April Events

Pure Update with My Care Consultant – 21st April 10am

An update from the Pure team along with guest speaker Tony Miles from My Care Consultant who will be focusing on the topic of ‘Financial Vulnerability Taskforce’ and their very own ‘Business Development Care Box’ and how they can help.

Holiday Lets now available from InterBay Commercial

Over the last 12 months there has been an unprecedented demand from consumers for UK staycations for various reasons including:

- The uncertainty regarding international travel

- Wanting to ‘escape’ from the home after spending extended periods of time ther

- Many consumers are feeling the financial impact of the pandemic and changing behaviours from holidays abroad to domestic stays.

As a result of these factors the demand for Holiday Lets has significantly increased and InterBay Commercial are keen to support this growing area for BTL landlords.

Highlights of our new product range include:

- Maximum 70% LTV

- Purchase and Remortgage

- Limited Company and personal ownership structures

- Maximum loan size £1million

- Minimum income per application – £30k

Other features of the new Holiday Let range include the BTL landlord can occupy the security for up to 60 days per annum for their own personal use which should be very well received and the affordability will be calculated on a commercial rental assessment basis (the average of high, medium and low seasonal rates).

Residential shared ownership products

With products up to 75% LTV (on full market value) on loans of up to £1m, our shared ownership range is designed to help your specialist clients with limited deposits.

With a wealth of experience in shared ownership, coupled with our common-sense lending and manual underwriting, our shared ownership product range is here to help you and your clients navigate the new normal.

C is for Case studies

At Zephyr they are dedicated to meeting the needs of Portfolio Landlords, hear from one of their BTL experts, Andy Rowe, about a recent Portfolio Landlord case study and find out they can help your clients, tune to our video here.

Here’s some criteria highlights that could be of benefit to your clients…

- Unlimited background portfolio with surplus portfolio rental income considered to support an application in certain cases

- Background stress test; rental income simply needs to cover 100% of the Zephyr mortgage(s)

- We partner with eTech’s BTL Hub to allow you to send through additional background information in a quick and simple way.

Criteria Changing

Leaseholder/Freehold connection

-No first charge on the freehold, only a legal charge

Minimum Size

– Reduced from 35SQM to 30SQM for studio flats in an urban area

Exposure Limit

– Will consider lending on all units in a block of 4 or less flats. If the block has 5 or more flats, fleet will still lend against 2 or 20%

Portfolio Landlord

-Now only require an asset and liability statement statement from the main applicant owning 4 or more properties.

Criteria Update on Expat products

With immediate effect Marsden Building Society will only lend to applicants who reside in the following countries:

• Canada

• Hong Kong

• Japan

• Korea (South)

• New Zealand

• Singapore

• Switzerland

• UK

• USA

• UAE

• Qatar

• Saudi Arabia

• Kuwait

The above relates both to our Expat Residential and Expat BTL products.

Please note, this change does not relate or impact our acceptable currencies list which is applicable for Expat residential and we still have no currency restrictions on Expat BTL.

Expat products can be based in any country as long as its not classed as High Risk/Monitored Jurisdictions or Australia.

See updates below from santander

- Introducer Internet downtime

Introducer Internet won’t be available from 9pm on Saturday 17 April until 6am on Monday 19 April.Your brokers won’t be able to submit cases during this time. We’re sorry for any inconvenience caused.

- Santander are changing how they assess residential self-employed applications

Click here to see the full details.

- Santander are supporting the mortgage guarantee scheme

Find out more.

There when you need them

In 2020, L&G paid out over £763 million across thier Life, Critical Illness Cover, Terminal Illness Cover and Income Protection policies, supporting 15,855 customers and their families.

L&G also supported families who lost loved ones due to factors attributable to Covid-19, paying out over £39 million in life insurance* claims – helping 1214 families.

Overall, they paid £32 million more in claims than in 2019, adding to a total of £3.19bn paid over the last 5 years

Case study: 5 days from Buy To Let application to offer

Lendinvest pre-offer Buy To Let team goes in-depth on a recent case to showcase how they deliver a quick speed to offer. Read more

Service Update

Following our recent return to 95% LTV lending for first-time buyers and home movers, we’re seeing an increase in calls to our Broker Support team.

To help them help you, please ensure your cases are fully packaged before submitting them and use web chat, phone and eMortgages for case updates where you can. This will free-up our teams and allow them to help more of you.

Please note, because we’re busier than normal at the moment, there’s a chance you might have to wait a little longer.

You can keep up to date with our service levels here.

Welcome. And welcome back.

You’d usually only get to hear their voices, but soon you’ll be able to see their faces too. Prepare to meet our Telephone Business Development Managers (TBDMs). They’re currently creating a series of live monthly webinars for brokers who have never used our service before, and brokers who have, but might want a refresher on what we offer.

You’ll be able to register for the webinars next week. In the meantime, here’s a preview of what to expect:

The ‘welcome’ webinar (new brokers)

- Find out about Skipton Building Society for Intermediaries.

- How to navigate our website/system.

- Our key lending criteria.

The ‘welcome back’ webinar (a refresher)

- Affordability, hints and tips for using the calculator.

- Hot criteria topics.

- Technology improvements.

Not to be missed

We’ll send another email when registration opens. If you can’t wait till then, take a trip to the Skipton Talks hub to view our on-demand Spring Webinar Series and read thought pieces from people in the know.

How’s This For Flexible? Maximum Loans For The Self-Employed

Complete FS have a full time dedicated TML underwriter waiting to approve applications for your self-employed clients.

TML’s new improved product range is extremely flexible and could really help your clients. Here’s how:

- Income based on the latest year’s accounts (No averaging)

- Profit before tax, plus salary used for affordability

- Minimum of 12 months trading up to 85% LTV

- Contractors up to 85% LTV – 48 x weekly rate (12 months experience)

- Businesses with CBILs and Bounce Back Loans considered (cannot be used for deposit funds)

Also, don’t forget we can help self employed applicants with credit impairment.

If you have self employed clients that need a flexible lender, please give us a call – 023 8045 6999 Option 1.

Meet the team – Quickfire Introductions

Raji Sidhu-Housden

Raji started at Saffron Building Society in 2017 working as an Arrears Officer. As she moves into the Business Development Team, Raji will be bringing her ability to develop and nurture trusting relationships. As a Business Development Administrator, Raji’s immediate goal is to gain a CeMap qualification to assist in continuing the growth in her ability to provide mortgage advice.

“I am really looking forward to assisting Saffron for Intermediaries in growing the number of intermediaries that use us regularly, by offering exceptional customer service, knowledge and expertise in specialist markets.”

Simon O’Donnell

Starting as a Branch Manager in 2016, Simon has had a number of roles within Saffron Building Society and is now excited to be in his new role as Business Development Manager for Saffron for Intermediaries.

“I’m a real advocate for Saffron Building Society and the products it provides. Over the last five years, I have built great knowledge of the Saffron Building Society mortgage products, and I look forward to bringing this to the Business Development Team.”

Phil Lawford

Phil Lawford started at the beginning of March in his role as a Business Development Manager. Phil boasts over twenty years as a Business Development Manager and will bring a raft of experience and knowledge to the Business Development Team.

“It is a wonderful opportunity, and I can’t wait to help raise the profile of Saffron Building Society among the intermediary market.”

Linsey Smith

Linsey joined in November of last year and has taken on an Administrator role in the Business Development Team. As part of her role, Linsey will be taking technical support calls, and overseeing live web chats, as well as supporting the team with reporting and administration as required.

“We are the first contact for Intermediaries when they enquire with Saffron for Intermediaries. I want them to be met with professionalism and efficiency, and I look forward to building up good relationships with our intermediaries”

Free LearningLab Live event, in association with Protect Commercial

Source can probably all agree that the property industry has been affected by COVID-19, but just how much?

It has been over a year of lockdowns in the UK. What’s the economic state of the mortgage and insurance industry 12-months on? Join this Source LearningLab Live to find out.

Source are hosting a LearningLab Live event, in association with Protect Commercial and guest speaker, economist Roger Martin-Fagg.

During this 90-minute event, they will be discussing how the economy has changed over the last year and how it has affected the mortgage and insurance market. Roger Martin-Fagg will be looking forward and providing his views on inflation, interest rates and house prices in the next 3 years. Find out how Roger’s outlook differs from the mainstream economists.

There will also be an opportunity to discuss and ask questions around the General Insurance (GI) landscape and the Commercial Insurance outlook.

The event will take place on Wednesday 21st April 2021 at 10am and will count towards your Continuing Professional Development (CPD) goal.

All attendees will receive a recording of the LearningLab Live and a CPD certificate as proof of their attendance, after the event.

Visit the webinar here to secure your place at this free event.

Could your residential remortgagers benefit from a Green Rewards cashback remortgage?

Foundation Home Loans, the intermediary-only specialist lender, has today launched a set of 75% and 85% LTV residential ‘Green Reward’ remortgage fixed rates over two- and five-year terms as part of its residential range.

The new product is available to existing owner-occupier borrowers who have made improvements to their home, who must have obtained an Energy Performance Certificate (EPC) rating of ‘C’ or above – dated within the last 24 months.

- £750 cashback on completion

- Up to 85% LTV

- Reduced product fee of £595, normally £995

- Deliberately simple criteria: specific types of improvements stipulated

The products are only available on a capital and interest repayment basis.

The product has been designed to offer a greater degree of choice for those conscientious homeowners who are not able to access high-street lenders, but who undoubtedly should be rewarded for improving the energy efficiency of their home. It is hoped that the product will act as a further catalyst to support the reduction of the carbon footprint from UK residential properties.

Before and after; do the effects of the Covid-19 pandemic on Britain’s borrowers mean that specialist is the new mainstream?

2020 in numbers

4.5 million – Number of workers on furlough in January 2021 as a result of the pandemic.

454,000 – Increase in unemployment in the year to December 2020

10 years – Time to save for a first-time buyer house deposit, saving at the average rate out of average UK income (at July to Sept 2020 rate of household saving.)

+7.9% – Increase in average first time buyer house price in 2020

14% – Proportion of the pre-pandemic self-employed who were no longer working in January 2021, up from 9% in May 2020.

61% – Proportion of the self-employed whose overall financial situation has worsened due to the pandemic.

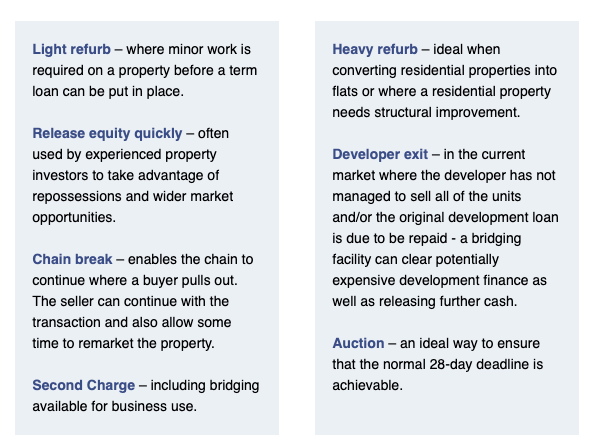

Reasons to consider Bridging Finance via impact packaging

Bridging can be arranged by Impact Specialist Finance on a regulated or non-regulated basis. The risk can be spread over more than one property to ensure the cheapest rate is applicable and can help to reduce the deposit required.

Impact has a dedicated bridging team who are experts in their field and are here to help with your bridging enquiries.

Impact have access to market-leading rates and dedicated underwriters to help you with the following scenarios (subject to lenders T&Cs).

Its a great time to partner with a specialist packager/distributor so you can take advantage of those rewarding opportunities. Even if you don’t have the relevant permissions or you want to pass over the client, impact can help.

85% LTV

Impact Specialist Finance has been provided access to exclusive 85% LTV mortgages from Pepper Money.

Pepper 24 is available to customers who may have experienced defaults, missed payments, arrears or CCJs in the last 24 months. The 85% LTV exclusive is available at 4.60% for either a two or five-year fixed rate.

Pepper 24 Light is available for customers who may have experienced defaults, missed payments and arrears in the last 24 months, but received no CCJs.