of blogs looking at the myths and misconceptions of protection, Robert Betts, Market Development Manager at Legal & General, introduces the latest Deadline to Breadline report and the common myths and misconceptions of protection it revealed. Here, Robert outlines what you can do to help bust the myths with your clients to show the need for protection.

First timers or seasoned pros? We have something for every landlord.

We welcome business from first time landlords for Standard product applications to seasoned pros with large background portfolios. Our competitive and broad range of products and criteria, featuring zero application fees and fee free product options available, means at Zephyr you can be sure to find something for every landlord.

First time landlord requirements

- At least one applicant must have owned and still own at least one property (residential or buy to let) for a minimum of 12 months.

- Employed – must be in permanent position for at least 6 months and not under notice of termination.

- Self Employed & Contractors – One full year’s evidence of income from accounts or accountants

certificate or SA302 together with a tax-year overview.

Portfolio Landlord highlights:

- No background portfolio stress test; rental income simply needs to cover the Zephyr mortgage

- Unlimited background portfolio

- We partner with eTech’s BTL Hub to allow you to send through additional background information in a quick and simple way.

Got a question about a case? Get in touch with one of our BTL experts!

Call 0370 707 1894

(Mon-Fri, 9am until 5pm)

Meet Charlotte

Charlotte’s worked in financial services for 15 years and now specialises in mortgages. She’s ACCA qualified and has been with Skipton Building Society for over six years.

What will you be doing in your new role as Head of Mortgage Products?

I’m looking forward to working with our mortgage networks/clubs and colleagues on the development of mortgage products, propositions and pricing.

I’m really passionate about the role our sector can play in ‘greening’ the housing market too, so I’ll be exploring how we can support brokers and their clients to build a more sustainable future.

I plan to share our mission of becoming a top 10 lender and look forward to playing a role in helping Skipton realise that ambition.

What are you most looking forward to in your new role?

I’m excited to see us continue to grow our mortgage lending and help more people to own their own homes.

I can’t wait to deliver on our mortgage strategy and work towards our ambition of becoming a top 10 lender.

Why should brokers use Skipton Building Society for Intermediaries?

We’re committed to making things easier for brokers and aim to achieve that in a number of ways. We can adapt quickly to changes in the market with our common-sense approach.

Engagement across all our mortgage teams is consistently high, which means our people will always go above and beyond to help.

Want to hear more from Charlotte? Sign up for the final webinar in our summer series where she’ll be discussing the role of technology in the future of intermediaries with Regional Manager for Intermediaries John Scrivens.

Speed. Service. Simple. Trust Vantage for your bridging finance.

When you or a client need access to finance quickly, bridging finance can often be the perfect solution. These short-term, interest-only loans are ideal for auction purchases, home improvements and renovations, fixing broken property chains, raising money for business purposes or just cash flow.

Vantage Finance is one of the leading specialist finance distributors that can provide fast access to a vast panel of lenders. One call to our team today and our experts will handle your case from application to completion. It really is that simple.

Bridging Benefits with Vantage:

- Super-fast completion times ideal for auction purchases.

- Rates from 0.48%.

- Loans available up to 85% LTV (100% LTV available with additional security).

- Any property type considered (including land).

- 1st, 2nd, and equitable charges available.

- Loans for foreign nationals and expats available.

- Personal and Ltd Co ownership considered both UK and overseas companies and Trusts.

- Regulated and non-regulated bridging loans.

- Development finance/Refurbishment projects from Extensions through to Ground up Developments.

- No early repayment charges.

- No upper age limits.

Contact us now for further information.

If you would like more information on the above or if you have any questions or cases, we can assist you with, drop us a line or give us a call today on 01753 883195.

New BTL range available

‘More’ just may be our favourite word and we’ve just added four more competitive, straightforward mortgage products to our buy-to-let range along with reduced rates and fees across our BTL range, making our products more competitive, for every kind of landlord.

Highlighted Criteria

- £50k minimum loan (unless stated otherwise in the product guide)

- First time Landlords

Steve Griffiths – Sales and Product Director:

“The combination of reduced rates and our Limited Edition with reduced completion fees makes us stand out from our peers. It also offers greater choice for landlords, whether they are looking to raise capital to increase the number of properties in their portfolio or refinance existing arrangements to better suit their needs.”

We consent and encourage for this release to be used in any weekly round up/newsletter/email/social comms if applicable.

If you have any questions or require any further information, please get in touch and let me know.

A guide to HMO buy-to-let

Houses in Multiple Occupation (HMOs) have become a popular property investment choice for landlords in the UK, often providing higher rental yields compared with other property types.

We have created a free guide for you and your landlord clients who are interested in finding out more about the possibilities of investing in an HMO.

TMA UPCOMING EVENTS

Protection HiiT Series

20th July

21st September

Virtual Workshop

Thursday 15th July

CLICK HERE

QUERY OF THE WEEK

Q – What lenders will do a Ltd company BTL for a British client, who has been back in the country for 4 months, they have a residential property and also experience in BTL but no BTL at the moment?

Please give our broker support desk a call on 0330 303 0236 for more information.