THE TMA AWARDS ARE BACK…

Have your say!

On Wednesday we announced our TMA Awards are back for 2021!

Every year we like to celebrate the hard work and loyalty of our member firms, of all shapes and sizes, and we’re over the moon to be able to see some of you again face to face in November as we celebrate your successes at our Annual Awards on Friday 12th November.

As always, our partner award winners are chosen by you – our valued members.

If you believe you’ve received support from our partners over the last 12 months that deserves to be recognised, vote for them in the relevant categories.

Voting will be open until 5pm Friday 13th August – have your say!

Announce lending on Holiday Lets

Last week Keystone Property Finance announced that they have now started lending on holiday lets for the first time amid strong demand from landlords and a boom in “staycations”.

Borrowers looking to purchase or remortgage a holiday let within England and Wales can choose from any one of Keystone’s specialist ranges.

It also means borrowers have access to the green mortgage range, which offers exclusive rates for properties 5 years and older that have an EPC rating of C or above.

The specialist buy to let lender will lend up to 75% LTV on holiday lets for those wanting to borrow up to £750,000 and 70% LTV for those wanting to borrow up to £1m.

To qualify, borrowers must earn a minimum of £40,000 a year, must already own at least one buy to let and their property must be furnished. The rental agreement must not exceed six months.

The borrower’s property will be valued, and the rental coverage will be assessed on the same basis as a standard buy-to-let.

Keystone have launched their holiday let range following feedback from brokers and are currently one of the few lenders to offer these types of loans.

If you have any questions or need any assistance with your case enquiries, Keystone’s Business Development Managers are here to help, call the broker hotline on 0345 148 9086 or email enquiry@keystonepropertyfinance.co.uk.

The Lending Lowdown:

How to package the perfect mortgage case

Doing business with us shouldn’t be hard work.

It should be clear, quick and simple. Always. That’s why we’ve created ‘The lending lowdown’ – a series of helpful content that highlights how we do business and makes your life easier.

To kick things off, we’re giving you the lowdown on how to package the perfect mortgage case – and give your clients the best chance of success.

Key points include;

- Top tips for packaging your case for success

- How to provide bank statements

- How to provide proof of deposit

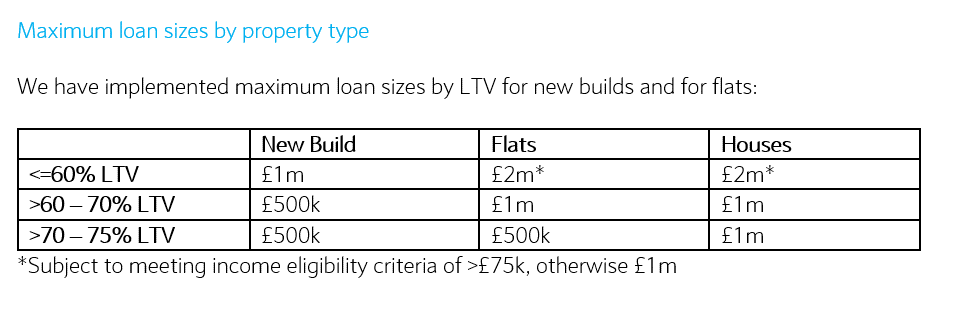

BTL Lending Policy

Please be advised, we’re making some important changes to our Buy to Let (BTL) lending policy that are applicable to any application created within our systems from, Tuesday 29th June.

As a reminder, we consider your client’s individual circumstances in our affordability assessment. The benefit of this is that clients can use their personal disposable income (including surplus rent from other properties) in addition to the rental income from the subject property to pass affordability.

Our overall affordability assessment will remain as a full assessment of income and expenditure, however, we will be introducing some updates to further protect your clients from leveraging their personal income too highly.

Unable to see the image above? please click here to view our maximum loan sizes by property type.

Maximum exposure limits

We have introduced a cap to subject property loan size at 10x your clients gross personal income (excludes existing rental income).

Note – Our existing policy on overall Buy to Let exposure will remain as per the current rules:

- Buy to Let Total Exposure with Barclays to £3m and 6 Buy to Lets

- Overall Buy to Let Total Exposure across all lenders to £4.5m and 10 Buy to Lets

Minimum ICR at a representative pay rate

Some applications may be declined moving forward if the Pay Rate ICR <100%. This will trigger where subject property rental income is not sufficient to cover a representative monthly mortgage payment.

You can use our affordability calculator to check whether your client meets our criteria and the maximum borrowing amount available before submitting a case.

Important proof of deposit changes

From Monday 5 July we’ll no longer accept residential or Buy to Let applications where your client’s mortgage deposit funds originate from the below countries/jurisdictions (this includes gifted deposit applications).

- Afghanistan

- Belarus

- Bosnia & Herzegovina

- Burundi

- Central African Republic

- China

- Cuba

- Democratic Rep. of Congo

- Egypt

- Guinea

- Guinea-Bissau

- Iran

- Iraq

- Lebanon

- Libya

- Mali

- Montenegro

- Myanmar (Burma)

- Nicaragua

- North Korea

- Republic of Serbia

- Russian Federation

- Serbia & Montenegro

- Somalia

- South Sudan

- Sudan

- Syria

- Tunisia

- Turkey

- Ukraine

- Venezuela

- Yemen

- Zaire (Democratic Rep. of Congo)

- Zimbabwe

Other proof of deposit changes

From Monday 5 July the following changes will also take effect:

- We will not accept deposit funds originating from a child’s bank account/trustee account or a foreign business bank account.

- For gifted deposit applications where the funds are received from abroad, there are some additional requirements we may ask for to evidence the deposit including a letter from each donor providing more details.

Pipeline rules

All full mortgage applications (FMAs) already submitted on Introducer Internet by 9pm on Sunday 4 July won’t be affected by these changes. Any FMAs submitted from 6am on Monday 5 July will be assessed using our updated rules.

Capitalise on the surge in second charge borrowing

Second charge lending totalled £91.4m in March, an increase of 31.27% on the previous month[1]. Are you taking advantage of this market trend?

There are many reasons why a second charge mortgage could be a great option for your clients if they are:

- Already on a competitive mortgage rate or have an interest only mortgage

- Tied into their mortgage with heavy redemption penalties

- In need of a larger sum over a longer term to lower the monthly cost

- Wanting to raise capital for a non-traditional purpose

- Unable to obtain a remortgage or further advance

- Looking to raise funds quickly with no upfront fees to pay

- Seeking early settlement flexibility

Mortgage Brain has solutions to help. MortgageBrain Classic and MortgageBrain Anywhere both have second charge sourcing fully integrated, so you can easily source products on their own or compare them side by side with remortgage deals to help find the perfect product for your client.

Whether you decide to use a master broker or go direct to a lender, the filters within our product sourcing platforms cater for both options and make the process quick and easy.

Learn more

Contact us: sales@mortgage-brain.co.uk

New users can register for a free 30-day trial today by

emailing sales@mortgage-brain.co.uk or calling 0208 665 3289

[1] https://www.moneyage.co.uk/second-charge-lending-jumps-31-in-march.php

Take a look at BTL

Welcome to ‘In Focus’ – Hinckley & Rugby for Intermediaries’ new update designed to keep you in-the-know about our latest applications. We will be focussing on mortgages available from our extensive product range, and sharing real-life applications discussed during our daily Mortgage Referrals Committee meetings.

This month we’re putting Buy-to-Let mortgages in focus. Recently named as a top three BTL lender for affordability by Mortgage Broker Tools, Hinckley and Rugby Building Society has an extensive range of BTL mortgages available. Whether your client is a first-time buyer hoping to get onto the housing ladder, a landlord adding a property to their portfolio, or a seasoned borrower who is looking for a new lender, we’re happy to discuss their needs.

Buy-to-Let Non-Owner Occupier Applications Approved:

Clients with Adverse Credit? Call impact packaging

Are you seeing a rise in clients with adverse credit as a result of covid?

We are undoubtedly seeing more cases with varying degrees of adverse credit since the start of the pandemic and it’s clear we are not alone, as demonstrated by our recent partnership with the well-regarded online mortgage broker, Mojo Mortgages. This partnership, which allows them to refer their complex customers to impact, gives us even more insight into what is happening in the wider market and it’s clear that a larger proportion of customers than before have experienced some form of blip in the last 18 months.

The volume of adverse credit cases we are managing has also been recognised by the leading lenders in this space, as we have access to the limited distribution product ranges from Bluestone Mortgages (Sapphire range) and The Mortgage Lender (Lumi range), plus we have great relationships and underwriting support from the likes of Pepper Money, Vida Homeloans and Together.

Are there plenty of options for clients with adverse credit?

We are starting to see lenders create limited distribution product ranges that cater for borrowers with adverse credit, especially those with slightly heavier adverse or more complicated circumstances. These lenders have also recognised the value of providing these to certain packagers, as we have the experience and expertise to help brokers with these clients. The relationship we have with some of the specialist lenders ensures that some will allocate an onsite underwriter to our offices (during normal times) who will purely look at impact’s cases. This ensures certainty of decision and underwrite and in return the lender receives volume, quality business and increased completion conversions.

In addition, due to our investment in technology, we are making it easier for brokers in providing access to over twenty specialist lenders in one place, without the need to rekey data. Our system seamlessly links with market leading sourcing and criteria systems, such as iress and Knowledge Bank, and automatically stores and updates evidence of research as well as any produced KFIs/ESIS. With documents able to be ‘dragged and dropped’ into the system and automated updates via SMS and emails, we believe any specialist packager partner you deal with should make the processing journey as simple and as slick as possible.

What are some of the considerations for brokers when helping clients with adverse credit?

The more thorough and better prepared brokers are from the onset – in terms of asking the right questions to generate relevant and detailed responses from any complex or adverse customer – the less time is spent firefighting issues further down the line, and less stress will be placed on the client, throughout this process. Many online tools are readily available to brokers and customers to check their credit profiles and so these should be utilised early with the customer to ensure you know the full picture before you engage with any lenders and/or packager partners.

European Citizens – how could we help your clients?

We’re making things easier for you by letting you know of some changes we’re making to our policy for EU Citizens from Thursday 1 July 2021.

We want to lend to your clients from the EU who now live in the UK. As a lender, we have a responsibility now that we’ve left the EU to ensure that these clients have the right to live in the UK.

It’s an easy check for us to make. All we need is for you to supply us with the ‘share code’, then we can check their status and proceed to offer as quickly as possible. The code can be obtained from the Government website and we’ll accept pre-settled and settled status.

For those European citizens who arrived in the UK after 31 December 2020, we will assess their Visas as per our normal Visa policy.

What does this mean?

Settled Status

For people with settled status, also known as indefinite leave to remain or enter, there is no time limit on how long they can stay in the UK.

Pre-Settled Status

Those with pre-settled status, also known as limited leave to remain or enter, can stay in the UK for a period of five years. This will allow them to remain in the UK until they are eligible for settled status, generally once they have lived continuously in the UK for five years. They can then apply for settled status.

If you have any questions, please speak to your local BDM.

Got customers with a lower deposit?

Your customers with lower deposits and first time buyers will now have more choice after Leeds Building Society improved its higher LTV mortgage products.

Both their 2 and 5 year fixed rate products come with a free standard valuation and the five year 90% LTV fixed product also comes with fees assisted legal services for standard remortgages.

This product information is for use by FCA authorised intermediaries only and must not be distributed to potential borrowers.

Fee-free June – just got better!

We are delighted to extend this offer throughout July!

June’s offer helped fuel our best ever month, but we know there are a large number of cases in the pipeline so this extension should you with these!

We exist to help mature borrowers aged over 55 and removing the normal £995 to £1,395 product fees is a great way of us giving extra value.

We have no maximum age, take a fresh look at affordability (based on interest only payments), and would love to hear from you on any new enquiries you might have.

Legal & General’s 2021 BQAs

On June 24th 2021, we announced the winners of our 10th Business Quality Awards (BQA). This was our biggest year yet in terms of entries with over 70 submissions for our Outstanding Customer Outcome award- the quality of which were outstanding.

In 2020, the Business Quality Awards 2020 were held just before the pandemic struck. This year, we had big plans to celebrate the 10th anniversary of the awards with our shortlisted candidates and recognise all of the great work you’ve done, particularly in light of the many challenges you’ve faced.

However, while the situation around the pandemic is currently improving, planning ahead has proven tricky during a very uncertain year. Venues are at reduced capacity, and understandably some people may not yet feel comfortable being in a large crowd. So, we decided not to hold a face to face event in 2021, and hopefully return to that format in future

View winners (BQA 2021 Winners & Shortlisted Firms | Legal & General (legalandgeneral.com)

Submit for 2022 and win a BQA

If you’d like to enter our next Business Quality Awards, entries will open in September 2021. Keep your eyes open for our announcement! To help you plan ahead, here’s a handy guide on How to win a BQA.

We know that you have all worked even harder to keep customer focused during the last difficult year. So with this in mind, please share with us the work you’ve done and be in with a chance of winning an Outstanding Customer Outcome Award.

To find out more about these awards, or how the Distribution Quality Management team could help with your business, email: LGIBusinessQualityAwards@landg.com

Virgin Money Greener Mortgages

Our Greener Mortgages are available to customers purchasing a new-build property with an energy efficiency rating of ‘A’ or ‘B’. Our flexible approach means we can accept an Energy Performance Certificate (EPC), a Predicted Energy Assessment (PEA) or a Standard Assessment Procedure (SAP) calculation to evidence the energy rating. Find out more in our Mortgage Update or on our website.

Our service levels at a glance

- Virgin Money’s average application to offer is currently 17 Days. Correct as of 28 June 2021.

Stamp duty holiday deadline

With just a few days to go until the stamp duty holiday is cut back, customers still have the opportunity to make some savings in England and NI, where a reduced rate will still apply up to £250k until 30 September. That feels like a long way off, but we know how quickly time passes in the mortgage world, so make sure your clients are aware of the deadline and that their third parties are working towards the same date.

Give your clients the best chance of completing in time by submitting their fully packaged applications as soon as possible. Remind yourself of what we need with each application by checking our Clydesdale Bank and Virgin Money packaging guides.

Second Charges for Landlords

A common misconception is that second charges are only available for residential clients on residential property.

But this is simply not true, we arrange second charges for professional and accidental landlords on BTL, CBTL and HMO property every day of the week.

Loans can be for any legal purpose but are most often to raise a deposit to buy another property.

- Interest only and capital repayment available

- Affordability based on rental cover, plus top slicing available

- Most credit profiles considered

- No minimum income

- Loans from £20k – £500k

Call our team of experts to chat through any case. If we can help, we’re happy to talk with your client directly.

Call us free on 0800 328 8930

Your June Update: New Products, Videos and Resources

Good morning Robert

Welcome to your monthly Pure update, a curation of business news and resources spanning the last month. As we continue to support you in helping your customers achieve the retirement they deserve with our lifetime mortgage solutions, it’s been a busy month of product launches, events and meeting you back on the road.

Scroll down to catch up.

Product Changes in Focus

Here at Pure Retirement, we’re continually working to provide flexible lifetime mortgage solutions to homeowners in later life. As part of this commitment, we’re pleased to announce new product enhancements across our Sovereign, Heritage and Classic ranges, all of which offer ERC-free partial repayments.

- New ERC-free repayment opportunities and direct debits facility across our

Sovereign Range, giving customers the freedom to manage their plans

in a way that suits their circumstances. - New Heritage Freedom 20 product, offering customers the flexibility to repay up to 20% of their loan each year ERC-free, with up to twelve repayments per year.

- New Classic Flexible Pricing allowing you to lower your client’s lifetime mortgage

rates with personalised quotes that take into account age, loan amount,

property type and postcode.

Learn more about our product solutions

Video Focus

One of the most important things to consider during early conversations with clients is whether they’re actually eligible for a lifetime mortgage. There are many factors to think about when answering this question, from their age to the property value. Our BDM for the South, Jane Forshaw, goes through some of the key questions to ask in our latest FAQ video on our YouTube Channel.

Launch of the Just For You Lifetime Mortgage Fixed Early Repayment Charge (ERC) option

On Wednesday 30th June we launched our Fixed ERC option offering clients a guaranteed cost if they choose to pay off their lifetime mortgage early.

With a choice of Fixed or Variable ERC, you can make your lifetime mortgage solutions even more personalised and recommend the one that suits your clients best.

Community groups to share £100,000 as building society maximises local impact

A NORTH-EAST building society has launched a new strategy to co-ordinate and maximise the benefits it brings to local communities.

Darlington Building Society has unveiled its “community impact strategy” to combine its commitment to donating five per cent of profits to good causes, along with volunteering, financial education, and sharing facilities with local groups.

Despite the economic challenges of the pandemic, the Society will this year donate £60,000 to worthy organisations from the profits generated during 2020.

And County Durham Community Foundation, which administers the five per cent fund on behalf of the Society, has announced it will make an additional donation to bring the total handed out to at least £100,000.

The first tranche of beneficiaries from the 2020 profits have now been announced and they are: Darlington CAP Debt Centre; Butterwick Hospice; South Tees Hospitals Charity; Hartlepool Special Needs Group; Middlesbrough Amateur Swimming Club; Yarm Wellness Centre; Spennymoor Town Band; the Allstars Netball Team, from Hartlepool; and Skelton United Football Club.

Niki Barker, the Society’s Director, People and Culture, said: “Darlington Building Society has been at the heart of the community since it was formed 165 years ago but we want to go further by joining up our key initiatives under one strategy.

“The five per cent pledge is close to our hearts, and we are proud to be able to share £60,000 this year despite the challenges brought by the pandemic. We are also hugely grateful for the support of County Durham Community Foundation and for boosting the fund with a generous further donation.”

Niki added that the financial contribution to good causes is just one of the four key pillars within the new community strategy. By strengthening and supporting as many local causes as possible across each of these, the Society believes it can have a real valuable and sustainable impact across its operating area. The four pillars consist of:

- Sharing profits – through the annual five per cent pledge

- Sharing time – through volunteering and fundraising

- Sharing knowledge – through financial education and career enhancement

- Sharing space – by making facilities available to community groups

The strategy also features a “Local 5” initiative in which the Society’s nine branches will be empowered to work with their members to select five charities and good causes in their local areas to have a more tailored focus on support each year.

“It’s a more focused approach, aimed at creating a sustainable, meaningful relationship with the community by bringing all of these core activities together so that we can maximise the value we bring to the local areas we serve,” added Niki.

In 2020, the Society announced that it was extending its five per cent pledge to 2025 and this year the focus will be on supporting organisations that are making a difference around three main themes: mental health, unemployment, and loneliness.

Margaret Vaughan, Chief Operating Officer for County Durham Community Foundation, said: “It has been wonderful to support Darlington Building Society’s charitable giving through the services of the Foundation.

“Like so many of our fund-holders, Darlington Building Society wants to make a difference when it comes to key issues like quality education, decent work and reducing inequalities. By working together, we can achieve so much more: sharing local knowledge and resources for the good of the community.”

To find out more about how Darlington Building Society supports the community and to apply for a donation go to: www.darlington.co.uk/community/

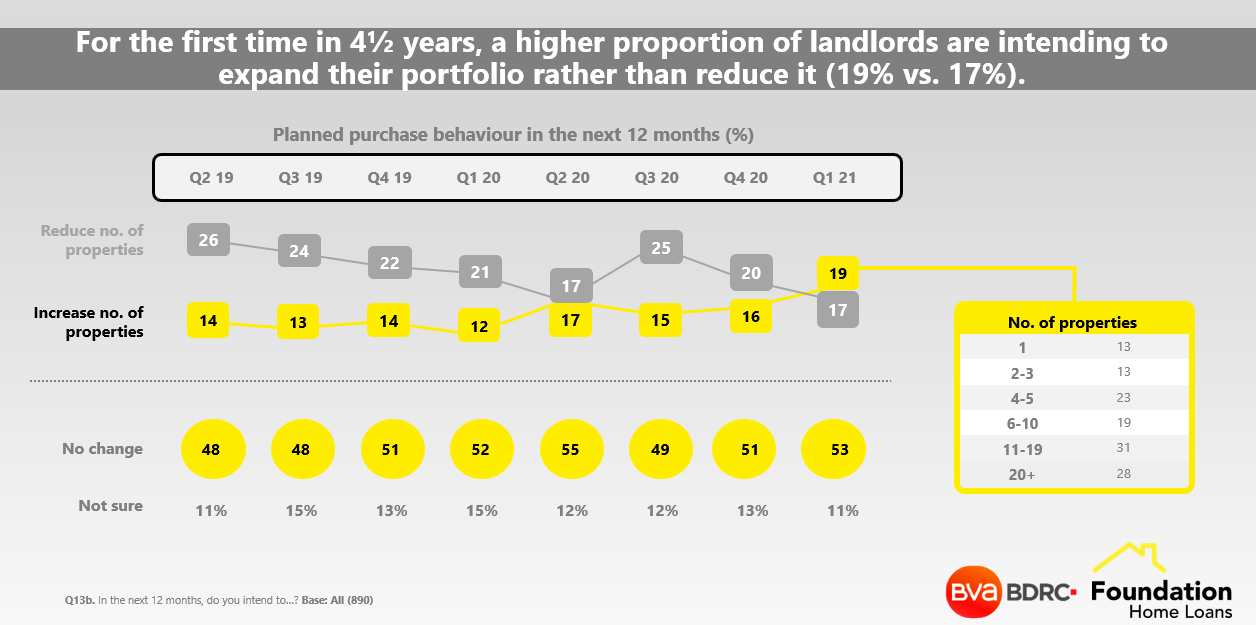

Landlords’ intentions to buy or mortgage in 2021

Like many lenders, we’re currently experiencing a surge in interest from landlords who are looking to diversify their portfolios. This forms part of a wider picture where landlord demand remains strong, and sustained, right across the buy to let sector.

One of the main headlines from our recent quarterly Landlord Panel research in conjunction with BVA BDRC of 895 landlords was that for the first time in four and a half years, a higher proportion of landlords are intending to expand their portfolio rather than reduce it (19% vs. 17%).

Within this, landlords with 11-19 properties were said to be the most likely to be looking to grow in the next year, following a 9%pts increase versus the Q4 ’20 data. In addition, landlords operating in the North East and Wales were highlighted as ‘most likely’ to be active in the BTL property market in the next year, with around half looking to either buy or sell.

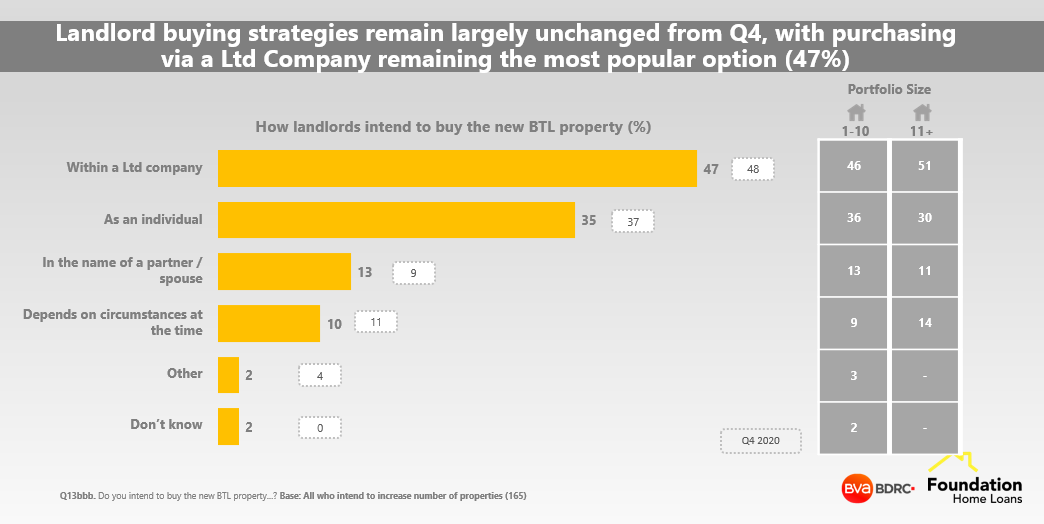

Unsurprisingly, the landlords look to maximise profits where possible, by increasing the income side with higher yielding properties, and reducing expenditure with lower cost mortgage solutions, which is why we recently introduced some fee-assisted options for BTL purchases as well as remortgages.

Whilst the majority of landlords rent their property as an individual (80%), 18% of landlords currently hold at least one of their properties within a limited company structure but of those Landlords intending to buy this year, 47% reported that they intend to buy their next property via a limited company, a sentiment largely unchanged from Q4 2020, and which we expect to continue to be on of the fastest growing areas of advice requirement in the coming years.

Purchasing strategies remain relatively similar regardless of portfolio size, with 11+ property landlords only slightly more likely than their smaller counterparts to intend to buy within a Ltd company structure (51% vs. 46%).

If you’re a mortgage intermediary, and you’d like to continue to be among the first to receive the latest data on landlord intentions and buy to let market trends, click here to register.

TMA UPCOMING EVENTS

Protection HiiT Series

20th July

21st September

Virtual Workshop

Tuesday 6th July

Virtual Workshop

Thursday 15th July

CLICK HERE

QUERY OF THE WEEK

Q – Who will lend on a property with a retrospective warranty?

Please give our broker support desk a call on 0330 303 0236 for more information.