WEBINARS ON DEMAND:

ROYAL LONDON

Business Health Check

LEEDS BUILDING SOCIETY

Shared Ownership

ROYAL LONDON

Business Protection

LATEST PARTNER BLOGS:

KRFI

Self-Employed client trying to find a resi?

AMI

Inclusion in the world of mortgages

PRECISE MORTGAGES

Forewarned is forearmed

UPCOMING EVENTS REGISTER HERE

TMA CONFERENCE

10th November

PROTECTION HIIT SESSION

17th November

VIRTUAL WORKSHOP

23rd November

Newcastle Building Society

Launch into the Shared Ownership Market

Newcastle Intermediaries are delighted to announce we will be entering the Shared Ownership Market from today Friday 18th November with a range of exclusive shared Ownership products to support the launch.

Click here to visit their website page for more updates. Below are some of the key highlights;

- Shared Ownership properties are offered by Housing Associations or registered Social Landlords who will act as the landlord

- We will only consider lending under this scheme in England only

- For new build applications, standard new build property criteria will apply, this includes:

- 9 month mortgage offer period

- Non-cash incentives accepted

- Acceptable warranties are available on our website

- Please note cash incentives are not acceptable with shared ownership

- Maximum household income level is less than £80,000 outside of London and less than £90,000 in London

- Available for purchase only

- Maximum loan amount is 95% LTV of the borrower’s share on both Houses and Flats

- The borrower must contribute at least 5% deposit, this can be from their own funds or as a family gifted deposit

- The rental payment and any ground rent & service charges will be included in the affordability assessment

- Maximum exposure limit of 25% per site

- Borrowers must reside in the UK and must not have any interest in another property

- Minimum share of the property to be purchased is 25% LTV

- Maximum share of the property to be purchased is 75% LTV

- Property must be leasehold & must follow the standard model lease agreement post 2010.

- Loan must be on a repayment basis

- Standard ‘resale’ properties, policy states 85 years required to be on the lease at completion

- New Build properties, we require 125 years on flats and 250 years on houses

The Mortgage Lender

How EPC ratings will impact the BTL market

Amid rising base rates and rocketing energy costs, landlords are now facing an extra potential headache – stricter EPC targets that will hit the rental sector hard. It could impact your BTL business, so you should be prepared.

Under proposed new rules, there’ll be a higher minimum rating required for all newly rented houses and flats from 2025. For many landlords, that could mean spending thousands on double glazing, insulation, and new boilers. As a result, many will consider selling older properties, while brand new homes will become more attractive for BTL business.

Our new article covers details including;

- What the new targets mean

- Exemptions, and who is likely to be eligible

- Potential portfolio unloading

- How landlords are snapping up new-builds

Understanding the legislation will give you a great reason to contact and talk to your BTL clients. And it will help you get ready for the inevitable changes in the market.

Legal & General

Deadline to Breadline 2022

Our research explores the financial resilience of working households across the UK.

Many households are overestimating their ability to survive with no income and are far less financially resilient than they think. Find out the impact for your clients.

Pure Retirement

Launch ‘MyPure’ management platform

Pure Retirement is proud to launch MyPure, the new way for customers to manage their lifetime mortgage accounts online via their smartphone, tablet or PC.

In an equity release industry first, customers are able to make one-off repayments, apply for a cash release, easily view their account balance and more, giving them, on demand access to their accounts.

By providing them with greater account accessibility, customers can now, in a paperless manner, view their recent transaction history, download their annual statements and complete and submit their annual Certificate of Continued Occupancy online for the first time.

The new platform also makes it easier for customers to get in touch with our team, while also giving them access to a bank of FAQs and useful documents.

We’ve listened to customer and adviser feedback, giving customers the power to access their accounts on the go.

LiveMore Capital

The latest issue of Fuel for Life

The latest issue of Fuel for Life from LV= is out now, a digi-zine created to support advisers with all things protection. This issue is packed with expert views, tips and proof points to get you positioning protection with your clients. Features include:

- What’s new from LV=: An overview of recent updates from LV=.

- Ask the experts: Hear from Emma Thomson (Sesame Bankhall Group) on her focuses between now and into 2023.

- Income Protection insights: Some key findings from recent consumer research ran by LV= to enhance your protection conversations.

- Protection Pays: Some recent Critical Illness claims for LV= and case studies to demonstrate the value of protection.

- Use value-added services in your retention strategy: Highlight the value in everyday benefits.

Gatehouse Bank

New BTL and Home Purchase Plan range

From Tuesday, 15 November 2022, Gatehouse Bank launched a new range of BTL and Home Purchase Plans. In addition, they also made some changes to the application criteria, details of which will be provided in the launch communication.

Improvements and Changes to our Application Process

Following feedback from our intermediary partners, over the past 6 months we have completely reviewed our application process, with a view to improving both the speed and quality of the Broker and Customer journey. As a result, we are delighted to share below the details of the key enhancements and changes that have been made in the following areas and will be effective from 15 November:

- Simplified requirements for supporting documentation

- Underwriting Team structure

- New case discussion call

- Case updates

- New early valuation option

- Validity periods for new business applications

- Enhancement to Credit Check process

- Vulnerable customers

- Country checklist updated

- Declined application process

Foundation Home Loans

Helping landlords to achieve strong yields and capitalise on growing tenant demand

A huge number of factors continue to weigh heavily in the thinking of both potential and existing landlords, no matter how large or small their expectations or portfolios. The significance placed on location has always been evident across the residential and buy-to-let markets and regional variations can have a huge impact on house prices, yield and tenant demand.

Mansfield BS

Versatility case study – accommodating an existing Debt Management Plan

Here’s a recent example of house purchase by a couple, where one of the applicants was in an established Debt Management Plan (DMP) as a result of a marital split:

- Loan amount £235,500 at 74% LTV

- Term – 34 years with the oldest applicant aged 36

- Applicant still remained on the former marital home mortgage

- The applicant plans to sell off the former marital home and repay all debts on the DMP

Any adverse criteria must be linked to a single life event with a full acceptable explanation. If an application contains criteria in more than one Versatility category, underwriter discretion will apply. All applications are subject to individual assessment and underwriting.

Our full range of Versatility products is available online via our intermediary mortgages page. Take a look at our criteria guide to see what we can do for your clients.

A common sense approach

If you’ve got a case on your desk that requires a common sense approach to lending then please pick up the phone to our Broker Support team on 01623 676360 or visit https://www.mansfieldbs.co.uk/intermediaries/

Inform Specialist Finance

Introducing Market Financial Solutions to the impact panel!

Impact Packaging has welcomed MFS (Market Financial Solutions) to the panel, the lender considers all complex and real-life situations, where typically the whole process is in a lengthy hurdle and offers products ranging from Buy to Let to Bridging.

Buy to Let Highlights:

- Max loan on single asset £3M, max loan on portfolio lend £10M

- No stress-testing on background portfolios

- Foreign Nationals & Expats (no credit footprint needed)

- Combine multiple complex customer situations, corporate structure, and locations with a wide variety of strong yielding property types

- Can combine with offshore companies, individuals, trusts, along with impaired credit up to and including discharged bankruptcies

Bridging Highlights:

- Will lend to any foreign national if they do not reside in a sanctioned country

- Max 75% LTV on 1st Charge, 70% on 2nd Charge

- Large Loans of £50M+

- Terms up to 24 months

- Will lend to applicants with unlimited adverse credit/negative media articles

Download MFS latest product guides

Take a closer look at MFS Buy to Let and Bridging product ranges to help find a solution for your client cases.

Have a case you would like to discuss? Call the impact packaging team now on 01403 272625

Skipton Building Society

It’s easier to check site exposure

You can now easily check which postcode areas have reached our new build exposure limit. We have created a list of these areas, which you can access whenever you need through our new build webpage.

New Build Postcode Exposure Limits.

Need additional new build support?

If you have any questions, or need further help, you can visit our new build support webpage. Here you will find useful information including our proposition and contact details for our dedicated help desk.

Vida Homeloans

Mortgage pricing in the new environment

It is not often that mortgages make the top read stories on the likes of the BBC website. Nor does it often occur that mortgages are the topic of so many conversations. But that is what has happened of late, since we saw rapid repricing in recent weeks.

However, with such widespread news coverage of mortgage rates, the technical aspects of pricing products have led to a degree of confusion. Some people have become confused as to why mortgage rates rose so sharply – more than the increase in the Bank Base Rate. Some people even believe mortgage lenders are just “profiteering” as the gap between the Bank Base Rate and general mortgage rates widens.

This does, however, give mortgage brokers a real opportunity to really demonstrate their credibility, a key element of the trust equation, by providing content to clients about the pricing of mortgage products.

The Loan Partnership

Solving problem cases whilst increasing conversions & income

Talk to The Loan Partnership and we’ll help solve even the toughest of challenges

Are you having trouble placing a customer with suitable finance? At The Loan Partnership we’re more than used to complex cases, one email or phone call to us is all it takes to solve the problem.

We’re ready to help you meet your targets, including converting the hardest challenges. We work closely with our panel of lenders to match the most suitable loan for your client, even when they appear to fall outside standard criteria and have been turned down elsewhere.

The following list of people can ALL be helped, with a Second Charge mortgage…

- Self employed or employed without proof of earnings

- We can help people who have just relocated

- Low equity in their property- LTV is available up to 100%

- People with a low credit score due to previous financial difficulties

- CCJs or fallen into arrears – plans available

- Debts outstanding on loans or credit cards – we can help them consolidate

If you have a case that could benefit from our expertise, no matter how challenging, then contact The Loan Partnership today. You can be sure we’ll do everything we can to help.

To find out more, talk to The Loan Partnership on 01923 250 090 or contact us online and see how we could help you and your customers.

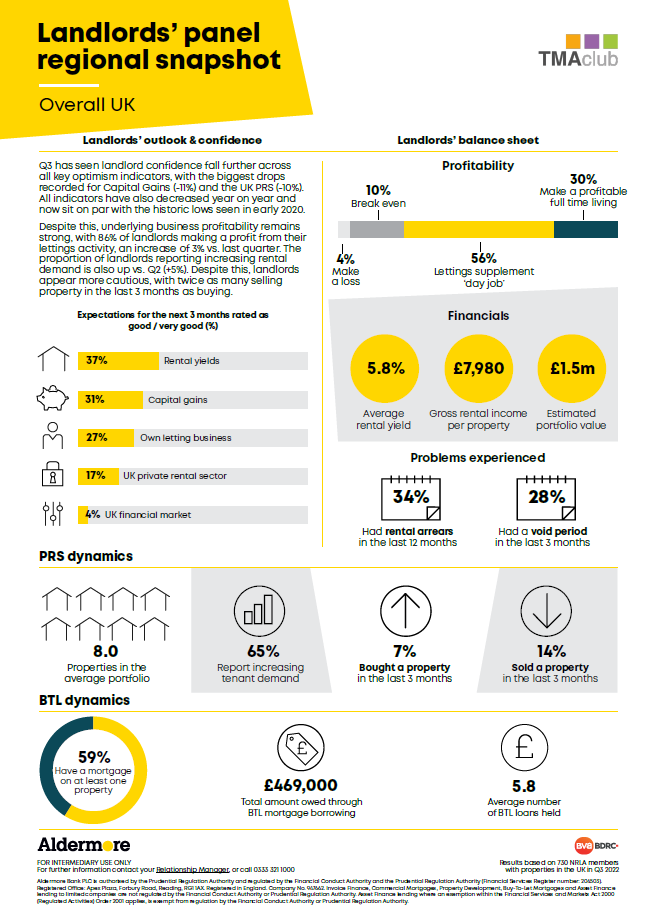

Aldermore

Aldermore BDRC Landlord Data

Zephyr Homeloans

No let-up in UK rent rises

In their Q3 Rent Index Report, our friends at The Deposit Protection Service (The DPS) – also a part of the Computershare group – reported on the latest trends in the sector based on their huge pool of landlord data. As Zephyr is a specialist buy to let lender, this insight is of great interest to us, and it also makes useful reading for brokers and their landlord clients.

Not surprisingly, given the UK’s rising cost of living, there has been no let-up in UK rents rises. At the end of Q2 we brought you the news that there had been the biggest quarterly increase on record at 2.47%, and Q3 isn’t far off that with a 2.18% increase, making average rents £889. This is an increase of 8.68% since Q3 2021.

When it comes to looking at regional data, rents in London stand out as they accelerated by 4.24% (£61) to £1,499 during Q3 2022. Average rents in the capital increased by 11.95% (£160) between Q3 2021 and Q3 2022.

Yorkshire, North West, East Midlands, Northern Ireland, and East of England also saw rent increases of more than 2% during Q3 2022.

Across the UK, flats saw the greatest percentage rent increase between Q3 2021 and Q3 2022, up £79 (9.52%), from £830 to £909.

Matt Trevett, Managing Director at The DPS, said: “Rent increases continued across the UK during Q3 2022 as a result of well-documented shortages in rental stock and general increases in the cost of living. “Ongoing demand for larger properties in London, as well as flats during the past 12 months is driving the significant rent increases we’re seeing in the capital. “In order to secure a property, tenants are still willing to pay historically high rents.”

Paul Fryers, Managing Director at Zephyr Homeloans, said: “Increases in the cost of living and property finance mean that landlords are facing higher maintenance, insurance and other costs.” It’s more important than ever that brokers do all they can to source the right mortgage deal for their landlord customers.”

Read the full Q3 2022 Rent Index report and regional summaries here.

Complete FS

New lenders, more choice!

Whilst the headlines have rightly focused on the sharp reduction in mortgage products available, there is an irony that the specialist market continues to attract new entrants.

Tougher economic conditions with high inflation and increasing interest rates will inevitably result in an increase in the number of clients requiring specialist mortgages, more lenders of course mean more choice.

The two new product ranges below have restricted distribution but are both available to TMA members through Complete FS:

Tandem Bank

Tandem Bank have a long-established reputation for unsecured finance but have now ventured into the specialist 1st charge remortgage market. Complete FS are part of this initial soft launch which looks to cater for clients not served by the High Street.

- Lower rates for EPC of A, B,C

- Credit blips

- Most cases require an AVM valuation only

- 100% of commission, bonus, overtime accepted

All Tandem products are available via Complete FS – Product Guide – Residential

West One

West One are a lender well known for Buy to Let, Second Charge and Bridging Loans. It is therefore a natural progression for them to launch Residential Mortgages. West One’s offering is a combination of flexible underwriting with market leading rates. Some of the best features are:

- Credit blips accepted

- Lending over retirement age

- A flexible approach to income type

- High income ICR available

All West One products are available via Complete FS – Products – Residential

Lendinvest

There’s no need for developers to panic

You don’t need me to tell you the economy has caused some uncertainty recently; it has dominated the press for months now.

A lot has been made of the impact on mortgage prices, rents and property values as the economic challenges have continued on, but where do developers fit in all this, and why should they not panic?

- Underlying demand

- Challenges remain the same

- Finding flexibility

LendInvest’s Head of Development Finance looks at the current market and why there is no need for developers and property investors to panic.

Santander

Helping you get a quicker offer

Here are some simple tips to help you get the right decision first time, saving you time and effort.

- Always use our affordability calculator

It’s quick, easy to use and will tell you how much your client could borrow. - Only provide us with the documents we ask for

And always make sure you check the names and addresses match the application. - Always provide supporting information

Please tell us any soft facts about your client that will help our lending decision e.g. tell us what any capital raising is being used for.