Our mortgage application process just got even easier

At LiveMore we’re on a mission to make borrowing more accessible for mature lenders – and that includes constantly striving to make our administrative processes hassle-free. Our online mortgage application process was always pretty quick and simple but now we’ve added some extra features to help you complete it with even greater ease

Easier navigation. You can see at a glance the various different stages and what information you’ll need to provide

Smooth scrolling. Just a single page making it easy to move from one stage to the next

Progress tracker. The navigation sidebar shows you exactly where you are in the process – what sections you’ve completed and which still need information.

Save option. This allows you to pause at any point if you get interrupted or need to gather more information. You can pick up where you left off without having to start again.

Error alert. This will highlight any sections with missing information you still need to provide.

These changes have been prompted by feedback and data we’ve gathered over recent months. We’ll continue to do this and will be constantly upgrading our tools to give you and your clients the best experience possible.

In the meantime we look forward to working alongside you to help your clients live life to the full – with the least possible fuss and bother!

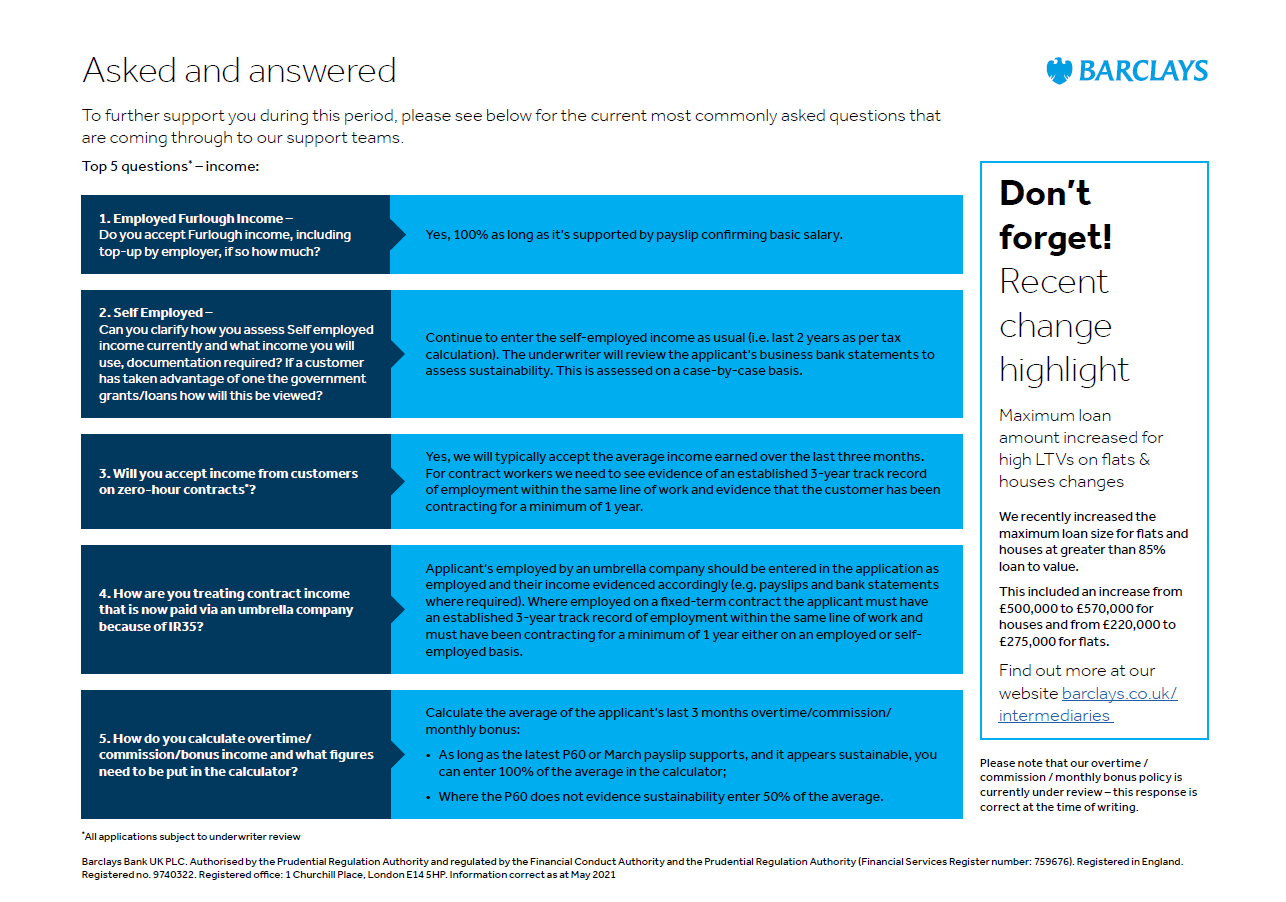

Barclays Ask and Answered

To further support you during this busy period, Barclays have produced a bite sized guide that answers the top 5 current most commonly asked questions that are coming through to their support teams.

For answers to questions such as do Barclays accept Furlough income, including top-up by employer or for clarity on how they assess Self employed income, please view the attached.

Barclays Green Mortgages

In April, Barclays launched their innovative Green Home Mortgage range that rewards customers who are buying an energy-efficient new-build home directly from a builder or developer. Available on all eligible new-build properties, the lender offers them a lower rate on certain fixed-rate mortgages compared with the equivalent option from their standard range, as well as some exclusive Green products (subject to lending criteria)

Support in six ways for your limited company cases

With the potential access to larger loans, and benefits for higher-rate tax payers, limited company loans may seem like an appealing prospect for landlords – especially those that are looking to diversify and expand their property portfolios.

At Kent Reliance for Intermediaries, not only do we offer the same rates for limited companies as private buy to let landlords, but our dedicated panel of approved solicitors can provide both sole and dual representation on your client’s cases should it be required. We can also now accept intercompany loans.

But what exactly can we offer? How can our broader limited company criteria support your cases?

Here are the six reasons why you should consider choosing Kent Reliance for Intermediaries for your next limited company case.

1. Up to four directors accepted

Not only do we accept up to four directors per application, but other companies can also be considered as shareholders– the purpose of this being to allow money to move within the group. These companies can be holding or trading business.

2. No strict SIC code requirements

Life after lockdown: The future of UK homeownership

As a follow-up to our 2019 first time buyer study, our new mortgage study Life after lockdown: The future of UK homeownership analyses research among 12,000 UK adults on how the pandemic has changed our attitudes to homeownership, how the financial impact of Covid-19 has frozen many first time buyers out of the homeownership dream and makes policy suggestions designed to make sure that first time buyers are not left behind.

Key findings

- The homeownership dream remains strong with nearly two-thirds (63%) saying it is now more important than it was pre-pandemic.

- The proportion of first time buyers who say raising a deposit is the biggest barrier to homeownership has risen from 30% in 2019 to 52% in 2021.

- Other challenges to buying include falling incomes, pressures on the Bank of Mum and Dad and house price rises across the country.

How we’re supporting first time buyers

- 5% deposit mortgages available through the Government’s mortgage guarantee scheme

- Product benefits including a free standard valuation on properties valued up to £2.5m, no product fees and cashback on selected mortgages. (Early repayment charges may apply).

Empowering brokers to help more customers…

“Knowledge is power. So, in 2019, Pepper Money decided to embark on an ambitious research programme to create and share knowledge about the attitudes and behaviour of customers with adverse credit. The in-depth study shone a light on this important group, challenged preconceptions and presented new opportunities for advisers to help a wider range of customers.

We have continued to run the regular survey throughout the COVID-19 pandemic, and the results have painted a clear picture of a divided nation. Whereas some people have been able to maintain or even strengthen their financial position, others have struggled, with reduced income and increased debt.

As we start to look beyond the pandemic, it’s vital as an industry, we ensure that these people do not continue to suffer a financial hangover of the virus through exclusion from everyday financial products and services.”

Laurence Morey, Pepper Money CEO

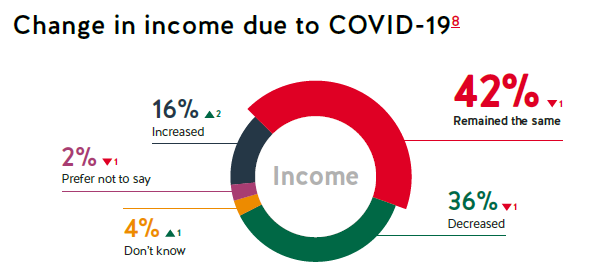

People with adverse credit have been hardest hit financially by COVID-19

Reduced income

36% of people with adverse credit say their income has decreased in the last year, compared to 24% of the general population.

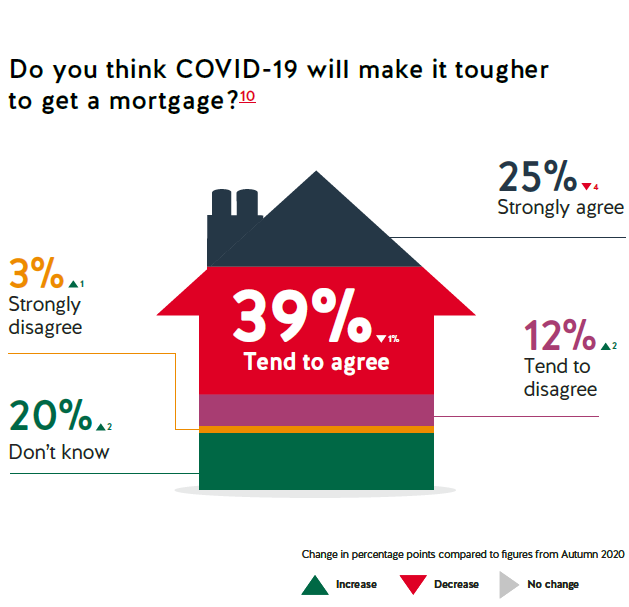

Mortgage prospects

65% of people with adverse credit think it will be harder to get a mortgage as a result of COVID-19, compared to 55% of the general population.

Key findings from this wave of research

• 6.29m adults in the UK have experienced adverse credit within the past 3 years. This number is actually down from 6.81 million 12 months ago.

• And of these, more than 880,000 intend to purchase a property to either live in or let out in the next 12 months

• 52% of adults with adverse credit who are planning to purchase a property in the next 12 months are concerned about their mortgage application being declined due to their credit history.

• However, only 44% of respondents with adverse credit who are looking to buy a property said they would go to a mortgage broker. This is down from 66% last autumn.

Service Level Update

Please note our application processing timescales have increased. To help prevent any further delays please ensure all supporting documentation is included on submission of your application.

Please visit our broker website www.themeltonbrokers.co.uk to view our current service levels.

We apologise for any inconvenience this may cause. If you have any queries please call our Broker Support Team on 01664 414144.

Accord 90 day offer extension beyond 30th June Stamp Duty Deadline

Applies to Residential and Buy to Let purchases and re-mortgages.

Accord are pleased to let you know that they have extended the timeline they originally had in place for the additional 90 day offer extension to reduce pressure across the clients’ mortgage journey.

What do you need to know?

Accord can look to extend existing mortgage offers expiring no later than the 31st October 2021 for a further 90 days, subject to a case review being completed.

The application needs to be near the expiry date of the original offer before we will start the process (i.e. within a month), which will include:

- Confirmation from the valuer regarding the previous valuation figure still applying

- Up to date evidence of income and bank statements and credit score

- Confirmation there are no material changes to the application

previously had an offer extension, no further extensions will be accepted.

What else has changed?

Grace Period

Accord have reintroduced the 10 working day grace period where the solicitor confirms they can complete within the 10 additional working days after the offer has expired.

Stamp Duty changes

Some brokers have been in touch about Accord’s policy for clients who will have their stamp duty paid as part of their deal with the developer if they miss the 30th June deadline.

Accord will accept stamp duty paid incentives, and will not include these when assessing against their incentives policy, on all applications which exchanged on or before 30th June as long as the solicitor confirms this in writing. Accord do not need an updated UK Finance Disclosure Form (formerly known as Disclosure of Incentives Form).

For applications which exchange after 30th June, any changes to the incentives must be confirmed using a UK Finance Disclosure Form. The changes must meet Accords new build incentives policy.

Care in every claim

The latest vodcast from our Expert Series explains how the claims process has improved in the past year providing emotional and practical support to your clients throughout the claim process.

Watch now

Tips, tools and your questions answered

Save your space at our third summer webinar where host Rachael Hunnisett will be joined by our in-house experts Claire Davey and Hayley McGee. This is your chance to ask about the tips and tools we offer to make things easier for you and your clients, so bring your questions!

Webinar details

Your most asked questions (and answers) and how you could get more from Skipton’s service.

Thursday 1 July at 9.30 – 10am.

With guest speakers from Skipton Building Society Claire Davey, Head of Direct Distribution and Hayley McGee, Senior Service Manager for Mortgages.

About Claire

As Head of Direct Distribution, Claire’s responsible for our broker and customer-facing phone, web chat and social media teams and looks after the operational side of our mortgages and savings divisions. She’s been with Skipton for 25 years.

About Hayley

Hayley leads our call-taking team, which supports brokers and customers, in her role as Senior Service Manager for Mortgages. She’s been at Skipton for 13 years, including eight in the contact centre.

See the full list of summer webinars at Skipton Talks – a hub for webinars, blogs and insight for the intermediary community.

‘Typical’ portfolios and the rise of younger landlords

As a lender, we are always striving to assess landlord profiles, what they are looking for from a lender, what a ‘typical’ portfolio might look like and how various landlords are reacting to current market conditions. This is also incredibly useful information for intermediaries.

According to our latest research in conjunction with BVA BDRC for Q1 2021:

- A typical portfolio was worth around £1.2 million and generated an annual gross rental income of £54,000.

- It had 7.3 properties, down from 7.7 at the end of 2020.

- Based on an average Q1 portfolio size of 7.3 properties, the typical property value was £168,000 generating an annual income of around £7,397 per property, or £616 per calendar month.

Insight from Knight Knox suggested that the average age of British landlords has decreased, with 47% now aged under 40. The report went on to suggest that landlords are getting younger — and they’re making more money from rental income than their older counterparts. The average income per year was said to be highest for the very youngest landlords, with those aged between 18 and 30 generating an average £25,481 a year.

Read more of our latest research about what a typical portfolio looks like

This research also found that younger landlords are also more optimistic about the future. 54% of under 30s surveyed were ‘very confident’ about the market predictions for the next 12 months — compared to 15% of over 51s who said the same. 47% of under 30s plan to buy another house within the next year. However, while landlords are getting younger, the number of homes landlords own on average has dropped slightly, from 2.5 to 2.1.

It’s great to see the spotlight being shone on the younger end of landlord spectrum and its highly encouraging to see confidence levels rising and plans in place to purchase more properties. This helps to further demonstrate that the future of the BTL market continues to shine bright and is in safe hands.

Why choose Zephyr?

There are so many reasons why you should consider Zephyr for your specialist BTL cases, along with our great service we have Specialist BTL experts on-hand to answer all your queries. Here’s just some of the highlights of what we offer:

- Standard & Specialist properties, including HMOs, MUFBs

- FACs & New Builds Individuals & Limited Companies

- Single properties & portfolios

- Personal & Portfolio income backed

- Top Slicing considered, subject to criteria

- 2 & 5 year Fixed rates up to 75% LTV

- Max loans to £2m (on our 65% LTV Standard product)

- No upfront application fees*

Q is for Quick answers

Just get in touch for any help and support you need, whether it’s a quick query on a case submission or a more complex question – they’re always happy to help.

Or call us on 0370 707 1894

Higher Earners can get up to 6x salary

For clients with evidenced income of £200k plus we will consider loans of up to SIX times income, up to 80% LTV (Interest only max 70% LTV) – speak to your BDM to find out more. Don’t forget: we can accept 75% of bonus income. Short term ERC free mortgages available.

Have you got high earning clients who need higher LTI borrowing? Contact your TFI BDM today:

Call 0800 378 669

HOW WE’VE ALREADY SUPPORTED HIGHER LTI BORROWING

Our client needed a short term mortgage to buy a new £1.2m London flat, breaking the property chain by waiting to sell their £800k former home at a later date.

With substantial employment income from a long term position we were able to agree two short term ERC free mortgages jointly worth 6 times income, enabling a chain free purchase, stress free move and unrushed sale.

Ralph Punter, BDM at TFI said:

“For clients with high evidenced income we’re able to lend higher LTI multiples to help them buy their dream property. We’ve already helped clients in this situation and are ready to help more.“

Let us help you retain your clients

Our Existing Business Agent Hub (EBAH) in OLPC keeps advisers informed when their clients miss payments or ask to cancel their policy. By quickly receiving this information advisers have the opportunity to get in touch with them, understand from them the reasons behind the missed payment, remind them of the importance of the cover they have – and discuss any potential changes in their circumstances and reassure your clients.

How it’s helped

In 2020 these real time notifications on EBAH have helped advisers in retaining 40,643 policies and £14,821,874 in commission. The agent hub will continue to help support your business in 2021, so your advisers can continue to help your clients in these uncertain times during the Pandemic, a time when clients may be experiencing a variety of difficulties.

Key System Updates

- 8 ways we’re making it easier to do business – view our quick guide to see how we’ve streamlined our application process – from beginning a policy to amending one.

- Live chat is available to quickly answer your questions during office hours.

- Our Legal & General Virtual assistant is available 24/7 and provides instant responses. Receiving over 20,000 questions a month it’s currently able to resolve 96% of all queries, for a quick and straightforward service.

Buy-to-Let? It’s our thing!

Are you still struggling with clients who cannot seem to get a buy-to-let mortgage on the high street? Or maybe they are trying to buy a HMO that has too many bedrooms? Whatever the reason, we can help.

We can help secure funding for a wide range of scenarios and deliver a tailored solution and are very experienced in dealing with complicated or unusual cases.

Our clients return to us because of what we offer:

- Direct access to decision-makers.

- Speed of service.

- Up to 80% LTV.

- All property types considered – residential, semi-commercial and commercial.

- First-time buyers and First-time landlords.

- NO maximum number of properties in the background.

- We can lend to ex-pats of foreign nationals.

- More lenient stress testing 100% of the pay rate.

- We can lend to all corporate structures Ltd Co, Off-Shore entities.

- Holiday lets.

- Houses of multiple occupancy.

- Student lets.

- No minimum incomes required.

- Portfolio landlords welcome with lenient outside Portfolio stress testing.

- Heavy adverse credit profiles considered.

For any questions, enquiries or pressing cases you would like to talk through, I’ll be happy to help. Please reply to this email or give me a call on 07841 026375.

Watch: How Open Banking simplifies Buy-to-Let mortgages

See all of our latest Buy-to-Let rates and offers here

Using Open Banking to increase the speed to offer for Buy-to-Let mortgages is a relatively new approach some lenders take, but one we’ve talked about for a long time.

As a technology-enabled lender, we’ve long seen the potential benefits of how we could use Open Banking to speed up underwriting, cut down on paperwork for brokers and their clients and ultimately deliver the right deal, faster.

We also understand, however, that with new tech comes cautiousness. This has been true of Open Banking, where brokers have shared concerns with us about security, and how the access it grants can be used to reject more deals.

Recently our Chief Operating Officer, Arman Tahmassebi, presented to brokers how our Open Banking process works, how it simplifies the Buy-to-Let process and went behind the scenes of how our Open Banking provider, Credit Kudos, operates.

You can watch the full video here:

Bridging: Short Term Lending via impact packaging

Bridging can be arranged by Impact Specialist Finance on a regular or nonregular basis. The risk can spread over more than one property to ensure the cheapest rate is applicable and can help to reduce the deposit required.

Advantages of Bridging with impact:

- We have a dedicated bridging team with decades of experience ready to help

- Strong close relationships with many of the leading bridging lenders

- Bridging lenders are generally geared up to complete applications faster than mainstream lenders in 3-4 weeks

- Proposed monthly payments can be added to the loan so they don’t needs to be made monthly

- Lenders may be more flexible about the property condition – good for refurbishments

- If buying at auction the loan can be agreed upon before you buy

- Credit issues considered on an individual basis

Call Impact today on 01403272625.

TMA UPCOMING EVENTS

Protection HiiT Series

30th June

20th July

21st September

Virtual Workshop

Tuesday 6th July

Virtual Workshop

Thursday 15th July

CLICK HERE

QUERY OF THE WEEK

Do you have a complex case? Take a look at our query of the week to find out how TMA supported a broker with a niche case:

Q -Consumer BTL remortgage

The client had already moved into a residential flat, the existing property had been rented out for less than 6 months and was a flat in the same block as the residential. There were 3 flats in the block, making the clients exposure 66.66%, with share of freehold. The case also required Top Slicing.

A – In this instance TMA have multiple lenders on the panel that are able to look at this scenario exactly.

Please give our broker support desk a call on 0330 303 0236 for more information.