Stamp Duty reduction changes 30 June 2021

The Stamp Duty reduction is due to change on 1 July 2021. It’s important you’re aware of the following information:

- The latest date for legal completion to qualify for the current Stamp Duty reduction is 30 June 2021

- If the purchase does not reach legal completion on or before 30 June 2021 Stamp Duty will be payable where applicable

The Conveyancer will be able to advise on the progress of the purchase transaction and will be aware of what action is required to progress the transaction

The above message has been communicated as a reminder of the deadline on stamp duty and we require your help to ensure that any potential impacts to our customers can be minimised. We would suggest if a new application is progressed at this late stage with expected completion on or before the 30 June 2021 that you ensure that the customer enters into the purchase aware of the implications of not being able to meet the above deadline.

Say hello to greener Mortgages

Virgin Money is passionate about building a brighter future for us all, and are working hard to deliver products and services that make a positive impact on society and the environment.

They’ve just launched a new range of Greener Mortgages; rewarding customers for purchasing energy-efficient new build homes.

Through their Greener Mortgages, customers benefit from a range of new build products that are priced 0.10% lower than the equivalent core products. They have 2 and 5 year fixed rates at a range of LTV options, also available for Help to Buy Equity Loans.

Customers must be purchasing a new build residential home with a certified or predicted energy rating of A or B. This will be evidenced by an Energy Performance Certificate (EPC), a Predicted Energy Assessment (PEA) or a Standard Assessment Procedure (SAP) calculation.

Their New Build lending criteria applies. For information on Virgin Money’s requirements and eligibility, visit their Lending Criteria.

A brighter future

Virgin Money have partnered up with Carbon Neutral Britain and for every Greener Mortgage that completes, they will fund environmental projects, such as the development of wind, solar and hydro renewable energy. The funding will offset the equivalent of the average UK home’s carbon emissions for an entire year*.

Together with Carbon Neutral Britain, they’re also aiming to plant 100,000 trees from the sale of their Greener Mortgages.

To find out more, visit their website, talk to your dedicated Business Development Manager or contact your Regional Service Team.

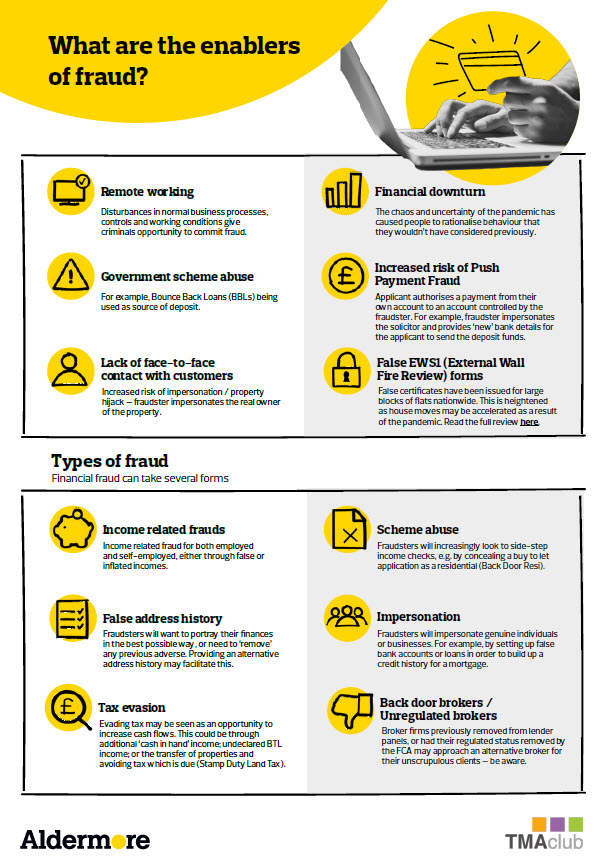

How to Identify and defend against financial crime…

Covid-19 has presented a challenge for all businesses, industries, and individuals. A huge concern throughout the pandemic has been the proliferation of financial crime and the opportunities that have presented themselves to fraudsters. The risk and instances of financial fraud have increased substantially.

Changing how they accept portability and additional lending

Accord are streamlining their processes to provide a more efficient service for brokers and their clients. The new process will automate the transfer of application data into their systems and remove the need for paper, meaning it’s better for the environment by reducing their carbon footprint.

Here’s what brokers need to know:

- From Tuesday 1st June Accord will no longer accept handwritten or postal portability and additional lending application forms

- Application forms must be completed digitally with all questions completed

- The forms must have a digital signature and be correctly uploaded as a pdf

- They can only automate the process if these steps are followed

- Handwritten or forms that have been scanned cannot be automated

- They’ll be asking for any forms not completed correctly to be resubmitted in the correct format.

They have some handy ‘how to’ guides on the lenders website. Click here for porting or here for additional lending guides.

They’ve also set up an email address for any brokers needing support before they submit a portability or additional lending application. Accord_sales@accordmortgages.com

The complexities of cladding

Cladding is a complex issue, which is often misunderstood within the mortgage industry. Our BDM Jonathan Evans wants to change that. After experiencing a growing number of enquiries, he educated himself on the latest cladding regulations and is now on a mission to support the rest of the intermediary community by providing information and insight on the topic.

Read Jonathan’s latest article on cladding.

New RICS guidance

At Skipton Building Society for Intermediaries we’ve already adopted the new guidance that was issued by the RICS in March this year, including the new EWS1 form. The guidance should result in fewer unnecessary requests and is different in a few key areas. It’s another way we’re Making Things Easier for You. Visit the RICS website for details.

What does the market tell us for Q2?

With Q1 2021 now behind us, it seems like a good time to take stock of what has happened during those first three months, and what the rest of the year might bring, particularly as we move out of this latest lockdown. The forecasts for the year ahead certainly look very different today when compared to early January, with the Budget announcement in March representing something of a catalyst for a more positive outlook for this year.

First time landlords looking for a BTL lender? Look no further

We welcome business from first time landlords for Standard product applications. With our competitive and broad range of products and criteria, you can be sure to find something for your first-time landlord clients. Here’s a snapshot of our requirements:

- At least one applicant must have owned and still own at least one property (residential or buy to let) for a minimum of 12 months.

- Employed – must be in permanent position for at least 6 months and not under notice of termination.

- Self Employed & Contractors – One full year’s evidence of income from accounts or accountants

certificate or SA302 together with a tax-year overview.

Take a look at our Application Submission Guide here for more information

Stay in-the-know

In these changing times, it’s important to find the most up-to-date information available for your BTL clients; and we’ll continue to bring you regular updates to help you to provide answers to any complex questions you and your clients have.

Get in touch with our BTL experts , call 0370 707 1894

(Mon-Fri, 9am until 5pm)

Launches larger loan cashback

Keystone Property Finance have launched a new Larger Loan cashback offer and have dropped their rates.

Not only have their core product rates dropped, but Keystone’s new Green Product mortgage range which launched in March, has dropped too – 10 basis points lower than their core products. The Green Mortgage Range offers discounted rates to landlords whose properties have an EPC rating of A-C.

Alongside the drop in rates, Keystone have launched a new cashback offer on loans of £200k and above. Landlords will receive £750 cashback on loans between £200k- £500k, and £1,000 cashback on loans £500,001 – £1m on completion of their case.

Keystone Property Finance hope that their reduced rates and cashback incentive will benefit landlords after a difficult 14 months since the pandemic started.

Visit www.keystonepropertyfinance.co.uk to view their new product range or call their broker hotline for more information: 0345 148 9086.

Care in every claim

With 98% of all protection claims paid out in 2020, our strong track record shows we’re there for you and your clients when they need it most.

Remodelling when two become one

Case agreed: short term mortgage to remodel two separate flats into one high-end home.

The facts at a glance:

- 4 bedroom detached London home

- Property split into two flats by vendor

- Borrowers planning to return to a single home through interior remodelling and move in

- 80% LTV of £1.575m purchase price

- Part repayment/ part interest only ERC free short term mortgage

Smaller loans & Portfolio Multi-loan

TML are continually looking at ways to enhance our proposition and also support landlords that are looking to grow their portfolio’s.

As well as having a proposition for larger loans above £500,000 we also have a smaller loans option, great for those lower value properties with high rental yields.

Smaller loans product:

- Min loan of £50,000 (max £200,000 on smaller loans)

- £0 completion fee

- Available for individuals and Ltd Co’s

Portfolio multi-loan product:

- Min loan of £50,000

- Multiple applications within a 6 month period to be submitted with no additional application fees

- Reduced completion fee of 1.25%

- Available for individuals and Ltd Co’s

- £0 application fee for subsequent applications submitted within 6 months (3 months for non-portfolio landlords)

For more information give our sales hub a call on 0344 257 0418.

From case manager to underwriter:

Buy-to-Let deals with Jess Kayli

Jess Kayli talks about her time moving through the case management and underwriter teams at LendInvest.

Take a closer look at our up-to-date Buy-to-Let deals and rates.

I joined LendInvest as a Buy-to-Let case manager in 2018. This was a position I held for a year and a half before I was asked to join the underwriting team as a trainee underwriter.

This was an exciting opportunity for me. I wanted to progress in my career but also further my Buy-to-Let knowledge. Prior to joining LendInvest I had worked exclusively in unsecured lending, so Buy-to-Let underwriting was the next step on what had been a big learning curve for me from the very beginning.

Right away though I knew I would be in good hands, as case managers we had always worked closely with the underwriting team and I knew they would be able to support me as I started the new role.

Having that close relationship was a good thing because at the start a lot of my training was sitting with them, watching what they did, asking questions and learning the process before I started taking on my cases.

At first when I took on cases I worked closely with members of the team who would oversee my work and review it with me. Over time I began taking cases through to preparing for an offer, where it would then be signed off and offered to the clients.

Being adaptable

Part of making this step work has been adapting my perspective when approaching deals.

With more responsibility over the progress of the case, the knowledge of our criteria and how the process works becomes more important as it is important for me to have the confidence to make decisions myself rather than referring quirky deals to others.

This is where I feel my background in case management has been really helpful to being a good underwriter, because during my time overseeing those cases I’ve seen every type of deal come through and observed closely how our underwriting team manages it. This has been a valuable experience to bring to my cases.

That knowledge and experience is what I think helps create a good underwriting experience, as well as developing close working relationships with brokers which we do more and more with every deal we complete.

For all the technology we use to make our jobs easier and the deal faster, that relationship is what helps deals move smoothly, and its what I see with well-packaged deals when a broker has provided us with the basic documents and clear information around the deal which goes on to make our experience so much easier.

We all want to get brokers and their clients the right deal at the right time, and it is building those partnerships which makes that happen.

Take a closer look at our up-to-date Buy-to-Let deals and rates.