LendInvest

How can brokers take advantage of green Buy-to-Lets?

The team at LendInvest are looking ahead to the future of the property market. To support landlords and developers making smart investments in energy efficient properties, our latest Buy-to-Let launch has included a new, cheaper product range – called EPiC – to incentivise investing in greener properties. Find out more about the new catalogue here.

It isn’t just because COP26 was in town – reducing emissions has been a hot topic in the lending industry for months now.

‘Greener’ mortgages or incentives are now everywhere in the market, offering your clients a lower rate or cut-price fees based on their properties meeting some form of more environmentally friendly criteria.

With so many of these appearing in different forms – how can you get the most out of these deals for your clients?

Find the lenders who have gone the extra mile

It is a trend to look green at the moment, but what is labelled as a green or environmentally-friendly product might not offer that much.

Obviously it is great to save on things like legal or val fees where possible, but it is worth researching the breadth of a lender’s offer.

Some are introducing whole ranges to incentivise green investments, taking bps off of all of their rates for properties which meet their criteria.

Our EPiC range, for example, adapts our standard 2-year, 5-year and 7-year Buy-to-Let ranges and cuts all of the rates for properties meeting the necessary EPC criteria.

Tell your clients to look green

The government already wants all rental properties to have an EPC rating of C from 2025, and with reducing emissions a key matter of public policy which won’t go away, landlords should expect more legislative changes for them to improve the efficiency of their portfolio.

With this in mind, and looking at the green products on offer, landlords should get ahead of this now by targeting environmentally-friendly property.

While this might mean they are looking at a higher purchase price, it could save them money in the long run.

Consider bridging the EPC gap

With government requirements for EPC ratings changing from 2025 and lenders incentivising improvements now, it is smart to perhaps look at bridging finance to help meet these requirements early so landlords can reap the benefits of lower costs and from being able to offer higher-quality housing to their tenants.

Bridge-to-Let, Refurbishment and small bridging products can all assist with getting a property up to the EPC rating where they will then qualify for a lower Buy-to-Let rate.

For example, LendInvest’s EPiC Star range is a set of even lower-cost rates for landlords who improve their EPC rating with our bridging products and refinance onto our Buy-to-Let.

Buckinghamshire Building Society

An enhanced application process

1. Enhanced application process – Based on extensive feedback from you, our brokers, we have launched an enhanced application process, which makes submitting a DIP and application simpler, with the emphasis on a slick user journey. The new process allows DIPs to be processed electronically through our Broker Online platform, and automates the link between the original DIP and subsequent application, preventing any duplication of keying. The system will keep you fully up to date on what stage each application is at, enabling you to keep your clients in the loop of the progress of their application. The system is simple – find out how to use it here.

2. Want to fast track your clients’ case? Simple! Just follow these easy steps and your case will be on its way to our underwriting team in no time… Submit application with: – Fully Completed DIP Checklist (this will be provided with DIP acceptance email) – All supporting documents, with file names that match the DIP Checklist – Finally, please ask your client to call us on 01494 879517 to pay the valuation fee ASAP. Please note, any cases submitted with missing/incorrect documentation cannot be progressed to the underwriter until this is received.

Suffolk Building Society

A new affordability calculator

Suffolk Building Society have launched a new affordability calculator with a more intuitive design and the ability to build in scaled LTI calculations – up to 5.5x this should help brokers find the max loan for their clients.

Check the calculator out here.

Landbay

New Limited Edition BTL remortgage

Landbay has launched an exciting range of Limited Edition 5 Year remortgage only products, with rate reductions of up to 25 bps!

The products are available for standard, small HMOs and MUFBs for loan sizes between £250K and £500K.

For more info, speak to your local BDM.

LiveMore

Clients over 55?

LiveMore is the specialist lender solely focused on those over 55 who are struggling to purchase or remortgage their homes with mainstream lenders and banks.We all share a passionate desire to overturn the failing attitudes that make life so difficult for intermediaries who want to help customers whose only issue is their age.

Helping the borrowers other lenders can’t reach

- Mortgages for over 55s made easy

We have no maximum age, lending up to 75% LTV on our products, ranging from 5 years, all the way up to lifetime. - A fresh look at affordability

We look beyond age, focusing on more relevant financial issues. All income, assets and savings are considered. We have no cap on employed / self-employed income. - Longer term fixes

No set repayment deadlines or early repayment charges in the event of a borrower’s death. We also offer up to 6-month payment breaks when major life events occur. - Revolutionary Ongoing Care Fee

For every annual customer care call completed, we will pay 0.13% (in addition to the 0.55% gross paid after completion), for up to 15 years after completion.

Contact us today to see how we can help your clients!

Call us: 0203 0114 991

Email: Sales@livemorecapital.com

100% of our customers would recommend us, and our Intermediaries think we are pretty great too!

“LiveMore – the lender that this market has been crying out for” – N. Pamment, Inspirational Financial Management

TFC

Gold partner testimonial

Sundeep Patel, Director of Sales at Together, said: “Our Gold Partner brokers receive a number of fantastic benefits, including access to some of our exclusive products an underwriter point of contact and a field account manager, among other major benefits. TFC Homeloans are renowned for their knowledge and skill when it comes to packaging even the most complex cases. This makes all the difference to specialist lenders such as Together and we’re proud to call them one of our Gold Partners.”

Zephyr Homeloans

Starting November with a bang!

It’s November already! The days are getting shorter and colder, so get cosy and have a read of our weekly update before you venture outside…

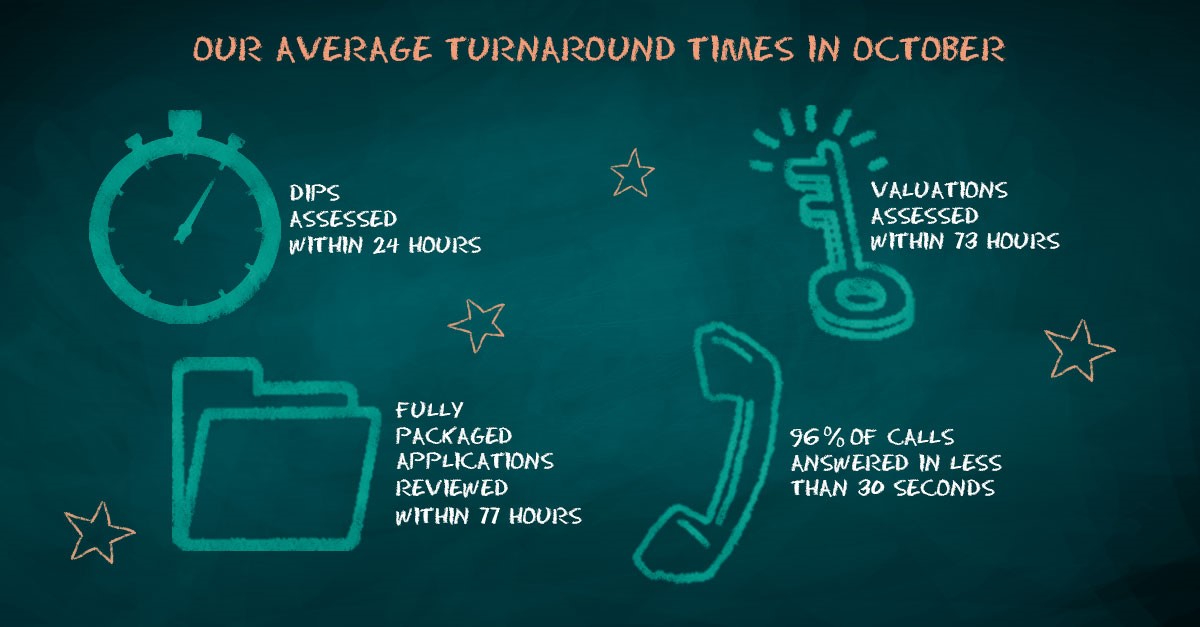

- We’ve shone a light on our current turnaround times, so you always know where you stand.

- Our RSM’s and BDM’s are on fire! Not literally, they just know their stuff so please contact them if you have a specific case query, quick question, or just need an update. They will get back to you in a flash.

- We’ve included a sparkling new case we’ve recently supported, to highlight the sort of cases we can lend on.

- Check out our new Friday Fact, for a little something you might not know.

- Finally, if you want to see us face to face you can see our full events list for November.

October’s turnaround times are in and it’s been a good month for service. We had some complex cases to support, which lengthened our review of fully packaged applications slightly mid-month, but this is already reducing and will improve further in coming weeks.

We think it’s important you always know where you stand, so our average turnaround times are updated on our homepage each working day by 9:30am.

To discuss a new BTL case find the contact details for your RSM or Telephone BDM on our website.

Client converting multi-unit property consisting originally of a flat and commercial unit to two leasehold flats whilst retaining the freehold.

We will lend on the original flat with a personal guarantee from the freeholder, whilst the converted flat is to be sold. Proceeds from the sale and remortgage will be used to repay the original bridging loan used to finance the purchase and conversion.

Upcoming events

- 9 Nov – TMA Virtual Panel Workshop – Virtual

- 10 Nov – Financial Reporter BTL Roadshow – Bristol

- 11 Nov – Financial Reporter BTL Roadshow – Derby

- 11 Nov – British Specialist Lending Awards – London

- 22 Nov – Mortgage Introducer Awards – London

Legal & General

Business Protection Bootcamp 2021: Get fit for business in a fortnight.

53% of businesses say Covid-19 has made them more likely to consider protection

From Monday 15th November – Friday 26th November, we’ll be hosting seven fantastic live learning sessions. Hosted by our award-winning Business Protection team, they’ll provide exclusive insights from the market with an opportunity to ask our industry experts anything around Business Protection.

Refocus, refresh and re-energise your Business Protection conversations today.

With an increase for businesses to learn about protection through an adviser, our CII accredited structured CPD webinars are designed for you to support your client conversations. Each webinar starts at 1:30pm and will last approx. 30-45 minutes. To help your business grow and you to prosper, our two-week programme includes:

Bootcamp #1: State of the Nation SME’s research.

Monday 15th November. Our latest research uncovers the risks to small and medium size businesses and the opportunities within the Business Protection market. Register here

Bootcamp #2: Key Person Protection

Tuesday 16th Insight into the need for Key Person Protection and how to write the policies, including the tax treatment. Register here

Bootcamp #3: Key Person Income Protection

Thursday 18th November. Introducing our new Key Person Income Protection, to protect the business in the event of employee absence. Register here

Bootcamp #4: Relevant Life Plan

Friday 19th An overview of the opportunity to write RLP’s and how the policies are structured in a tax efficient way. Register here

Bootcamp #5: Executive Income Protection

Monday 22nd Identify where Executive Income Protection and personal Income Protection fit into the advice process. Register here

Bootcamp #6: Shareholder and Partnership Protection

Wednesday 24th Covers the most common structures for these arrangements, any legal agreements required and how the level of cover is identified. Register here

Bootcamp #7: Articles of Association and company accounts

Friday 26th Great insight into the protection a business needs and how to ensure it’s written in the best way. Register here

West One

HMO remortgage for large portfolio landlord with over 100 properties

Finding the right buy-to-let mortgage can be difficult for portfolio landlords, many high street lenders are unable to lend to landlords with 4 or more properties because of their strict underwriting process that focuses on individual affordability.

At West One, our range of buy-to-let products are available to a wide range of individuals including large portfolio landlords. Our specialist underwriters don’t use a credit score, instead each case is assessed on its own merit. This approach recently enabled us to help a portfolio landlord to remortgage a 6 bed HMO.

Loan Value: £1,030,000

LTV: 75%

Property Value: £1,375,000

Loan Term: 20 years

The Client: The client was a property developer, with a large portfolio of buy-to-let properties. They were looking to remortgage an existing 6 bed HMO property to fund an onward purchase.

Situation: With over 100 buy-to-let properties the client was looking for a lender that offered a flexible approach to finance the remortgage of their property which was valued at £1,375,000.

Our Solution: As a result of our flexible approach to portfolio landlords we were able to offer the client an advance of more than £1 million pounds at 75% loan to value with our Specialist W1 product range at a 5-year fixed rate of 3.54%.

Benefit: West One’s unique approach to credit risk meant that we could be flexible in assessing the clients’ portfolio and did not require stress testing of the client’s portfolio.

Result: The client was able to remortgage their existing HMO property in just 45 days meaning that they could complete on the purchase of a new property without any hold ups.

The Mortgage Lender

The Lowdown on the Self-Employed

We like to make working with us as easy as possible– helpful info and advice that highlights how we do business and makes your life easier.

This week we’re looking into our lending criteria for the self-employed. That way, the next time you’ve got a freelancer, sole trader or contractor looking for a mortgage, you’ll know exactly how we do business.

When it comes to self-employed, did you know:

- We will consider using 2019/20 accounts for applicants whose most recent accounts have been impacted by Covid if their last 3 months business bank statements show a return to a similar level of turnover (speak to a BDM before submitting an application)

- We will accept one years’ trading and use their latest year’s figures without averaging, even at 85% LTV

- We will use their share of profit before tax plus their salary for affordability

- Can accept accounts or SA302 as proof of income

- Base contractors’ annual income on 48 weeks a year (12 months previous experience with minimum contract term remaining)

We consent and encourage for this release to be used in any weekly round up/newsletter/email/social comms if applicable.

If you have any questions or require any further information, please get in touch and let me know.

TBMC

Student life is good for buy-to-let

Recently, Paragon Bank published an interesting report on student letting which highlighted some of the reasons this area of buy-to-let is popular with the UK’s landlord community.

In this broker update we discuss:

- Popularity of student lets

- Rental yields

- Location and opportunity