Four tips to nail those menu conversations

By Shelley Read, Senior Protection Development and Technical Manager

Making Menu Plans meaningful to clients can be a challenge. What is a Menu Plan? Why do I need one? How and when will it pay out? These are just a few questions you might be asked on a regular basis. So where do you start?

We want to help you have compelling Menu Plan conversations – that’s why we’ve put together some useful hints and tips to help you bring the benefits of Menu Plans to life.

1. Establish the protection need

If your client was too ill to work, could they cope financially? Is there a financial problem they wouldn’t want to face, should the worst happen? This is your starting point for recommending a protection solution.

Some useful questions to ask include:

‘If you had to take two months or more off work due to illness or injury, what would happen to your monthly outgoings?’

‘Could your family afford the mortgage payments without your income?’

We often use the ‘IAN’ model – ‘ideal’, ‘actual’ and ‘need’. If the worst happened, what would be your client’s ‘ideal’ financial situation? Then, what ‘actual’ financial provisions do they have in place? From here, you can work out their protection need. When calculating their ‘actual’ financial need it’s important to consider things like how much money is available to cover essential bills each month, and whether they’ve employee benefits or if they’d need to rely on the state.

The desired outcome for most clients is to be in a position where they can repay their monthly outgoings, including their mortgage payments – so they can keep their home and not struggle financially.

You’ve now created a situation where your client has become aware of their protection need and is looking to you to provide a solution.

2. Make the risks relevant to them

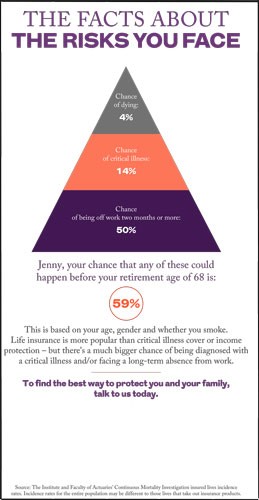

Our risk report provides a powerful way to show your clients the key risks they face – establishing the need for a protection solution that covers multiple claim opportunities. Based on your client’s personal information, it shows their chance of death, critical illness and being off work due to illness or injury for two months or more before retirement.

If you take the example of Jenny*, aged 34 on her next birthday and a non-smoker, the risk report shows that although she only has a 4% chance of dying before she reaches retirement, she has a 50% chance of being off work for two months or more due to illness or injury.

As you can see the argument for a plan that covers different eventualities becomes pretty compelling.

3. Demonstrate the chances of a claims payout

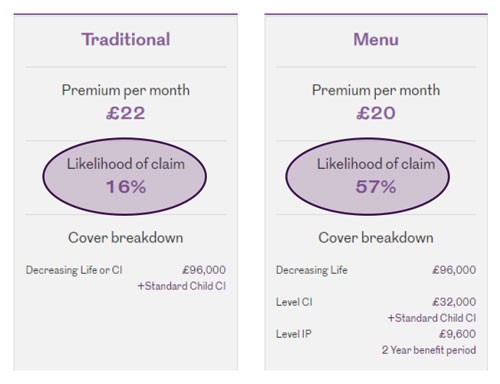

Now you’ve established the need for a multi benefit plan, we’ve a new menu tool to help you bring the benefits of menu to life and show how a menu plan means more cover for life’s uncertainties.

Our menu tool highlights the difference in chances to claim between a traditional protection approach and a menu approach, showing a side-by-side comparison.

While a traditional approach – covering life and a bit of critical illness – may not provide a high enough chance to pique a client’s interest, a menu approach shows a much greater chance of claim, often at a lower cost. This highlights the benefits of a comprehensive, flexible Menu Plan that protects clients for multiple life events and gives them peace of mind they’d be financially protected, should the worst happen.

4. Spot protection opportunities

The beauty of Menu Plans is their flexibility. Whether your client is a home owner or renting; single, a couple or a family – a Menu Plan can be tailored to their life stage. And you can adapt a plan if their circumstances change.

Some key opportunities to look for in your existing client bank could include:

- Clients with life cover only – they’d have no protection at all if they fell sick

- Self-employed clients – without employee benefits, if they fall sick they’d have to rely on state benefits or their savings

- Families – talk to families about protecting their mortgage, bills and lifestyle to keep things as normal as possible for dependents if the worst happened

- Divorced clients – may suddenly find themselves with just their income and no partner to rely on if they fell sick and needed to take time off work

- Parents paying school or nursery fees – family income benefit could help maintain these fees in the event of death or critical illness, with Income Protection providing additional cover

- Clients needing flexibility – those renting, starting their career or with aspirations to buy are the perfect fit for a Menu Plan that can change as their life and family evolve

These are just some examples of clients that could benefit from a Menu Plan conversation with you. For more ideas and information on how recommending Menu Plans can help you grow your business, demonstrate the value of your advice and ensure your clients get the cover they really need, listen to our ‘nailing that menu conversation’ webinar.

*This example is for illustration purposes only. It doesn’t represent an actual customer. Example used is a female (34nb), non-smoker, expected retirement age 68. Illustration produced using studio.royallondon.com risk report, ‘The facts about the risks you face’, accessed January 2021.